Ceramics stocks have been shining recently, and have shown improved margins. It was the same case with Cera and today again Asian Granito and Somany have confirmed the margin improvements. Even for that matter Kajaria Ceramics has improved its margins slightly, but on the revenue and profit growth front, Kajaria has put a dismal show.

Somany Ceramics

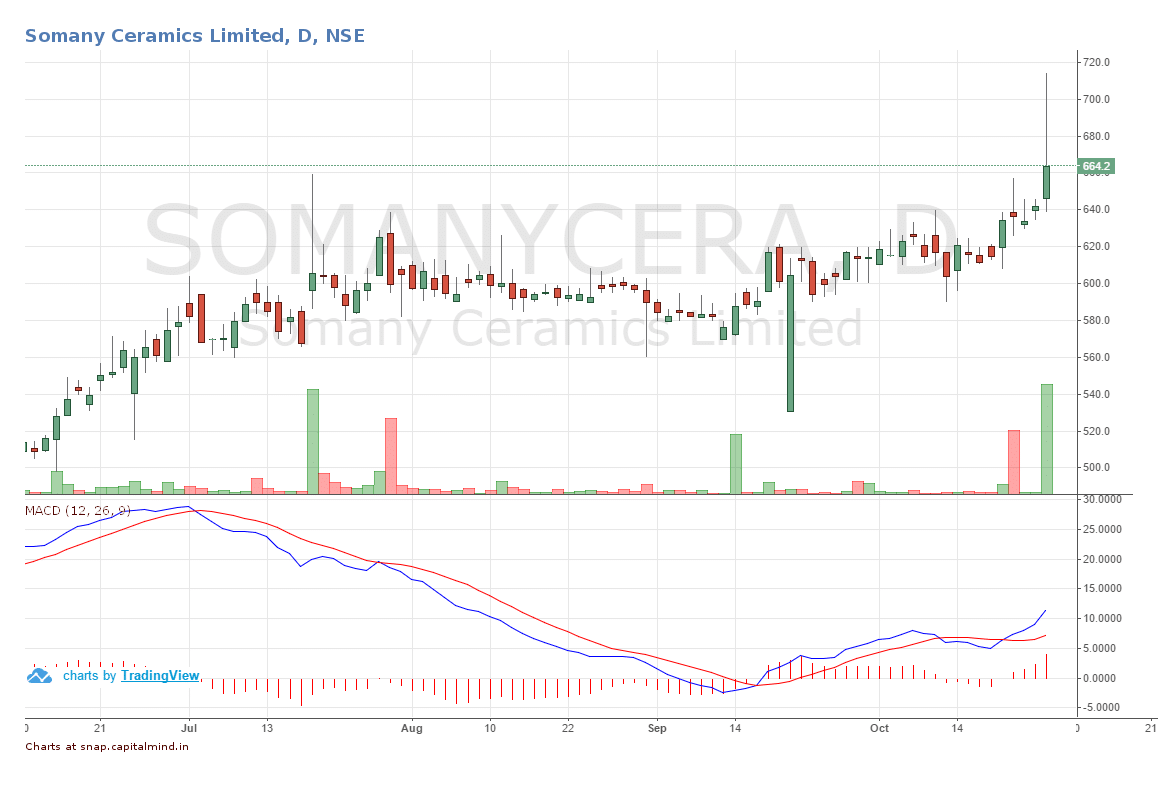

![]() Somany ceramics which is into tiles, sanitary ware and fittings has given blockbuster results for the quarter. Somany has posted 116% growth in profits YoY, with just 11% growth in revenue.

Somany ceramics which is into tiles, sanitary ware and fittings has given blockbuster results for the quarter. Somany has posted 116% growth in profits YoY, with just 11% growth in revenue.

Key Takeaways:

- Operating Margin improved from 5.48% in Q2FY16 to 7.51% for the current reported period.

- Power and Fuel expenses have fallen: they accounted 7.81% of the revenue for this quarter, but for same quarter last year it was about 9.35%.

- Somany Ceramics still has 101.50 Cr unused cash with it from previous QIP, which doubled the “other income”. The QIP raised 120 Cr for the company in December 2015.

- They intend to buy 51% investment in Sudha Ceramics for setting up vitrified tiles manufacturing plant in Andhra Pradesh.

Asian Granito India

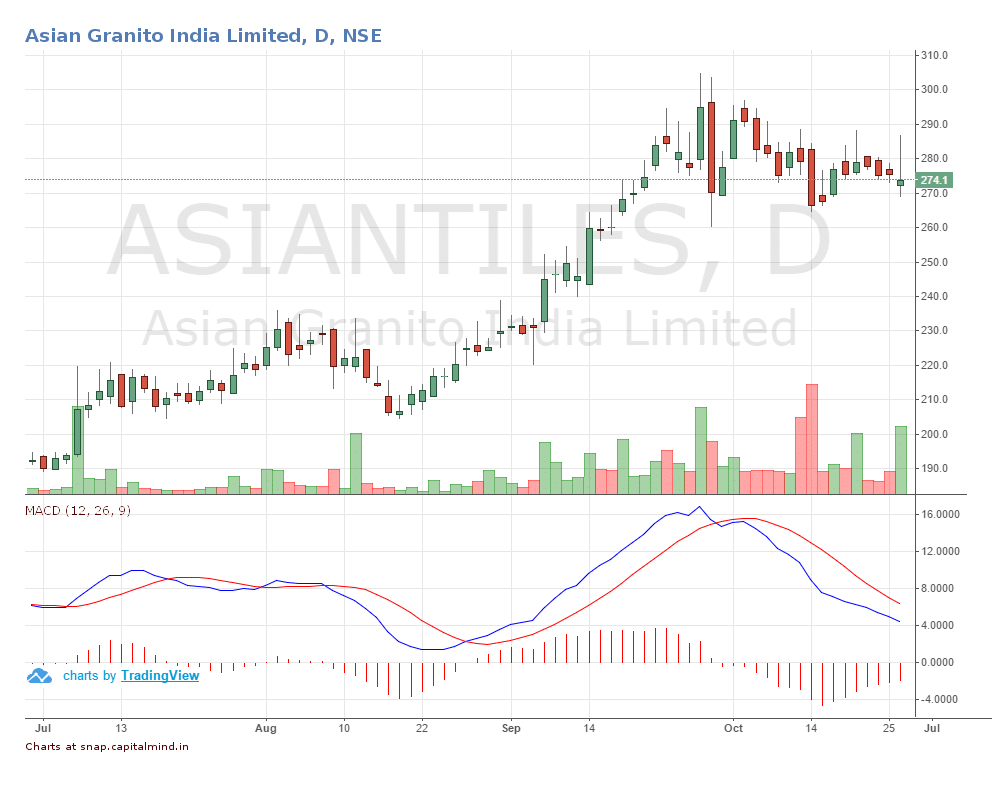

![]() This Ahmedabad based granite company generated 56% growth in profits, with a revenue growth of just 6% YoY. Improved operating margins due to lower power and fuel costs and revenue generation from its newly acquired companies have made this profit possible.

This Ahmedabad based granite company generated 56% growth in profits, with a revenue growth of just 6% YoY. Improved operating margins due to lower power and fuel costs and revenue generation from its newly acquired companies have made this profit possible.

Key Takeaways:

- Operating Margin improved from 6.4% in Q2 last year to 8.36% for the current quarter.

- Power and Fuel cost fell: they were 13.9% of the revenue in Q2 last year, for Q2 current year power and fuel cost accounted for 11.26% of the revenue.

- Finance cost has increased by 35.44%, indicating higher debt on the books after the mergers.

- EPS growth was only 17.22% compared to 56.17% growth in profits, mainly due to 75 lakh more shares added due to dilution due to the acquisitions.

- Board has declared interim dividend of Rs 0.50/ share.

Kajaria Ceramics

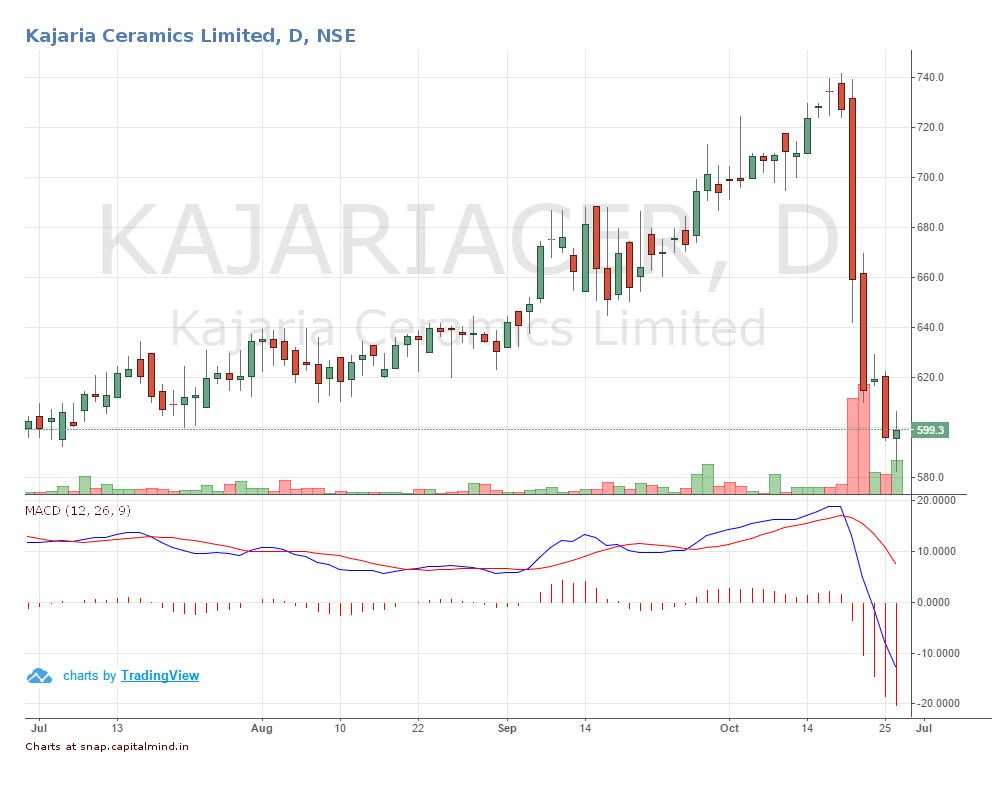

![]() India’s biggest player in terms of ceramics has put up poor growth numbers for the current quarter. The revenue grew by 4.04% YoY, with profit increase of meager 7.68%.

India’s biggest player in terms of ceramics has put up poor growth numbers for the current quarter. The revenue grew by 4.04% YoY, with profit increase of meager 7.68%.

Key Takeaways:

- Operating Margin increased slightly from 14.83% Q2 last year to 15.04% for Q2 current year.

- Power and fuel cost which accounted for 15.54% of the revenue for current quarter, was at 18.45% for same quarter last year.

- Finance costs have come down from 9.6 Crs in Q2 Last year to 7.88 crs for current reported period – a decline of 18% indicating a decline in overall debt of the firm.

- For the current quarter, the firm paid 38.25% of the PBT as taxes, for same quarter last year it was about 34.33%.

- The stock crashed after results from nearly 740 to below Rs. 600. The results were, perhaps, not quite in line with other ceramics companies where a 10% topline growth resulted in substantially higher profit growth due to lower expenses.

Disclosure: Author does not own any shares in any of the companies above.