In this post we look at how company’s can manage the cash flow statements and hide the true economic picture of the company.

The Financial Shenanigans Series:

- Part 1: Manipulating Revenues

- Part 2: Manipulating Expenses

- Part 3: Those Cash Flows!

- Part 4: Key Metric Shenanigans

- Part 5: Acquisition Accounting

In this post we look at how company’s can manage the cash flow statements and hide the true economic picture of the company.

It is considered that cash flows are hard to manipulate, when compared to the profit and loss statement, however managements which want to hide the true economic picture of their company will find ways to do so. We also need to remember that in the indirect method of computing cash flows (used by all company’s), we first start with the earnings before tax and make adjustments to arrive at the cash flow from operations (CFOs). Hence if the earnings are manipulated then it will also spill over to the cash flow statement.

Many of us focus on the cash flow from operations (CFOs) or cash profits while looking at the cash flow statements and rightly so. CFOs show the amount of cash that the company generates by running its day to day operations, however company’s are also aware of the importance of CFOs and the amount of focus that it is given by all stake holders. Hence it is advisable to look at all the 3 sections – operating, investing and financing closely while analyzing the cash flow statement.

While the CFO must be looked at closely to check what is driving this, broadly one should check if

- CFO versus net income – we are here comparing the cash profits with the accounting profits. For instance if the CFO lags net income over long periods it is an area of concern and must be investigated

- CFOs and net income should be in line over a period of time

Cash Flow Shenanigans

The three techniques in which cash flows are manipulated are

- Shifting financial cash inflows to the operating section

- Moving operating cash flows to other sections

- Boosting operating cash flow using unsustainable activities

Let us say a company borrows a loan from a bank and the collateral that it keeps with the bank is its inventories. This is normal loan and should be recorded as a liability on the balance sheet and appears in the cash flow from financing section.Can the company treat this transaction in a different way, which leads to change in the cash flows? The answer is yes, and let us see how this happens

The company keeps inventory as a collateral, it can now record a sale of inventory to the bank. The sale reduces the cost of goods sold on the P&L and reduces the change in inventory on the cash flow from operations section, this treatment of a vanilla loan leads to increase of earnings and cash flow from operations. Delphi Corporation in 2000 had followed this method to boost its cash flow from operations.

Another way of boosting the CFO is by the way of selling its receivables before its due date. Companies can sell their receivables either by way of factoring or securitization. When the company sells its receivables and collects cash, the receivable balances go down and the cash collected should ideally be shown in the CFO. While there is nothing wrong in selling receivables and realizing cash, things to keep in mind while looking at these transactions are

- Has the liability of the receivable been shifted to the buyer (usually banks) or the company is still liable if the vendor fails to pay on the payment date. There may be case where a loan is taken by having receivables as collateral, in such a case it is a loan and not sale of receivable

- Is the company doing this regularly? If so, it may indicate that the company is shifting future period cash flows in the current period

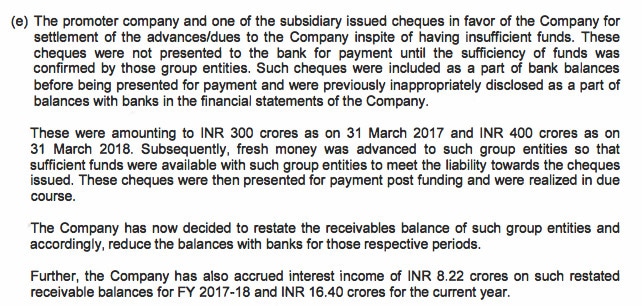

There may be cases where even before receivables are yet to be realized the company records cash on its books. In other words, the company shows increases its cash balance but the payment from the vendor is yet to be received. Take the case of CG Power and Industrial Solutions which was in the news off late for misrepresenting its financial statements.

CG Power was to receive monies from promoters and subsidiaries, however before it received the cash, the company recorded these monies as part of the bank balances. These have been restated as receivables for the period to which they pertain.

Take one more case where receivables were netted off inappropriately

In the above case the action of netting off reduces receivables to the tune of amount, Rs 245 Cr in this case. Reduction in the receivable balance boosts the CFO. For instance in this case 245 Cr of working capital in the form of receivables was freed up and assuming that the receivable balance remains constant, this amount is reduced to arrive at the final CFO.

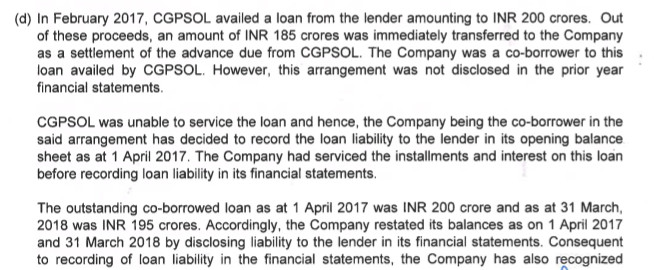

One more instance where the receivables had to be reinstated

In the above case the company was supposed to received monies from CGPSOL and did receive the same, however CGPSOL had availed a loan of Rs 200 Cr to make this payment and the company was a co- borrower to this loan. CGPSOL had defaulted on this loan and the company took this debt on its books. The company prior to taking this step had adjusted the loan with its retained earnings, however the loans and receivables have been treated accordingly.

Shifting Operating Costs

Shifting of normal operating expenses from the operation section also gives a boost to the CFO. Operating costs are normally shifted to the cash flow from investing section.

We had discussed as to how capitalizing expenses boosts earnings on the P&L statement. Capitilizing expenses also gives a boost to the CFO. Let us see how this leads to an increase in CFO

When companies capitilize expenses they are put on the balance sheet as an asset. Since expenses on the P&L are not recorded the net profits takes a boost. The starting point of arriving at the CFO is earnings before tax (EBT), this is the indirect method of preparing cash flows. Since the profits are higher on the P&L, the starting point while preparing the CFO is also higher.

The asset purchase is recorded as an investing outflow in the cash flow from investing section. Hence, it is advisable to check the free cash flow (FCF) and compare this with the CFO over long periods of time. For instance say the cumulative CFO for a company over a period of 7 years is Rs 500 Cr and in the same period the company has a negative FCF of -300 Cr. This means that the company is not able to generate enough cash from its operations to meet its CAPEX requirements, they would need to raise debt or issue stock to meet this shortfall.

It may be the case that the company has to make investments as it sees an opportunity to create the CAPEX that it is doing, or there also may be a possibility that it is capitilizing its costs. It becomes very important to understand as to what is moving the CFO and the FCF.

There may be instances where purchase of inventories, which should appear on the CFO section are shown as investing cash outflows and do not appear in the CFO section, thereby overstating the CFO. For instance if a company is engaged in the business of selling CDs and DVDs, these are the companies inventories and any YOY change in inventories is shown in the CFO section. However to boost its CFOs, companies may record these as investing cash outflows and record them in the cash flow from investing section. The key here is to understand the nature and type of business the company is engaged in, in this case the primary business of the company is selling CDs/DVDs and these should be treated as inventories.

Boosting Cash Flows using Unsustainable Activities

CFOs take a boost, when companies undertake certain unsustainable activities. Primarily these manage the cash conversion cycle – inventory, receivable and payable days to boost their CFOs.

For instance a company may be collecting its receivables faster and as a result its receivable days will go down. This may be due to various reasons – efficiency in collections, discounts to vendors to buy products on cash or aggressive approach towards collections. We need to ascertain the reason for faster collections and understand if this is sustainable.

In the case of payables, companies may be deliberately paying their customers late or may be under financial stress. If it happens to be that the company is paying its suppliers late, this may be not be sustainable and supplies to the company may be effected if late payments continue.

Lower inventories may be stocked/bought to boost the CFOs. The down side of this is that if there is demand for the companies products and if it is not able to deliver its products on time sales of the company will be impacted.

It is important to look at the cash conversion cycle over a period of time and understand how it has changed and how will this shape up going forward.

Illustration

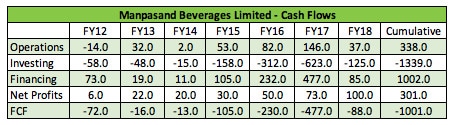

We now take a look at the cash flows of Manpasand Beverages and analyze the same.

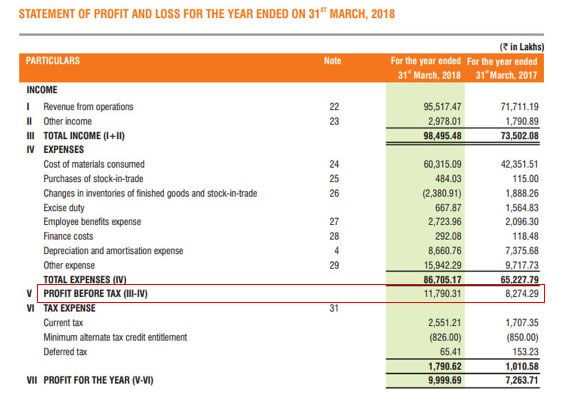

The cumulative CFOs for the 7 year period is Rs 338 Cr, as stated earlier we need to compare this with the net profits also known as the accounting profits, the net profits stand at Rs 301 Cr. CFOs have been greater than the accounting profits, which is good. However one can notice from the above table that these haven’t been consistent, for instance the CFO in FY14 was Rs 2 Cr and the net profits Rs 20 Cr. Similarly we can see huge divergence between the CFO and net profits in FY17 and FY18. We will take a deep dive into the FY18 cash flows and see what has caused this divergence.

Cash flows from investing have been Rs -1,339 Cr. The company has primarily used the money to buy business assets (property, plant & equipment), some part of the money is also used to buy financial assets. The company had come up with an IPO in FY16 for Rs 400 Crs and a follow up QIP issue in FY17 for Rs 500 Cr. The assets have been funded with the IPO proceeds, some of the proceeds have also been used to retire debt.

Free cash flow (FCF), which is the difference between CFO and CFI is Rs -1,001 Cr and that has been meet through financing (equity dilution).

The CFO for FY18 was Rs 37 Cr, however the net profits were Rs 100 Cr. Net profits were higher by Rs 63 Cr. Let us take a look in detail as to how the CFO for the year has been generated.

The cash flow statement starts with net profits before tax, we can observe that the net profits shown in the cash flow statement is different from the one in the P&L statement. The figure in the cash flow statement is Rs 100 Cr, whereas in the P&L, PBT stands at Rs 118 Cr. Adjusting for this the CFO should have been higher at Rs 55 Cr.

Non cash expenses, depreciation in this case to the tune of Rs 87 Cr has been added back and increases the CFO. Working capital changes – primarily receivables and inventories have lead to the CFO being less than the net profits. Receivables during the year have increased by 85% and stand at Rs 140 Cr versus Rs 75 Cr in the previous year. We need to check the increase in receivables with the change in sales, sales during the year have increased by 30%, from Rs 717 Cr to Rs 955 Cr. This means that the company has been slower in collecting its payments and this could be due to various reasons. Receivables as % of sales stood at 15% versus 10% in the previous year.

Working capital changes and trends have to be looked at over periods of time to check the direction of the working capital. Is this increase a one off or working capital requirements are changing structurally as the company is aggressive in growing?

The other item that has lead to drop in CFO is current assets

The balance with government authorities which was non existent last year, in FY18 stands at Rs 22 Cr. The company has some deposits with the authorities, we need to check if this is one time or will this amount increase going forward.

The tax expenses on the cash flow statement are Rs 45 Lakhs against Rs 18 Cr on the P&L statement. Why has the company paid taxes of only Rs 45 Lakhs versus recording 18 Cr on the P&L needs to be investigated. If the company had paid taxes of Rs 18 Cr, CFO would have further been reduced by this amount. The point we are trying to make by highlighting this is that paying taxes to this magnitude is unsustainable and we need to account for normalized taxes while arriving at the CFO.

Payables have decreased by Rs 15 Cr, decrease in payables should decrease the CFO. This is because the company is paying its suppliers faster, by paying faster the company no longer enjoys the advantage of suppliers funding the working capital that they did earlier.

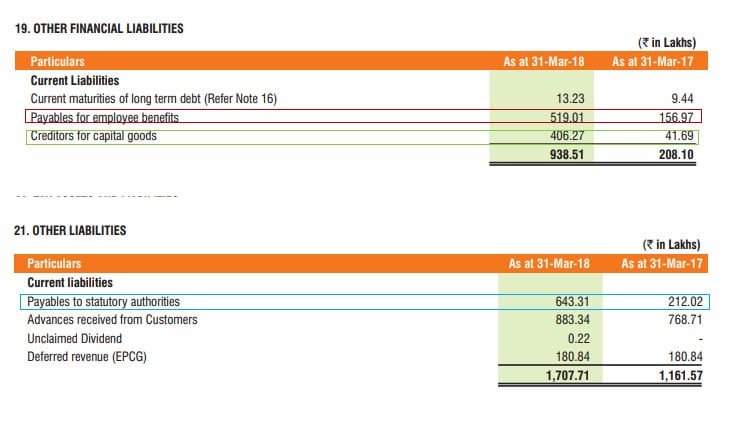

There has been increase in other payable items, which have reduced the overall impact while arriving at the CFO.

Payables to employees and statutory authorities has increased drastically, though these are small figures, but we need to check as to what has lead to this situation.

In the cash flow from investing section, the company has bought assets to the tune of Rs 327 Cr, it has sold investments worth Rs 175 Cr, although the line item on the cash flow statement shows this as the purchase of investment. The net cash outflow from investing is Rs 125 Cr, which means that the CFO is not enough to meet this and the company has to raise debt to meet this shortfall. The company has borrowed monies to the tune of Rs 95 Cr to meet this shortfall, and also paid dividends during the year inspite having a negative FCF. The change in cash is Rs 3 Cr as per the statement above, however this needs to be adjusted as the starting point of preparing the cash flows is erroneous.

Final Thoughts

As can be seen from the above example, it is very important to go through the financial statements in detail. For instance in the above case if we were to only look at the final CFO number, we wouldn’t know that the starting point to arrive at the cash flow is erroneous. Other questions which are important also arise – why have the payable to statutory authorities gone up by 3x, payable to employees up by 3.3x? Why is there a sudden jump in balance with government authorities?. Getting an answer to all of these helps in getting a better handle on the business. We can’t emphasis enough the need to go through the financial statements in detail, as just going through the numbers in detail will help us avoiding companies that we shouldn’t be investing in.

We hope that readers would benefit from the above analysis and this would enable them to look at the finer details while going through the cash flow statements in the future. In our next post we will cover the key metric and acquisition accounting shenanigans.

The Financial Shenanigans Series:

- Part 1: Manipulating Revenues

- Part 2: Manipulating Expenses

- Part 3: Those Cash Flows!

- Part 4: Key Metric Shenanigans

- Part 5: Acquisition Accounting

NOTE: As a disclosure some Capitalmind authors may own the above company in their stock portfolios. There is no other relationship between Capitalmind and the above company. Please do not consider this article as a recommendation, It is purely for informative purpose only.