Bajaj Finance’s journey began in 1987 as Bajaj Auto Finance Limited, primarily offering loans for Bajaj Auto’s two- and three-wheelers. For nearly a decade, it operated as a captive finance arm serving Bajaj Auto’s customers. Gradually, the company expanded into consumer durable financing, offering small-ticket loans for appliances, and later diversified into business and property loans.

The real turning point came in 2007, just ahead of the global financial crisis, when Rajeev Jain took over as Managing Director. Under his leadership, Bajaj Finance transformed from a slow-paced lender into a high-growth, innovation-led NBFC. In 2010, to reflect its broader vision, the company dropped “Auto” from its name, becoming simply Bajaj Finance Limited.

Below is a breakdown of the current Bajaj Group structure:

*Source: BFL’s Q3 FY25 Investor Presentation.

*Source: BFL’s Q3 FY25 Investor Presentation.

Turing Crisis into Capital: Transformation Post 2008 Turmoil

Around the same time, Citibank India decided to exit its consumer lending business (Citi Financials) due to rising bad loans post the 2008 crisis, creating a noticeable gap in the market.

Recognizing the opportunity, Mr. Pamnani (Ex-Citi bank India CEO & relative of the Bajaj family), Mr. Sanjiv Bajaj, and Mr. Rajeev Jain took decisive steps. They began by cleaning up the legacy loan book, took the initial hit, and shifted focus to consumer and retail lending, including personal loans, consumer durable financing, and mortgages.

From there, Bajaj Finance steadily expanded into a wide range of lending verticals such as SME financing, commercial lending, rural lending, and even brokerage.

A major boost came with the launch of the Zero EMI model, which turned out to be a game-changer, benefiting manufacturers, retailers, and the financier alike, and rapidly accelerating growth in consumer lending.

Presently, BFL stands as one of the most diversified NBFCs, offering 40+ lending products across consumer, SME, commercial, rural, and mortgage segments. It also established subsidiaries like Bajaj Housing Finance (home loans) and Bajaj Financial Securities (broking) to extend its presence in housing finance and investment services.

Below is a segment-wise breakdown of its AUM:

*Source: BFL’s Q3 FY25 Investor Presentation.

*Source: BFL’s Q3 FY25 Investor Presentation.

Mortgage is its biggest contributor, followed by Urban B2C loans and SME lending. Let us have a quick look at its mortgage book too:

*Source: BFL’s Q3 FY25 Investor Presentation.

*Source: BFL’s Q3 FY25 Investor Presentation.

Product Per Customer (PPC) is a useful metric for a diversified business that indicates the average number of products a customer has used over their lifetime with BFL. This figure has steadily increased from 4.99 in FY21 to 6.10 in 9M FY25, highlighting the company’s strong cross-selling capabilities, something we’ll explore in more detail ahead.

*Source: BFL’s Q3 FY25 Investor Presentation.

Now that you have a better sense of BFL’s history and the breadth of its business, let’s try to dissect on factors which as has somewhat kept BFL ahead of the curve over the years.

What’s Set Bajaj Finance Apart Over The Years?

- Innovation:

While it may sound cliché, innovation has truly been a hallmark of Bajaj Finance. The company has consistently carved out new niches in financial services. A standout example is its “No-Cost EMI” model for consumer durables—an offering that not only drove massive adoption but also served as a precursor to the “Buy Now, Pay Later” (BNPL) trend that later became a fintech buzzword. - Prudent Risk Management:

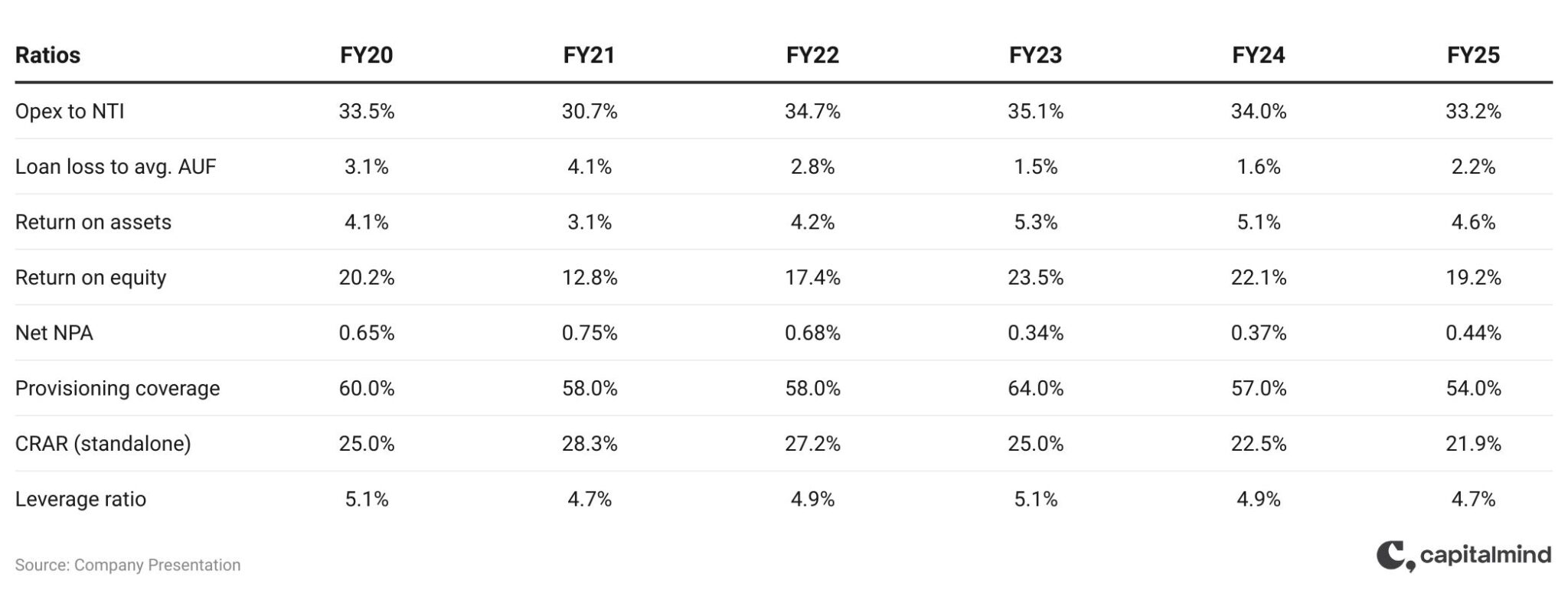

While chasing growth, BFL has built its credibility by never compromising on asset quality. Here are are few metrics to give you insight-

Notable from the table above:

- OPEX to NTI has remained consistently at ~33% from FY20 to FY24, signifying operational leverage.

- Loan Loss to avg. AUF has come down to 3.1% to 2.2%, after peaking at 4.1% in FY21(Covid Hit).

- Profitability metrics like ROA and ROE have remained strong.

- NPAs have remained impressively low.

- Provision Coverage at 54% provides a decent buffer for future stress.

- Capital Adequacy Ratio (CRAR), stands sufficient at ~22%.

On the liabilities side, BFL has maintained a disciplined Asset Liability Management-

*Source: BFL’s Q4 FY25 Investor Presentation.

*Source: BFL’s Q4 FY25 Investor Presentation.

To better understand the chart above: cumulative gap refers to the percentage by which assets exceed liabilities over a specific time period. Bajaj Finance has historically kept this ratio in the 60–110% range for the “up to 1-month” bucket, indicating a comfortable liquidity buffer. Notably, during times of stress like the COVID-19 period, this shot up to 220%, reflecting a deliberately conservative stance. For the 1-year bucket, the company has typically maintained a range of 30–90%, balancing liquidity and asset deployment efficiently.

NBFCs usually deal with higher funding costs because they rely more on borrowings. Over time, Bajaj Finance has managed to ease this challenge by steadily building a strong base of public deposits, which now make up over 20% of its funding mix. This has helped it reduce dependence on short-term market loans. Its borrowings are now more balanced across bank loans (~28%), NCDs (~35%), deposits (~20%), and short-term debt (~12%).

*Source: BFL’s Q4 FY25 Investor Presentation.

*Source: BFL’s Q4 FY25 Investor Presentation.

3. Cross-Selling: BFL operates on a model that inherently supports strong cross-selling, which has been key to deepening its customer relationships. As noted earlier, this capability, backed by a diversified product suite, has driven its average Products Per Customer (PPC) to 6.10 as of December 2025.

Complementing this is BFL’s omnipresent distribution network, spanning over 2.32 lakh touchpoints across India, from large electronics outlets to small kirana stores. This extensive reach has powered rapid customer acquisition, with 18 million new customers added in FY25 alone. Beyond acquiring customers, BFL effectively uses data insights and loyalty programs to cross-sell, helping it build a robust cross-sell franchise of over 64 million.

But What’s Next? Why is Bajaj Finance Looking Interesting Again?

The last 1.5–2 years weren’t kind to lenders. A rapid rate hike cycle—taking repo from 4% to 6.5% between May 2022 and Feb 2023—meant borrowing costs surged, EMIs ballooned, and discretionary credit demand (like personal loans and consumer durables) took a hit.

What Changed?

Inflation has eased to multi-year lows, prompting the RBI to not only pause but begin trimming rates, cutting the repo to 6% by April. This has brought much-needed visibility to funding costs. In fact, a few NBFCs, including Bajaj Finance, have started to see a modest decline in their cost of funds as early as Q3 FY25. Retail deposits (cheaper and more stable) are also growing, offering a stronger foundation for the next lending cycle.

Additionally, the recent budget move to exempt income up to 12 lakh under the new tax regime (effective April) could meaningfully boost disposable incomes, particularly in the middle-income segment. This is expected to revive small-ticket discretionary spending, an area where Bajaj Finance has historically thrived. With its omnipresent distribution and proven playbook in consumer financing, BFL appears well-positioned to ride this potential consumption upswing.

That being said, let’s quickly run through its financials:

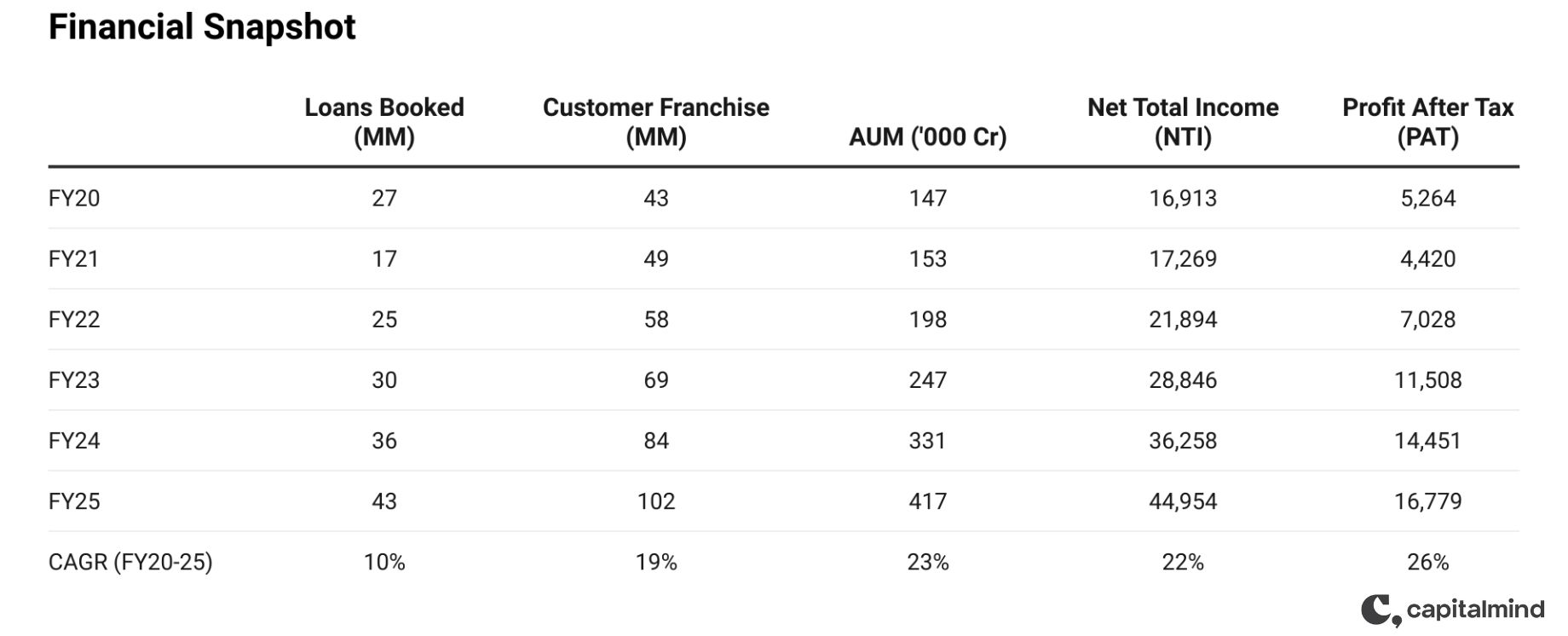

Over the past five years, BFL’s loan book has grown at a 10% CAGR, expanding from 27 Mn to 43 Mn loans, while its customer franchise has more than doubled from 43 Mn to 102 Mn.

Over the past five years, BFL’s loan book has grown at a 10% CAGR, expanding from 27 Mn to 43 Mn loans, while its customer franchise has more than doubled from 43 Mn to 102 Mn.

Its AUM have also seen strong growth, rising at a 23% CAGR to reach 4.17 lakh crore by the end of FY25. Net Total Income has kept pace with AUM growth, while PAT has clocked a 26% CAGR over the same period.

The management is targeting a customer franchise of 190–210 million by FY29, while aiming to scale its cross-sell franchise to 115–225 million over the same period.

Bajaj Finance follows a 14-year-old strategic process called the Long Range Strategy (LRS), a five-year rolling plan with 12–24 month execution roadmaps. Through this, the company identifies emerging megatrends to drive its future growth.

As part of its LRS 2025–29, BFL plans to work on 28 megatrends in total, with three newly identified: Green Finance, Multi-Cloud, and Zero Trust.

Under Green Finance, BFL plans to start financing solar and EV products such as solar panels and electric vehicles for retail and MSME customers beginning in Q4 FY25, with a goal of building a 2,000 crore green finance portfolio by FY26.

The Zero Trust initiative will focus on the principle of “trust but always verify”, with the company strengthening its cybersecurity framework to better protect customer data and transactions.

Meanwhile, the Multi-Cloud strategy aims to enable its applications to run seamlessly across multiple cloud platforms. In the first phase, Bajaj Finance plans to migrate the top 40 out of 94 critical applications over the next 18 months.

What We Think, The Future Holds?

With that, BFL appears well-positioned to capture further growth if the lending environment continues to improve, as discussed earlier. While the company has always been recognized as a high-quality franchise, the broader lending sector has faced its share of challenges over the past couple of years.

Now, with better visibility on interest rates, lower inflation, and reviving consumption trends, the backdrop seems more favorable. In terms of valuation, BFL is currently trading at a TTM P/E of around 33x, which is fairly in line with industry averages, neither overly expensive nor particularly cheap, but reasonable considering its historical track record and growth profile.

Going forward, it will be important to watch how the company executes on its newer initiatives, while also strengthening its core businesses.

Disclosure: I, Sidhanth Paul, Research Analyst, author, and the name subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific view(s) in this report.

Research Analyst or his/her relative or Capitalmind Research LLP does not have any financial interest in the subject company. Also, the Research Analyst, his relative, Capitalmind Research LLP, or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further, Research Analyst or his relative or Capitalmind Research LLP or its associate does not have any material conflict of interest at the time of publication of this research report.

Also, Bajaj Finance is a part of our Capitalmind Premium Portfolios. This article is intended solely for informational purposes and should not be considered as an investment recommendation.

Capitalmind Research LLP is a SEBI Registered Research Analyst, having registration no. INH000014003.

Additional Reads: