Things are looking strangely bad for the economy. Bad because, well, I’ll put up some data. And strangely because this isn’t really upon us overnight – but we were rejoicing just a few quarters ago.

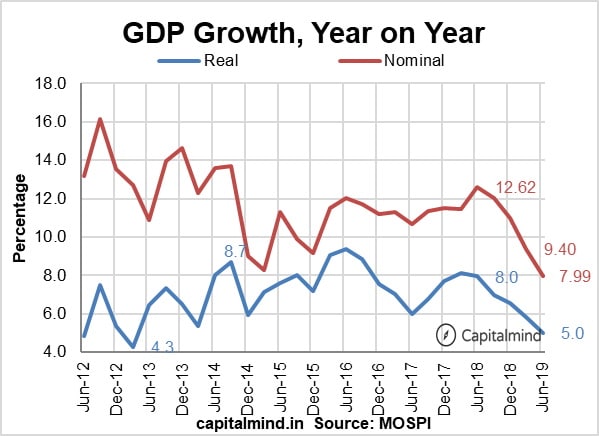

What’s really wrong? At the very top, the GDP is now SLOW as heck.

The Real GDP which subtracts inflation is now down to 5% growth. But the issue is also in the part that included inflation (the “Nominal” GDP). Even that is only growing at 8%!

To give you a context, India’s not seen nominal GDP at such a low number since June 2009, which was just after the global financial crisis! In fact, there have only been four instances in the last twenty years when nominal quarterly GDP grew below 8% – In 2001, 2003 and then twice in 2009. In all three occasions, the economy was in a mess.

But this time, it comes on the back of sustained low inflation. That’s a good thing. But low growth is a bad thing. They are related – you can push up growth through high inflation, which then hits you hard when inflation is brought down, because growth comes down. If you want real growth, then it has to come even when inflation is low.

(Note: the only other time when real growth was below 5% was in 2013 in the chart above. But guess what, even then, nominal growth was 12.5% – meaning, we had low growth and high inflation. That’s a much worse situation)

Oh yes, there are parallels

In the US there was high inflation in the late 70s, and Paul Volcker took interest rates up to 16% (!) to control it. This resulted in two back-to-back recessions, when the GDP growth number was a mathematical negative! We haven’t reached that stage (yet) but it’s evident that a high interest rate cycle that is used to control inflation has an impact – that it slows the economy.

But was it really bad? After Volcker was the era of Alan Greenspan, who lived through some of the best years economically, for the US. The 17 years after the 1982 recession were relatively benign times for the US, which was easily able to cut interest rates and grow. You could say that Volcker’s recessions through high rates removed so much of the excesses that the US was able to regenerate and grow rapidly through the 80s and 90s. Essentially, that his work formed the base for a solid economy going forward.

If you look at it that way, India’s right there. High inflation in the past, check. Slowing inflation, check. High interest rates (till earlier this year), check. The high interest rates creating slow growth, check.

(Hear: Our podcast on the stubbornly high cost of capital, or interest rates, in India)

So if we’re slowing because this is the impact of controlling inflation, it’s not that bad – but the fear is that it’s a lot worse. Whatever it is, it’s a slowdown, a cut down of sorts. It could be the delayed impact of demonetization. It could be that the compliance costs of GST hurt. It could also be the impact of the hurting of the informal economy. At one point just after demonetization, I wondered if the economy would see a recession. (Read post)

We’ll see lower inflation, though at this point, inflation is driven by supply also, and lower supply might be a concern. Trucks aren’t able to carry things over, and if supplies fall short, inflation will spike. Over time, though, we will see a marked drop in prices if there is a contraction.

A contraction or recession are just terms – in reality, we won’t see GDP figures actually go down, since the data collection process won’t show too many chinks in the armour. But the hit to the economy will be visible even if growth slows from 7% to 3%.

There is long term gain in any recession when things are getting cleaned up.

Is there a benefit to a (gasp) slowdown?

Indians have a God of destruction. This is a fascinating concept. Not a demon or an asura. An actual God. We have the traditional view that the act of destruction, however tragic, can be good.

Cancer treatment involves killing of bad cells by chemotherapy. But the chemo kills good cells too – they are just collateral damage. The idea of killing a part of you to save the rest of you – is that good or bad?

In financial terms, we have bankruptcy laws. In India we think this is a way for banks to recover money. It’s not. It’s a way for banks to finally decide how much they will lose. It’s the destruction of their capital that ensures that a company can be revived or given to someone who can run it better without the burden of all that debt. It’s the act of destruction of something (bank capital) that revives something else (the company).

India’s greatest reforms came in 1991-92. When we were so badly screwed that we had to reform, or else. We opened up the economy. It wasn’t like a secret that the economy needed opening. Everyone knew it. But no one would do it because oh my goodness, if you did do it, what’s the impact? Allowing foreign companies to come in? They’ll steal everything! Letting Indian companies produce as much as they want? The sacrilege! Etc.

But it happened because there was a recession then. And we had our backs to the wall. And the naysayers were too busy telling us that the world is coming to an end, rather than calling it sacrilege to produce more than some license allowed. So the reforms happened.

They didn’t waste that slowdown.

Don’t Waste This Slowdown Either

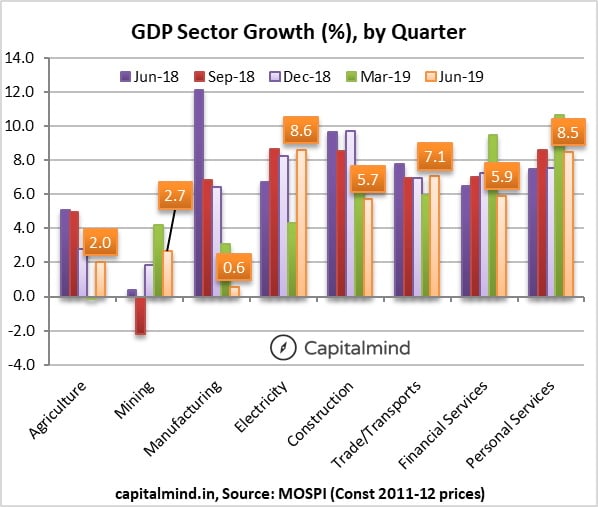

A slowdown is happening. And where? Here’s a look at GDP in another way – sectors:

You see the problem? It’s not in personal services. This is your household services, or consultants, or doctors or food or such things. That’s growing at 8% Real.

Not in trade or transportation yet. That’s 7.1%. Electricity grows at 8.6% because hey, more people etc. Some in construction (5.9%) and some in financial services (5.9%). Thats because of the slowdown in the investment process – no one wants real estate quite as much. And much of the financing around it has shut down too. Maybe we can fix that. That’s one part to look at – real estate and construction.

There’s agriculture at 2%. We need to change that – because it’s not like we are reducing yields. We are producing more of the things India doesn’t really need more of (rice and wheat and vegetables) and not enough of things we might need (meat, fish, eggs, milk). There needs to be a way to energize this sector – or at least, move out people from here to a different and more productive profession.

Mining is rough, but it goes hand in hand with industry.

The big one is manufacturing. It’s slowed to 0.6%. And that really sucks. And we need to change that. How? That part comes in later.

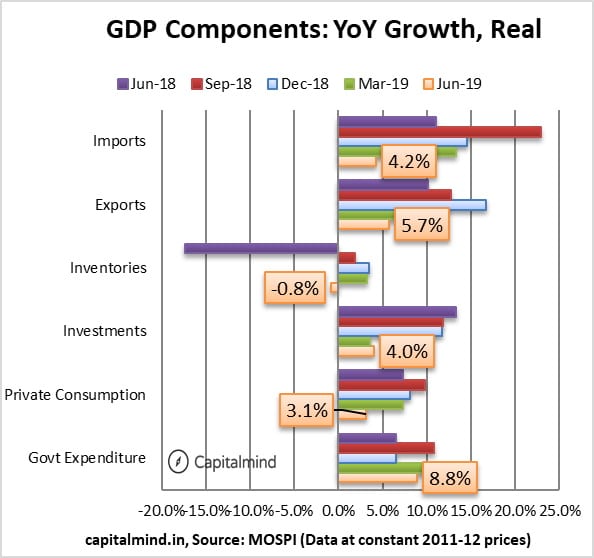

A look at various ways the GDP is captured.

Government expenditure did the deal, but it’s not meaningfully higher than in previous quarters.

The big deal is private consumption. This is like 55% of the economy, and consumption has gone for a toss. We need to fix this, but not at the expense of other things. However, encouraging consumption doesn’t have to mean doing stupid things. The likes of Swiggy and Oyo and Uber have fearlessly paid us for many years to take cheap car rides or get discounted food or hotels. But when they’ve eliminated most competition, they find that the population simply will not pay more when they remove the discounting or attempt to charge hotel owners. You don’t want to encourage consumption by discounting it. (Let the startups keep doing that. A few more years, please.) You want to foster competition and allow for more technology that can come in and allow for even cheaper transport or food or such – consumption will pick up. More on this later.

We need more investments. This is growing too slowly, and decelerating. With a big chunk of Indian savings and investments going to gold and real estate, looking at savings rates is a bad idea. We need more productive investments – in real businesses, in technology and in items of some scale.

Exports minus Imports is what enhances the GDP. You know something? In the March quarter, if you removed just one item from the imports (Gold) you will find that we actually have more exports than imports. No, really.

We did see many horrendous quarters, but the March one was a reversal, and in good part, we were negative because of one thing: Gold. (We also raised import duties and clamped down on Chinese imports this year, which probably helped).

Gold was $8 billion in the March quarter. If you removed Gold entirely, we would have been $3.5 billion positive!

We can’t just ban gold imports. Then we’ll deal with something that combines ISIS+Al-Qaeda+Mexican-Cartel together in terms of smuggling and money power.

But we can do certain things that, in good times, would be considered not that great. Like we should allow Gold exports (did you even know they were banned? Even in part of the British era?)

But we can do it now because it’s a slowdown and things must be done.

Let’s not waste it this time.

Over the next few posts, I will elaborate on my thoughts about this topic.

- Reducing gold imports (Read post)

- Encouraging investments and thus manufacturing/startups

- Deregulation (especially from the RBI)

- Other changes like freeing the rupee, changing certain stupid laws and so on.

Regardless, what we should do is to understand that tough times need good measures. The opposition to things like a free rupee, or to allowing gold exports are usually the kind that says “we can’t trust the government” or “we can’t trust people to not wet their own pants all the time”. This works for great discussion when everyone’s stomach is full and people are gainfully employed. So it won’t be allowed.

In a slowdown, sabki phat thi hai. We’ll have no choice but to trust and make these decisions, and learn to fail a little and falter a little but at least keep moving ahead. You can speculate, till kingdom come, about how deep a river is. But if there’s a wild animal chasing you, you’re going to find a way to cross – the alternative is unacceptable.

Hey, we could keep slowing down and complaining. Or we could use this time to make a change. Our choice.

Chime in, please. @deepakshenoy on twitter.