Options traders will know how critical the 30th of October is.

It’s the date when F&O contracts are massively changing in size, from the current Rs. 2 lakh to Rs. 5 lakh each. Already, November contracts are trading at Rs. 5 lakh contract values, which means the lot size of a Nifty contract is 75 if you bought the November future versus only 25 if you bought the October future.

We know that things will change on Oct 30, because then, the October contract would have expired. (It expires on Oct 29) What happens then?

[level-capmind-pro]

The biggest fear is in stock options. They are already illiquid, and if the lot size increases, they will become even more illiquid, one thinks. But that’s not quite so.

Most Derivatives Go Up 2x to 3x

There are 167 stock and index instruments that have derivatives, not counting those on foreign exchanges or on the VIX. Of these:

• 95 will see an increase of 2x to 3x in terms of lot sizes.

• 54 stocks see a change of 1.2x to 2x

• The Full List is here.

Certain stocks will see no change in the lot size or the lots will become smaller.

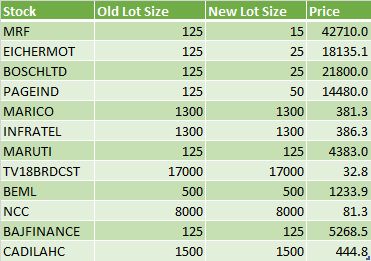

In these stocks we should see activity increase. MRF didn’t see that much option trading, nor did Eicher Motors or Bosch. We should see that change now. Stocks like Maruti which have been active in the options scene will stay active. Or get more so as traffic moves away from the other zones.

But some stocks see a big increase:

Action in these stocks will probably be only in the futures – options are likely to be shunned for now. Unitech’s lot size is a joke. But Unitech’s price is also a joke. It’s strange it’s even allowed into the F&O market.

In general, options volumes are heaviest on the Nifty. The rest – stocks and other indexes – aren’t very large in comparison.

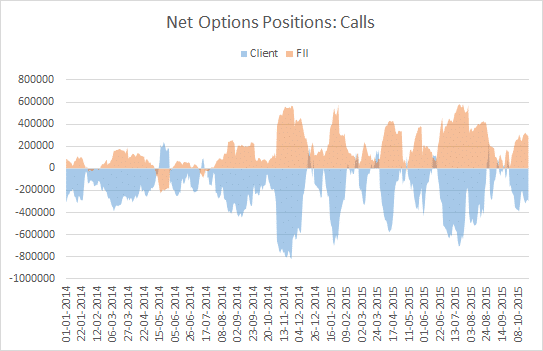

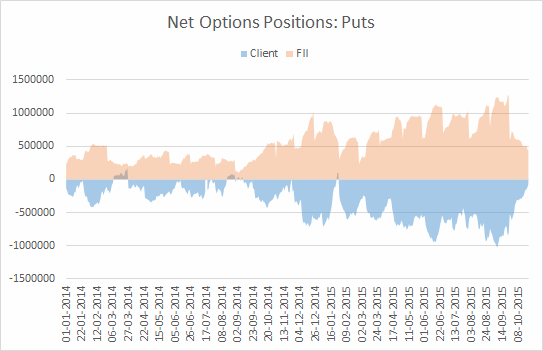

Retail: The Biggest “Short” Index Options Trader

Looking at the data, HNI and Retail clients (called “Client”) have the highest short options positions in the market. If you look at both calls and puts on the Index, FIIs are generally on the long side (net position), while Clients are on the short side. (The other players are Domestic Institutions or DIIs, who are not allowed to be short in options, and PRO, meaning proprietary trading accounts of brokers).

In general, index puts – mostly the Nifty – will have increased in lot size from 25 to 75. But since the Nifty requires a very low margin, a short position in options currently needs only Rs. 20,000 or so in margin. This will change to Rs. 60,000 per lot, which is not a dramatically high number.

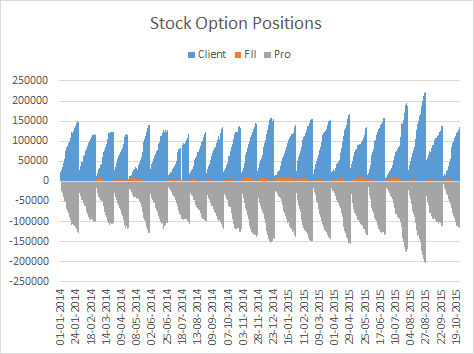

The Impact Will Be In Stock Options, Where Clients Are Long

But the picture is completely different in stock options positions. Here, retail clients are long in general, not short.

And the counterside is taken by brokers, as the PRO positions. FIIs are non players in this segment!

You would have never guessed this until the data revealed it – the largest player in stock options are retail clients, on the long side.

Brokers go short, but much of this is through algorithmic trading. (anecdotal, but you can see it on the terminals)

In general, costs of option contracts will go up 2x to 3x, come October 30. This will change liquidity patterns – people would buy just one contract will find it too expensive given the larger lot size. If these players leave, demand will fall, and even though the supply side is well populated (largely through algos on the broker end).

This will probably lead to over priced options at some level, but the presence of algos on the other side (the sell side) means that liquidity may not be that hard to come by. Market Making algos generally use the underlying (or future) to decide where to buy or sell an option, and if there is liquidity in the future they will still be placing bids and asks.

Still, it remains the most important side to the argument on the changing lot sizes: Will Stock Option Liquidity Fall?

Our View: Index Action Will Continue, But Stock Options Could See A Big Change

Index options are largely shorted by retail traders but as we have seen, the margin increase is not out of bounds. Someone who’s only got Rs. 20,000 will not be shorting index options, they will be going long stock options. Someone who’s short an index option might actually have 2 lakh or more of capital. For such a person, the increase in lot size from 25 to 75 (of Nifty) and 25 to 30 (of Bank Nifty) is only semantic. We therefore see very little impact of the lot size change here.

But stock options see mostly algo-shorts from brokers. FIIs are non players here. Retail clients are mostly long here. This segment will see the bulk of the change, and liquidity could fall as there are less buyers available. However, the large presence of algos (who don’t care how much they have to wait to get a trade) will mean that liquidity may still be available to an option buyer, just that the price changes may not be reflective entirely of demand.

Where will they go? If they can’t trade options, the retail small speculator will find solace in small and mid-caps. Or, they will move entirely to those options where the lot size change is not significant. Both have solid trade implications, and this analysis will be repeated as the next expiry progresses.

![]()

Disclaimer

Nothing in this newsletter is financial advice and should not be construed as such. Please do not take trading decisions based solely on the matter above; if you do, it is entirely at your own risk without any liability to Capital Mind. This is educational or informational matter only, and is provided as an opinion.

Disclosure: The authors at Capital Mind have positions in the market and some of them may support or contradict the material given above, or may involve a direction derived from independent analysis.

[/level-capmind-pro]