A part of India is getting richer, and it’s happening faster than ever!

There are multiple data points that have led me to make the above statement. Whether it’s the growing number of HNIs & UHNIs in the country, the growing number of tax filers with incomes over 1 Cr, or the robust asset growth in mutual funds and alternative investments, all things hint towards Indians getting richer.

For context, the 360 One Wealth Hurun India List 2023 reported that the number of Ultra High Net Worth Individuals (UHNIs) in India with assets exceeding 1,000 Cr, reached 1,319, reflecting a notable yearly increase of 216.

*Source: 360 One’s FY24 Annual Report.

*Source: 360 One’s FY24 Annual Report.

The same report also gave an interesting insight into the fact that wealth creation in India has undergone a significant shift and is not limited to tier-1 cities only. In the last decade, the number of Indian cities on the rich list has surged from 10 to 95.

Below is a snippet showing growth in the number of UHNIs across the top 20 cities in India. Surprisingly, the list is topped by Udaipur, followed by Vadodara and then Surat.

*Source: 360 One’s FY24 Annual Report.

That being said, projections suggest that the number of HNIs and UHNIs in our country will grow at a CAGR of 15.7% and 9.6% respectively by 2027.

*Source: Anand Rathi’s FY24 Annual Report

*Source: Anand Rathi’s FY24 Annual Report

Rising No. of Wealthy Tax-Payers

Another interesting data point strengthening our rationale is that the number of income tax filers with income > 1 Cr has more than doubled in the last 5-7 years from ~68,000 in FY17 to ~1,70,000 in FY23.

Growing Market Size

Growing Market Size

According to McKinsey, the cumulative financial assets of Indian households (HNI and UHNI combined) stood at around 1.2 trillion as of CY23. This figure is projected to grow to approximately 2.2 trillion by CY28, with a CAGR of 13-14%.

*Source: 360 ONE Q1 FY25 Investor Presentation.

*Source: 360 ONE Q1 FY25 Investor Presentation.

AMC Industry on a roll

India’s overall asset management industry has been on a roll. There has been significant growth across mutual funds and alternative investments (PMS and AIF).

FY24 was a stellar year for domestic mutual funds, with AUM growing to 53 trillion. The same growth also sustained into FY25, with its AUM as of August already hitting the 66 trillion mark.

PMS and AIFs have also kept pace, with PMS assets growing to ~9 trillion and AIFs at ~4 trillion, along with commitments worth 11 trillion, signaling further growth potential.

That being said, we all understand that as Indians, savings as a concept is deeply ingrained in us. However, investing those saved income into financial assets like stocks, mutual funds or PMS and AIFs for the wealthier is a fairly new phenomenon.

Hence, despite the significant rise in interest in these assets lately, they still have a lot of ground to cover as compared to more matured markets.

*Source: Nuvama’s FY24 Annual Report.

*Source: Nuvama’s FY24 Annual Report.

Direct equities and mutual funds have consistently accounted for only 10-13% of India’s financial portfolio, highlighting an extensive pool of potential asset growth.

*Source: Anand Rathi’s FY24 Annual Report

*Source: Anand Rathi’s FY24 Annual Report

Looking at all the factors we have discussed in consolidation highlights a huge white space to cater and that is where wealth management comes in.

To put it simply, there is more money to manage in the Indian market than there has ever been and it’s only expected to grow further. Hence a growing opportunity for wealth management companies to have a share of the growing pie.

Things you should know about the wealth management space:

Mode of Revenue

A wealth management firm can make money majorly through two routes.

- Recurring Based – It’s the predictable and regular source of income for the firm. Example – Management fee, Advisory Fee (Fixed or % of AUM), Trail based commission, etc.

- Transaction-Based– It’s the one-time income a firm makes for facilitating a transaction. Example – Brokerage fee for executing a trade.

Wide Array of Players

The wealth management sector in India is dynamic and fast-growing, with multiple players eyeing the pie.

- From a target market perspective, a firm could either focus on UHNIs (360 One), the mid-market (Anand Rathi), or a mix of both (Nuvama Wealth).

- From a service offering perspective, some firms may purely function as distributors (Anand Rathi) or a mix of both manufacturing and distribution (360 ONE).

- From a fee perspective, a firm might either operate on a direct advisory fee or on a pure distribution commission model, or a mix of both.

It’s a Fairly Cyclical Business

Though the sector looks well poised for significant growth, it still is a cyclical business. The net flow is largely dependent on market sentiments and how the markets have done in recent times (MTM gain).

Pure play wealth management business seems to be more cyclical as AMC’s usually make money on an AUM basis.

Compressing Yields

With regulatory changes such as the Total Expense Ratio (TER) for mutual funds and trail-based commissions for PMS/AIFs, there’s growing pressure on yields from recurring assets.

Additionally, the increasing popularity of the advisory model, as more investors opt for direct products, seems to be contributing to this yield compression.

Now, let’s dig deeper and dissect the following wealth management businesses, trying to find out which we like better –

- 360 ONE WAM Ltd.

- Nuvama Wealth Management Ltd

- Anand Rathi Wealth Ltd

360 ONE WAM Ltd.

360 ONE WAM Ltd, previously known as IIFL Wealth Management Ltd is one of the biggest wealth and asset management companies in India. Their offerings cover a wide range of products from wealth to asset management and lending solutions as well.

Its business could be broadly classified into two verticals-

- Wealth Management

- Asset Management

Wealth Management

Its wealth management vertical, also called 360 ONE Wealth is quite diversified in itself. As of H1 FY25, the total AUM under this vertical grew to 3,19,000 Cr while servicing more than 7,500 clients.

Let’s break it down further.

360 One Plus

360 One Plus provides portfolio solutions to its clients either through discretionary, non-discretionary or advisory propositions. Its offerings range from direct equities to managed solutions (Mix of MFs & ETFs) as well as bespoke solutions that offer customized portfolios in adherence to acceptable instruments and selected investment approaches.

Lending

It also offers lending solutions to its clients for their short-term capital requirements. As of Q1 FY25, its loan book is at 6,845 Cr with having serviced over 1000 clients.

Product Distribution

It is also in the distribution business with strong brokerage capabilities across equities, fixed income, commodities, and currencies. It has ~230 + RMs with a presence across 23 cities.

Transaction & Broking Services

360 ONE also provides research-based broking services across various asset classes to its clientele.

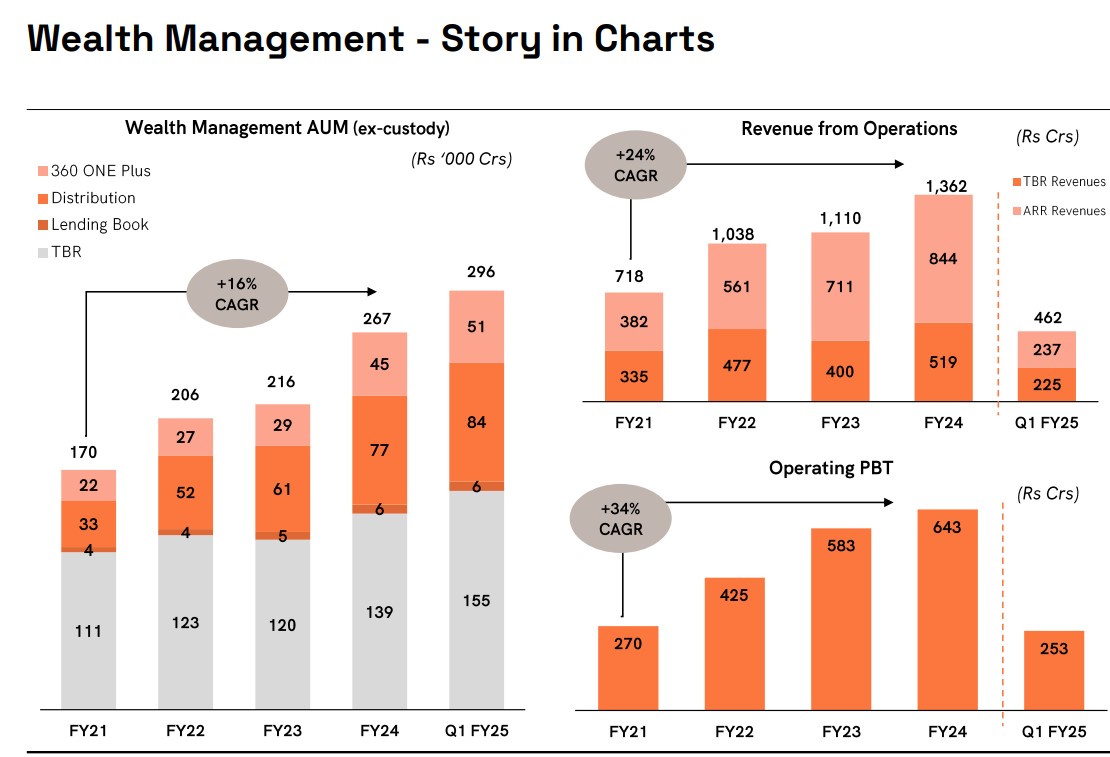

*Source: 360 ONE Q1 FY25 Presentation.

Its overall asset book (excluding custody) has grown at a 16% CAGR over the last four years. Notably, transaction and broking (TBR) services have consistently accounted for over 50% of its total AUM.

The fastest-growing segment in terms of assets is its distribution business, expanding at a 33% CAGR, followed by 360 ONE Plus at 27%. The lending book remains a small portion of the overall asset base.

In terms of revenues, the topline has grown at 24% CAGR during the same period, with Annual Recurring Revenue (ARR) growing impressively at 30% CAGR.

Given the yield pressure on recurring assets (especially in advisory), we like its mix of transaction and recurring income.

Tapping Newer Segments

360 ONE in its course of action till now has majorly catered to the diverse wealth management requirements of UHNIs. But, now with the country’s capital markets seeing enormous interest from retail investors, the company also wants to have a share of the affluent(HNI) and the mid-market segments.

With that it is also getting into global business, leveraging its already existing capabilities to cater to Indian families across borders for their global wealth pools. The management in its recent conference call said it’s on track for this segment to be live by the end of September.

Now coming back to the mid-market segment, to strengthen its position, 360 ONE has also announced the acquisition of ET MONEY, a fintech platform focused on wealth advisory.

The acquisition is subject to regulatory approvals, 360 ONE will acquire 100% of ET MONEY via a stock and cash deal.

- ET MONEY has 9 lakh + transacting clients with more than 1 lakh revenues generating users.

- It tracks an overall AUM of ~70,000 Cr. The AUM invested through its platform is around 28,000 Cr, out of which MFs constitute more than 25,000 Cr.

- ET MONEY Genius, which is its advisory arm, has more than 76,000 active paying clients with an AUM of 1,200 Cr.

All in all, the platform offers significant synergies with 360 ONE, strengthening its position to capture the rapidly growing 10 lakh to 1 Cr segment.

*Source: 360 ONE Q1 FY25 Presentation.

*Source: 360 ONE Q1 FY25 Presentation.

In its recent conference call, the management also said that it has already for 45 RMs (Relationship Managers) for the mid-market segment, 10 of which are dedicated for sales.

The total number of RMs for the mid-market segment is expected to come to 75 by the end of this year.

Asset Management

Its asset management vertical, also called 360 ONE Asset, offers three products: Mutual Funds, PMS, and AIFs. Its funds are uniquely positioned from seed stage to pre-IPO, credit, real assets, etc.

*Source: 360 ONE Q1 FY25 Presentation.

*Source: 360 ONE Q1 FY25 Presentation.

As of H1 FY25, the total AUM for its asset management vertical reached 85,770 Cr. It has also consistently increased its distribution coverage with more than 33,000 partners (added 2,000 partners in FY24).

*Source: 360 ONE Q1 FY25 Presentation.

*Source: 360 ONE Q1 FY25 Presentation.

As of FY24, PMS forms ~50% of its AUM and has had that proportion in its asset book throughout. Its fastest-growing segment is mutual funds, growing at 129% CAGR over the last 4 years, followed by PMS growing at 73%, and then AIF at 54%.

Its total revenue during the same time has grown at 75% CAGR to 496 Cr, out of which ARR was 483 Cr. While operating profits grew at 106% CAGR.

Below is a consolidated view of 360 ONE WAM:

- Its cumulative AUM has grown at ~24% CAGR from FY 21-24, whereas the ARR AUM has comparatively grown at a faster rate of ~28% CAGR.

- Coming to the topline, its consolidated revenues from ARR & TBR have grown at ~26% CAGR during the same period.

- As said previously too, we like its mix of transactional and recurring revenues as TBR is highly dependent on market sentiments, while ARR gives stability.

- Its cost to income has also come down by ~5% to 48.7% in FY24.

- Its PAT also grew handsomely to 802 Cr in FY24.

Nuvama Wealth Management Ltd.

Nuvama Wealth Management is one of India’s largest and most diversified wealth management firms. In addition to its wealth and asset management verticals, it operates a capital markets business offering services such as brokerage, custody, and investment banking.

Up until 2021, Nuvama was part of the Edelweiss Group, after which it was acquired by PAG, a leading Asia-focused alternative asset manager with over ~46 lakh Cr in assets across private equity, real assets, credit, and markets.

The business has 3 verticals:

- Wealth Management

- Asset Management

- Capital Markets

Wealth Management

Its wealth management vertical is further divided into two, namely –

- Nuvama Wealth (Affluent & HNI category)

- Nuvama Private (UHNI Category)

Nuvama Wealth

Nuvama Wealth caters to the HNI and affluent category (including SME business owners & salaried individuals). It offers a diverse range of investment solutions across various asset classes with a combination of third-party and proprietary products.

As of FY24, its AUM surged to 77,930 Cr, achieving a 33% CAGR over the last 4 years.

Its revenues during the same period have grown at a ~35% CAGR to 669 Cr while operating profits have grown at 106% CAGR.

*Source: Nuvama Q1 FY25 Presentation.

*Source: Nuvama Q1 FY25 Presentation.

By the end of H1 FY25, its AUM had further increased to 1,00,060 Cr, driven by a 39% YoY growth in MPIS (Managed Products & Investment Solutions) and MTM gains on other assets. MPIS contributed 86% of total new flows in FY24.

The company has heavily invested in the last 12 months to increase the number of RMs (Relationship Managers) by 337 and expand its network of external wealth managers by more than 2000.

It presently has more than 1,200 RMs and ~7000 EWMs (External Wealth Managers) covering 450+ locations (including 70 Nuvama branches).

Below is a snippet showing the revenue composition by solutions as well as by channels. This should give you some more insight.

*Source: Nuvama Q4 FY24 Presentation.

*Source: Nuvama Q4 FY24 Presentation.

In terms of solutions, MPIS forms a major chunk of its revenues (52% in FY23 & 48% in FY24), followed by NII from loans, then followed by brokerage.

MPIS is expected to remain the key growth driver for Nuvama Wealth’s vertical moving forward. However, given that most of the managed products are now annuity-based (trail-based), the contribution to the topline is anticipated to grow meaningfully as the accumulated trail increases with the addition of assets over time.

Now looking at revenue by channel, over 70% of Nuvama’s revenue is generated through its relationship managers, demonstrating the importance of direct client engagement in this space.

Nuvama Private

Nuvama Private is the arm of its wealth management vertical which caters to the UHNI category through a range of solutions like investment advisory, managed accounts, bespoke solutions, wealth restructuring, credit, etc.

Nuvama private is the vertical, that is directly comparable to 360’s wealth business as both service the UHNI category.

As of FY24, its AUM reached 1.69 lakh Cr growing at 20% CAGR in the last 4 years. This number has already grown to 2.05 lakh Cr by the end of H1 FY25.

Its revenue has also grown at ~35% CAGR to 519 Cr in FY24 while operating profits grew at 79% CAGR.

*Source: Nuvama Q1 FY25 Presentation.

As of H1 FY25, the number of RMs has grown to 127, servicing more than 4050+ families. Nuvama Private has added 4 new cities beyond Tier 1 in the last 12 months, considering the growing numbers of UHNIs in India outside Tier 1 cities.

The company is also looking to leverage its onshore capabilities to build a global wealth platform. The value proposition is to serve UHNI clients looking to diversify its wealth pool or already have a global wealth pool.

Also, Indians residing abroad, looking to allocate to Indian opportunities. It has received final approval from DIFC (Dubai International Financial Center) for Dubai in July 2024. *Source: Nuvama Q4 FY24 Presentation.

*Source: Nuvama Q4 FY24 Presentation.

Referring to the above table, in the last 2 financial years, ~75% of Nuvama’s assets came from transactional assets whereas in terms of revenue, it’s about a 55:45 % split between ARR and Transaction assets.

Asset Management

Nuvama launched its asset management business in 2021, majorly focusing on alternative investment strategies across private markets, public markets and commercial real estate.

As of H1 FY25, its AUM reached 10,288 Cr, of which 79% i.e.,~8,113 Cr is fee-paying. It has 8 active strategies, presently with a team of 20+ investment professionals.

It distributes both in-house and has tie-ups with 20+ distributors.

*Source: Nuvama Q1 FY25 Presentation.

At the current scale, its AMC business is loss-making. However, with improving scale and synergies from its other verticals, it should contribute meaningfully to both the revenues as well as profits.

Capital Markets

Nuvama’s capital market vertical can be classified into asset services (clearing and custody), institutional equities, and investment banking.

Asset Services- Under this, Nuvama offers a range of services like fund-setup advisory, securities custody, derivatives clearing, and reporting.

Institutional Equities- It provides research and trading solutions to over 700 domestic and global clients, including long-only funds, hedge funds, mutual funds, insurance companies, and family offices.

Investment Banking- It has 20 years of experience as a full-service investment bank. It offers solutions across equity capital markets, debt capital markets, and advisory services (private equity and M&As).

IE & IB both are volatile businesses, being dependent on market sentiments. However, the capital markets vertical formed 39% of revenue in FY24.

Hence any volatility in market sentiments could hamper the company’s topline and profits. This is where its asset services arm comes in to give some cushion as it’s relatively sticky.

The AUM from its asset services has grown significantly at 50% CAGR from FY21-24, to ~92,000 Cr by FY24, with 109% YoY growth coming in FY24, thanks to robust capital markets.

Additionally, its Investment Banking division has a natural synergy with the wealth vertical, creating substantial cross-selling opportunities. According to the management in a recent concall, 40% of relevant client deals in the past 12 months have transitioned into private wealth relationships.

*Source: Nuvama Q1 FY25 Presentation.

*Source: Nuvama Q1 FY25 Presentation.

Referring to the table above, asset service revenues have grown at 25% CAGR between FY21-24, while IE & IB growth is comparatively subdued at 12% CAGR for the same period. The same is true for operating profits as well.

Here is a consolidated view of Nuvama:

- In FY24, Nuvama saw its revenues grow by 31% YoY, with capital markets being the fastest-growing segment, driven by strong capital markets, followed by asset management and wealth.

- In terms of revenue composition, wealth management remained the largest contributor, accounting for ~57% of FY24 revenues, while capital markets contributed 39%. The asset management business, though growing, hasn’t yet made a significant contribution.

- Despite a reduction in the cost-to-income (C-I) ratio to 62% in FY24, it remains high due to a subscale AMC business and a significant reliance on capital markets.

- Here’s the AUM breakdown:

Wealth Management: 3.5 lakh Cr

Asset Management: 10,288 Cr

Asset Services: 1.25lakh Cr

- Within its wealth management vertical, Nuvama Private represents ~68% of the total AUM, with 20% consisting of ARR-earning assets. However, wealth forms a larger part of revenues for this vertical, ~56% in FY24.

- Meanwhile, 81% of its AMC AUM is fee-paying, contributing to recurring revenue.

Anand Rathi Wealth Ltd.

Anand Rathi Wealth (ARWL) was established in 2002, becoming an AMFI-registered Mutual Fund distributor. Over the years it has become one of the leading wealth solution providers in the country.

It predominantly focuses on the HNI or mid-market segment (individuals with net worth between 5 – 50 Cr). Its total AUM across products as of FY24, grew to ~59,000 Cr catering to 9,911 active client families.

*Source: ARWL FY24 Annual Report.

*Source: ARWL FY24 Annual Report.

In terms of product offerings, the business provides a range of solutions, including equity MF, debt MF, and NSP (Non-Principal Protected Structured Products), alongside services like tax and estate planning.

NSPs are customized products designed to meet specific client needs within accepted asset classes. Over the past 11 years, ARWL has distributed more than 3,200 products, with over 1,400 having matured. Notably, 100% of the matured products have successfully returned the principal.

By the end of H1 FY25, ARWL’s AUM reached ~₹75,000 crore, driven by a net increase of 1066 active clients during the first half, bringing the total to 10,977.

Equity MFs are the largest contributor to ARWL’s asset book, accounting for 55% of the total. Net inflows for the first half have shown impressive growth, surging 128% YoY.

Equity MF net inflows have grown by 64% YoY, driven largely by the robust performance of capital markets over the past year. This reflects the growing interest among investors, with more individuals viewing mutual funds as a go-to option for its wealth management solutions.

It has added 63 RMs in the last 12 months, taking the total count to 374. Its client attrition has also consistently remained in the 0.1% – 0.2%, signaling greater stickiness which is important in a distribution-centric wealth management business.

New Businesses

Digital Wealth

Under its digital wealth vertical, ARWL aims to leverage human expertise through a phygital model, focusing primarily on the mass affluent category (10 lakh – 5 Cr).

As of H1 FY25, the total AUM under this vertical reached 1,826 Cr, up from 1,387 Cr a year back. The total number of clients also grew from 4,475 to 5,454 during this period.

Omni Financial Advisor (OFA)

OFA is a digital platform, which runs on a B2B2C model, designed to help mutual fund distributors manage client relations and grow their businesses using digital solutions. It follows a subscription model, granting access to both distributors and clients.

As of H1 FY25, total assets on the platform grew by 31% YoY, reaching ₹1.55 lakh crore. The number of mutual fund distributors increased to 6,188 from 5,880 a year earlier, while the number of clients grew to 1 lakh, bringing the total to 21 lakhs.

Best bet in the wealth management space?

By now, you must have gotten a good brief about all three companies and how each fits into the wealth management landscape.

While the businesses have similarities, they are also very different in their ways. In terms of preference, we like 360 ONE and Nuvama, better than Anand Rathi.

ARWL is a robust company with significant growth potential going forward. However, it’s a pure distribution business and not a manufacturer like the other two. Also, as talked about earlier, both 360 ONE and Nuvama are also into asset management providing them some more stability.

And, hence, 360 ONE and Nuvama provide a better business mix, than Anand Rathi.

360 ONE WAM vs Nuvama Wealth

The table below compares the proportion of recurring revenue of 360 ONE Wealth and Nuvama Private, both majorly servicing the UHNI category.

Note: This comparison only includes Nuvama’s Private vertical which focuses on the UHNI category.

As discussed earlier, there has been an increasing yield pressure on recurring assets while transaction-based revenues though volatile, help in profitability.

There is a visible trend of increasing the proportion of revenue from recurring assets for both businesses. However, 360 ONE seems to have a higher proportion of ARR.

We like 360 ONE’s emphasis on increasing its recurring asset base which gives stability while maintaining a healthy proportion of transaction-based revenue too.

Let us now look at the retention numbers. It is the percentage of total AUM, retained by the company as its revenue.

360 ONE Wealth’s ARR retention has declined from 0.83% in FY21 to 0.78% in FY24, likely due to the growing proportion of advisory in its asset book and lending forming only ~2.5% of it.

360 ONE Wealth’s ARR retention has declined from 0.83% in FY21 to 0.78% in FY24, likely due to the growing proportion of advisory in its asset book and lending forming only ~2.5% of it.

On the other hand, Nuvama Private’s ARR retention improved significantly to 0.95% in FY23, though it slightly dropped to 0.89% in FY24. This better retention is primarily driven by a higher proportion of lending in its asset mix.

However, while higher lending boosts ARR retention, it also increases capital consumption, which could dampen profitability.

Now, comparing the retentions from recurring assets of the AMC vertical of both businesses.

As we have said throughout this report, yields are under pressure in the pure-play wealth management space and an AMC business would bring stability, while also being a key factor in profitability.

The asset book of Nuvama’s AMC is very small in comparison to that of 360 ONE’s. As of Q1 FY25, 360 ONE Asset’s total AUM reached ~79,600 Cr, whereas Nuvama’s AUM is at ~7,600 Cr.

However, it is expected to grow significantly in the next few years, with the management targeting to add 3,500-4,000 Cr AUM by this year.

Let’s Conclude

Now let’s have a consolidated view of both businesses.

Nuvama’s AUM has grown at an impressive ~30% CAGR from FY21 to FY24, while 360 ONE has a slightly lower growth rate of 24% CAGR over the same period. However, it’s important to note that as of FY24, Nuvama’s Capital Markets segment contributes around 26% of its asset book. In contrast, 360 ONE’s total AUM is derived exclusively from its Wealth Management and Asset Management segments, making its asset base more focused on wealth advisory and investment management.

The same is the case in terms of revenue growth, Nuvama’s revenue has grown at 27% CAGR, in comparison to 21% of 360 ONE. However, capital markets contributed 39% of Nuvama’s FY24 revenues.

360 ONE also has more than double the number of RMs compared to Nuvama. Yet, the client-per-RM ratio remains quite comparable at 30 and 32 for 360 ONE and Nuvama, respectively.

In terms of cost-to-income ratio, 360 ONE shows far more efficiency when averaging over the past three years. This can be attributed to Nuvama’s higher share of capital markets, which comes with higher fixed costs, and its subscale AMC business.

Overall, if you are looking for a pure play on Wealth Management, 360 ONE WAM is a better choice. However, if you would like to have exposure to Capital markets as well, Nuvama Wealth looks good because of its stronger business mix, with all its revenue stemming either from wealth management or asset management, a higher proportion of recurring assets, strategic acquisitions, and newer business segments.

360 ONE’s entry into the HNI segment positions it well for growth, especially considering the rapid increase in the number of HNIs in India. Additionally, its acquisition of ET Money is a strategic move that enhances its ability to capture the affluent market. Also, Nuvama’s AMC business is still subscale, with an AUM of about 10% of 360 ONE’s.

From a valuation perspective, Nuvama trades at a lower PE (TTM) of 28x, compared to 360 ONE at 39x.

That being said, Nuvama also has a strong business with clear growth drivers. However, we prefer 360 ONE for the above reasons.

Disclosure: I, Sidhanth Paul, Research Analyst, author, and the name subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific view(s) in this report.

Research Analyst or his/her relative or Capitalmind Research LLP does not have any financial interest in the subject company. Also, the Research Analyst, his relative, Capitalmind Research LLP, or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further Research Analyst or his relative or Capitalmind Research LLP or its associate does not have any material conflict of interest at the time of publication of this research report.

Also, Nuvama, 360 One and Anand Rathi are not a part of our Capitalmind Premium Portfolios. This article is intended solely for informational purposes and should not be considered as an investment recommendation.

Capitalmind Research LLP is a SEBI Registered Research Analyst having registration no. INH000014003.

Additional Reads: