You’ve probably heard enough buzz about India’s premiumisation wave and how the hospitality sector post-COVID has turned into a goldmine, think revenge tourism, a surge in business travel, packed flights, and booming hotel demand.

And while all of that holds true, there’s one business amidst all of this riding the wave , Le Travenues, better known as Ixigo. Now India’s second-largest online travel agency.

In this report, we take a closer look at Ixigo, its journey, business segments, revenue levers, and what lies ahead for the platform in an industry undergoing a travel tech transformation.

Introduction

La Travenues Technology Ltd, more commonly known as Ixigo, was founded in 2007 by Aloke Bajpai and Rajnish Kumar, headquartered in Gurugram. For starters, the company began as a travel search and comparison tool aimed at simplifying travel planning for Indian users.

Its focus on budget travellers from Tier II and Tier III cities, commonly referred to as the mass market or the ‘Bharat’ market is what sets it apart from other OTAs that primarily cater to metro cities.

In 2011, it launched its dedicated flights mobile app, followed by a trains app in 2013 to serve the large railway segment. By 2017, Ixigo became an official IRCTC B2C partner and started facilitating train ticket bookings on its own platform.

In February 2021, Ixigo acquired ConfirmTkt, a Bengaluru-based train booking app, and in August 2021, it bought AbhiBus, a Hyderabad-based intercity bus ticketing platform. It also acquired Zoop in 2024, a train food delivery and e-catering startup.

Presently, it stands as one of the most widely present OTAs in the country, with a presence across flights, trains, buses, and hotels as well.

What Looks Promising?

Though present for almost 2 decades in the industry, there still seems to be significant headroom for strong growth for the business.

Robust Travel and Tourism Market

The Indian Travel and Tourism Market is expected to grow at 9% CAGR till FY28, with Air being the fastest growing at 12% followed by buses, hotels and then the already enormous rail.

*Source: Le Travenues Q4 FY25 Investor Presentation.

*Source: Le Travenues Q4 FY25 Investor Presentation.

While the online penetration is expected to grow across all segments.

*Source: Le Travenues Q4 FY25 Investor Presentation.

*Source: Le Travenues Q4 FY25 Investor Presentation.

OTAs Outpacing the Overall Travel and the Online Markets

India’s total travel market is projected to grow at a 9% CAGR through FY28, while the online segment is expected to expand faster at a 13% CAGR. The share of online bookings is also expected to increase meaningfully, from 54% in 2023 to 65% by FY28, gradually eating into the offline segment.

Building on these shifts in user preference and digital adoption, the OTA market is expected to clock an even faster 18% CAGR during the same period. Within this, bus and air travel are likely to be the fastest-growing verticals, followed by hotels and then rail.

Riding on ‘Bharat’

As briefly discussed earlier, one of the cornerstones of Ixigo’s strategy has been its sharp focus on the mass market, specifically users from Tier II and III cities, at a time when most peers were busy courting the affluent metro crowd.

While India’s air travel market has undoubtedly seen robust growth and holds strong future potential, for the average Indian, travel still largely means railways. We’ve all read growing up that the Indian Railways is the backbone of the country’s transportation system, and Ixigo leaned into that reality. In many ways, it positioned itself as that familiar “uncle” in every neighbourhood or the local travel agent who helps you book train tickets, just made digital.

Cross-Selling Synergy

Ixigo’s presence across all major travel segments in India forms the backbone of a strong cross-selling engine. In its recent concall, the management highlighted deep integration and synergies across its platforms, Ixigo, ConfirmTkt, AbhiBus as a key growth lever. This interconnected app ecosystem allows seamless upselling of value-added services like Travel Guarantee and Price Lock, along with monetisation from hotels, food delivery, and advertising, driving better unit economics across the board.

*Source: Le Travenues Q4 FY25 Investor Presentation.

*Source: Le Travenues Q4 FY25 Investor Presentation.

Notably, as seen in the table above, Ixigo’s Monthly Active Users (MAU) have grown from 63 million in FY23 to 82 million in FY25. Its Monthly Transacting Users (MTU) also rose from 2.13 million to 3.34 million over the same period. The benefits of cross-selling across its ecosystem are clearly visible, with annual spend per transacting user increasing from 6,537 to 9,716 in the last two years.

Now that we’ve covered a brief overview of Ixigo and what’s working in its favour, let’s dig deeper into how the business actually makes money.

Its Business Model

Ixigo’s model brings together all major transport modes into a single platform, or more aptly, an ecosystem for travellers navigating India’s highly fragmented market. This multimodal approach sits at the core of Ixigo’s business model, designed to scale efficiently while driving user stickiness.

That said, one area where Ixigo still trails its peers is hotel bookings and accommodations. The company launched its hotels OTA business only in FY24, making it relatively new to this vertical. In its latest conference call, the management described the hotel segment as nascent but showing promising growth though no specific numbers were disclosed.

With that context, let’s now break down its three primary revenue segments: Trains, Flights and Buses.

Trains Business

For both Ixigo and the broader Indian travel market, trains remain the high-volume backbone. Railways are Ixigo’s historical stronghold—habitual, high-frequency, and deeply ingrained in the travel patterns of its core Tier II and III user base.

Importantly, this large train user base has created organic cross-selling opportunities. For instance, if a user’s train ticket remains unconfirmed, the app can nudge them toward a bus or flight alternative—unlocking additional revenue. This functionality is part of its value-added service (VAS) called Travel Guarantee, which has been fully rolled out across both Ixigo Trains and ConfirmTkt as of Q4 FY25.

Under the train segment, Ixigo has multiple revenue streams—ranging from agent service charges on every ticket booked, to payment gateway fees, value-added services like Travel Guarantee, and in-app advertising.

Flights Business

Now coming to its flights business, this can be viewed as Ixigo’s upsell and premium segment. The company focuses on a relatively underpenetrated flyer base, including many first-time fliers. While flight bookings are less frequent than trains or buses, they come with a higher ticket size. Ixigo also offers value-added services like Ixigo Assured and Assured Flex, along with other ancillaries such as seat selection, travel insurance, and baggage protection. These not only support revenue growth but also improve margins. By FY25, Ixigo has been aggressively gaining share in the flights segment, with air passenger trips rising to 8.44 million from 3.26 million in FY23.

Under the flights segment, Ixigo generates revenue through airline commissions, convenience fees, value-added services (VAS) and ancillaries, as well as advertising.

Bus Business

The bus business can be seen as a high-margin complement for Ixigo. Powered by the AbhiBus acquisition, it has emerged as one of the company’s most profitable segments. Traditionally, the bus category has been low-cost and highly price-sensitive. However, Ixigo’s leverage of AbhiBus’s direct integrations with private bus operators and state transport corporations has helped secure better inventory and pricing.

This, combined with cross selling from train users (suggesting a bus when train tickets are waitlisted), makes the bus segment a high margin engine.

Under its bus segment, the revenue streams are convenience fees, operator commissions, VAS, SaaS and Advertising.

In FY25, while buses contributed the least to overall GTV, they delivered the highest take rate among the three segments. With that, let’s walk you through some key numbers. But before we dive in, here’s a quick refresher on a few terms we’ll be using

Gross Transaction Value (GTV):

This is the total value of all bookings made on Ixigo’s platform whether for trains, flights, or buses. It reflects how much customers are spending through the app.

Take Rate:

This is the share of GTV that Ixigo earns as revenue. For example, if a ₹1,000 ticket is booked and Ixigo earns ₹50 from it, the take rate is 5%.

Contribution Margin (CM):

This shows the profit Ixigo makes after covering the direct costs of each booking (like commissions and payment gateway fees). It tells how efficiently the core operations are running.

Note: CM is not the same as EBITDA margin, it doesn’t include indirect costs like salaries, office rent, or marketing expenses.

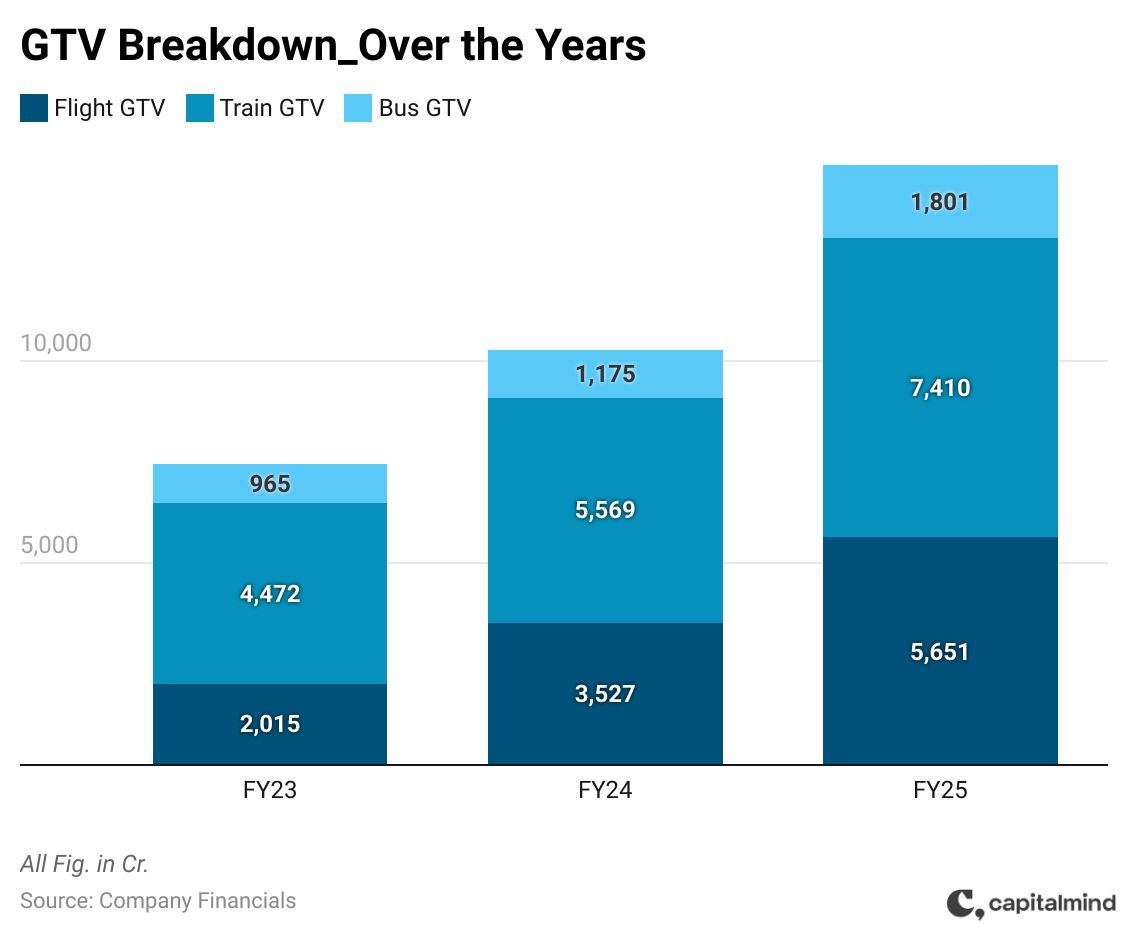

Ixigo’s GTV has grown at almost 40% CAGR over the last three fiscals, with all three segments contributing meaningfully, flights grew by 67%, trains by 28%, and buses by 36% over the same period.

Ixigo’s GTV has grown at almost 40% CAGR over the last three fiscals, with all three segments contributing meaningfully, flights grew by 67%, trains by 28%, and buses by 36% over the same period.

Also evident in the chart above, trains remain the largest contributor to GTV, followed by the high-ticket flights business, with buses coming in third.

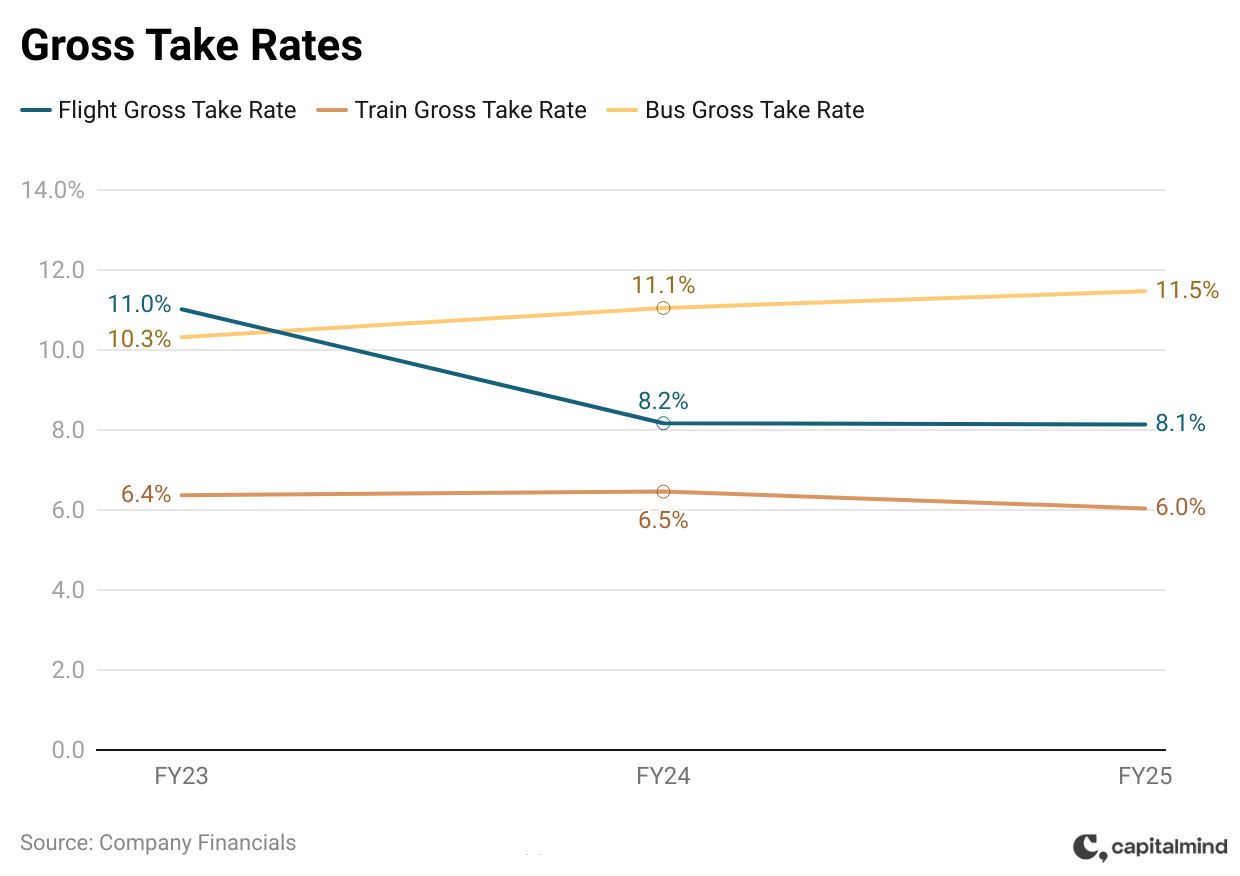

Now, coming to take rates. Ixigo’s flight business take rates have declined from 11% in FY23 to 8.1% in FY25. The management attributes this to deliberate steps taken over the past few years to become more competitive and gain market share. This included lowering convenience fees, offering customer incentives, and reducing pricing on value-added services, all of which weighed on per-transaction margins.

Now, coming to take rates. Ixigo’s flight business take rates have declined from 11% in FY23 to 8.1% in FY25. The management attributes this to deliberate steps taken over the past few years to become more competitive and gain market share. This included lowering convenience fees, offering customer incentives, and reducing pricing on value-added services, all of which weighed on per-transaction margins.

As mentioned earlier, Ixigo caters to a more mass-market audience with lower average ticket sizes. So even if the absolute earnings per booking remain similar, the take rate naturally compresses as GTV rises. To offset this, Ixigo is doubling down on ancillary revenues like price lock, insurance, and seat selection, while actively leveraging AI to improve ‘Attach rates’ – the percentage of users opting for these add-ons.

Its train business take rates have remained steady in the 6–6.5% range.

Moving to its bus business, which we previously described as the margin complement, has seen its take rates improve notably from 10.3% in FY23 to 11.5% in FY25. This uptick has been driven by a greater contribution from private operators, the introduction of value-added offerings like Abhi Assured, and AI-led dynamic pricing to enhance ancillary revenue. Additionally, its fixed CAPEX model supports further margin expansion.

Now let us see how the composition of its contribution margin evolved over time.

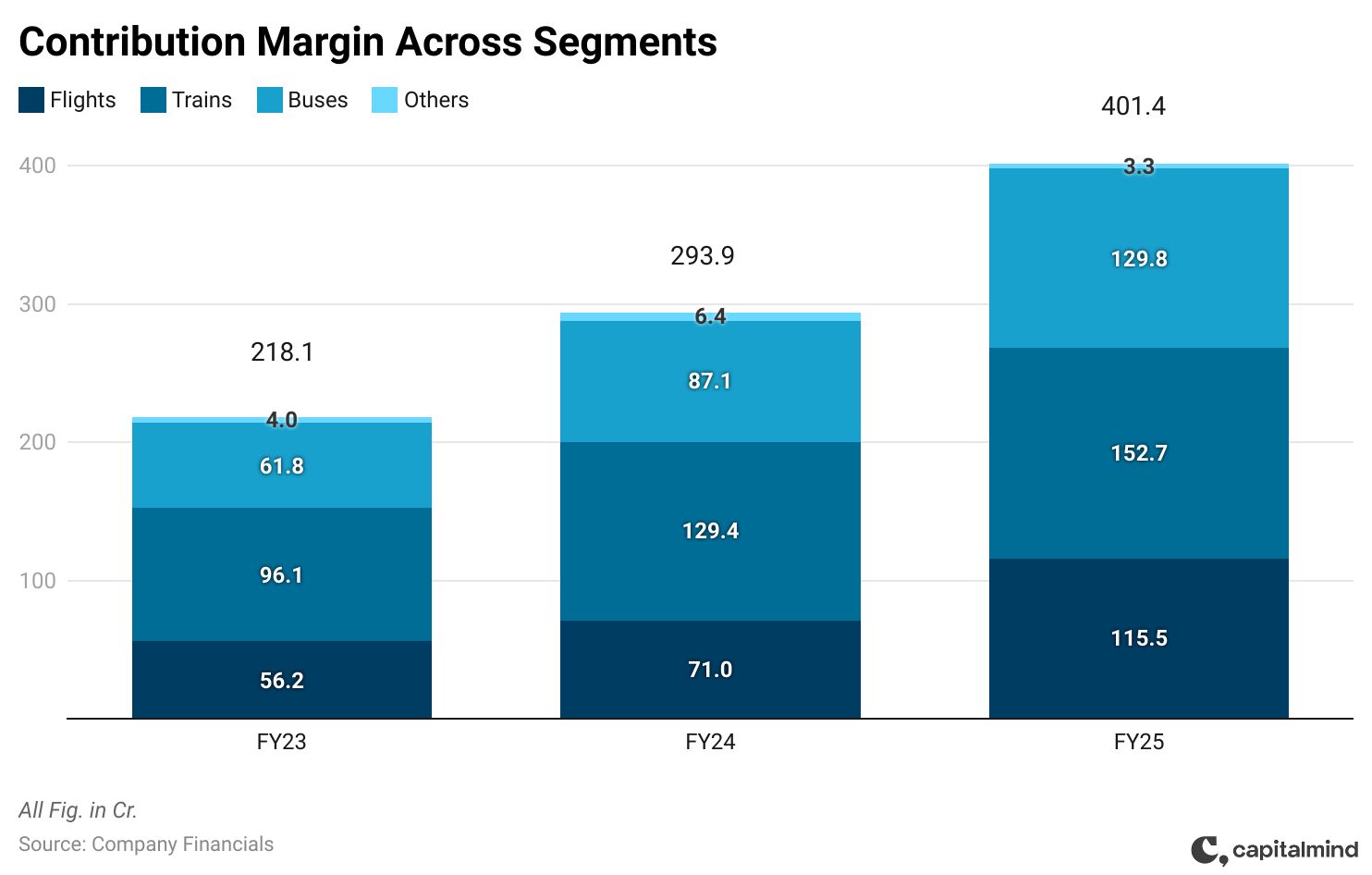

Ixigo’s absolute contribution margin has grown at a healthy 36% CAGR between FY23 and FY25. As expected, the bus segment led the growth with a 45% CAGR, followed closely by the flights segment at 43%. However, despite the higher growth in other segments, trains continue to be the largest contributor to contribution margin on the back of its sheer volume and consistently strong GTV.

Ixigo’s absolute contribution margin has grown at a healthy 36% CAGR between FY23 and FY25. As expected, the bus segment led the growth with a 45% CAGR, followed closely by the flights segment at 43%. However, despite the higher growth in other segments, trains continue to be the largest contributor to contribution margin on the back of its sheer volume and consistently strong GTV.

Now that we’ve explored Ixigo’s business model, its key segments, revenue drivers, and margin dynamics, let’s take a quick look at the broader picture by running through its company-wide financials.

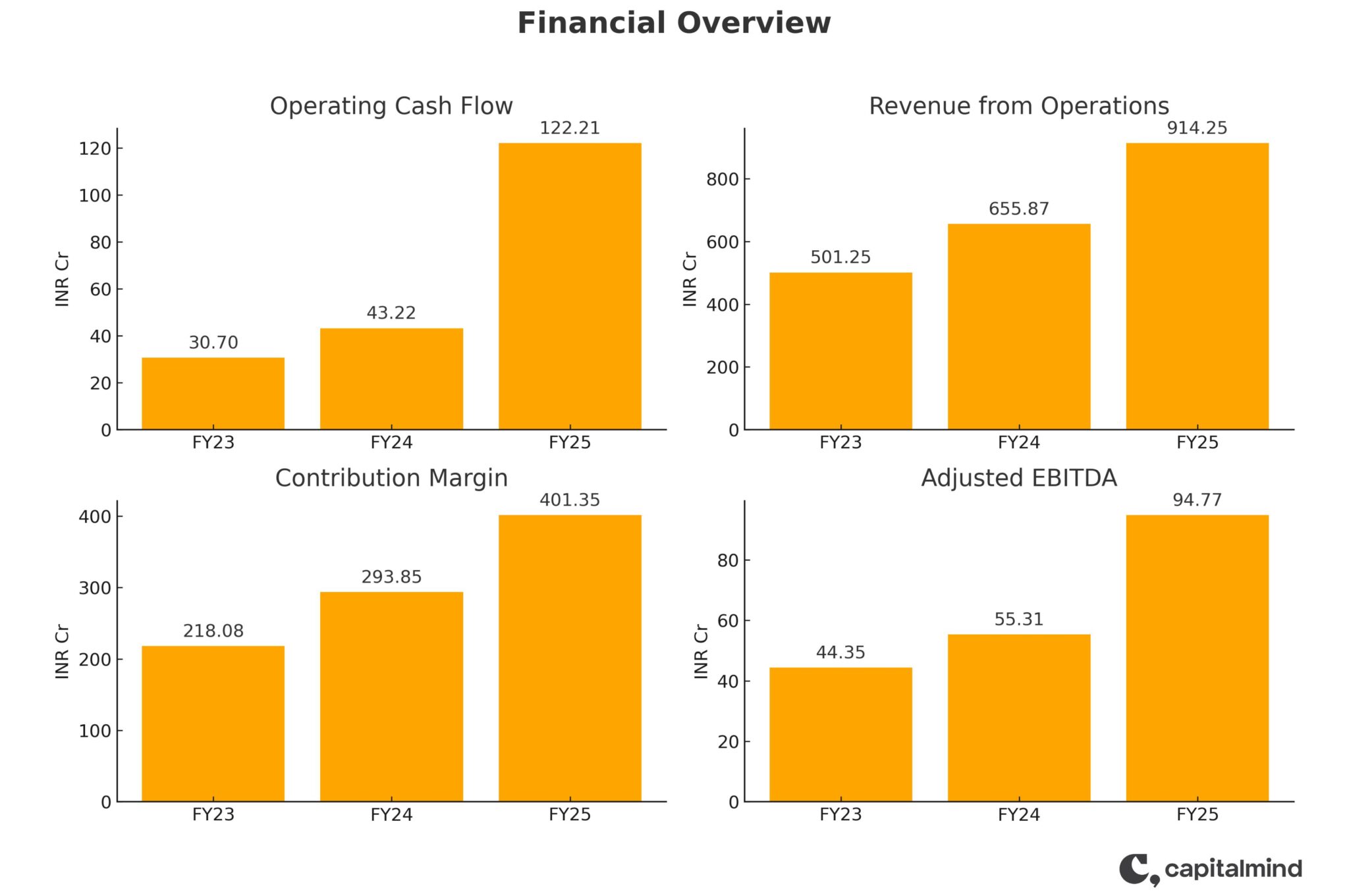

Ixigo’s revenues have nearly doubled since FY23, reaching 914 Cr in FY25. Trains led the revenue mix at ~50%, followed by flights (~28%) and buses (~21%).

Ixigo’s revenues have nearly doubled since FY23, reaching 914 Cr in FY25. Trains led the revenue mix at ~50%, followed by flights (~28%) and buses (~21%).

Operating leverage has clearly begun to show, with operating cash flows jumping 182% YoY to 122 Cr in FY25. Contribution margin and adjusted EBITDA have also scaled well, growing at ~36% and ~46% CAGR respectively over FY23–FY25.

In terms of its ESOP expenses, the management mentioned that it expects it to stay within the 20 Cr mark (FY25 ESOP expenses stood at 14 Cr), though it may inch higher with the roll out of a new target-based plan approved by shareholders. However, the new plan will only kick in once certain market cap thresholds are met. It includes filters like a 30-day VWAP, market cap, and time-based conditions.

With that, while Ixigo appears well positioned in India’s rapidly growing travel market, there are a few challenges that are worth keeping an eye on.

What Could Go Wrong? Key Challenges for Ixigo.

Intense Competition

The Indian OTA space remains intensely competitive, with well-funded players like MakeMyTrip (including its Goibibo brand), Yatra, EaseMyTrip, and Cleartrip all battling for market share. Each brings its own strengths, MakeMyTrip dominates in hotels and holiday packages, while Yatra has a stronghold in corporate travel. Even in trains and buses, where Ixigo holds a leadership position, it faces competition from IRCTC’s own platform and other travel aggregators.

Dependence on Partners and Suppliers

Ixigo’s train ticketing business is built on a non-exclusive agreement with IRCTC, recently renewed till April 2028. While it grants Ixigo principal service provider status, IRCTC is free to partner with competitors and can terminate the agreement if terms are violated. This, coupled with dependence on external partners like airlines and bus operators, exposes Ixigo to margin and operational risks. Maintaining strong relationships and consistently adding value will be key to defending its position.

Regulatory and Policy Risks:

Ixigo faces regulatory and policy risks that could affect its margins and operations. Caps on convenience fees, stricter refund rules, or mandates to share revenue with government bodies could dent profitability. Travel is also vulnerable to external shocks like visa changes or geopolitical tensions as seen in 2025 when Ixigo suspended certain international bookings. Staying compliant and agile is crucial in navigating such disruptions.

Limited Presence in Hotels:

Hotels remain a weak spot for Ixigo. Unlike rivals with years of experience and deep hotel inventories, Ixigo only launched its hotel booking platform in late 2023. This limits its appeal to users seeking complete travel bundles (like flights + hotels). Bridging this gap will require significant investment and time, but also presents a key growth opportunity.

Broader risks like sustaining profitability, executing growth plans effectively, and navigating macroeconomic or external shocks apply to Ixigo like any other business. However, the risks discussed above are more specific to the space and model in which Ixigo operates.

Current Outlook and Valuation

Ixigo delivered a strong performance in FY25:

- GTV neared 15,000 Cr, growing ~45% YoY

- Revenue rose ~40% YoY to 914 Cr

- EBITDA surged ~86% YoY to 99 Cr

- Annual active users increased from 480 Mn to 544 Mn

- Annual spend per user improved from 8,539 to 9,716

Ixigo now stands as India’s second-largest OTA, behind only MakeMyTrip. More notably, it’s growing faster than its peers, MMT grew GTV by 23% YoY, while EaseMyTrip and Yatra posted marginal to negative growth at 2% and –7% respectively, indicating the company is meaningfully outperforming market growth.

Valuation Check: Premium, But Justified?

As per FY25 numbers and current market pricing, Ixigo trades at a steep PE of 119x, compared to EaseMyTrip (36x) and Yatra (40x). While this premium is notable, it reflects Ixigo’s strong outperformance in GTV and revenue growth, which the market has already priced in.

Looking ahead, we estimate Ixigo’s topline to reach 1,500 Cr by FY27, implying a ~28% CAGR, with PAT margins stable around 7%. On these assumptions, the stock would trade at a forward FY27E PE of ~68x and a PEG ratio of ~2.1, still elevated, though relatively more palatable.

That being said, whether this valuation holds will depend on a few key levers:

- Can Ixigo sustain its multi-modal growth momentum?

- Will margin tailwinds from the bus segment continue?

- Can its value-added services consistently drive incremental revenue?

India’s travel market is clearly on an upswing, and Ixigo is well-positioned at the intersection of this trend. But how well it executes from here will decide whether the premium it commands today turns out to be persistent or premature.

Disclosure: I, Sidhanth Paul, Research Analyst, author, and the name subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific view(s) in this report.

Research Analyst or his/her relative or Capitalmind Research LLP does not have any financial interest in the subject company. Also, the Research Analyst, his relative, Capitalmind Research LLP, or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further, Research Analyst or his relative or Capitalmind Research LLP or its associate does not have any material conflict of interest at the time of publication of this research report.

Also, LeTravenues Technology Ltd is not a part of our Capitalmind Premium Portfolios. This article is intended solely for informational purposes and should not be considered as an investment recommendation.

Capitalmind Research LLP is a SEBI Registered Research Analyst, having registration no. INH000014003.

Additional Reads: