Why are we so trusting of rating agencies? The recent drama with Amtek Auto and the restriction on redemptions to 1% by JP Morgan AMC on two of its funds is a glaring example of where rating agencies have failed to identify problems early.

In two more examples, it’s apparent that rating agencies have rated debt very high when they shouldn’t at all be given that kind of rating, at least in my opinion

Take the case of Sprit Textiles Private Limited. This is a promoter company of Zee and Dish TV, and is owned by Subhash Chandra and the promoter group. Let me quote the rating agency, Brickwork, on specific aspects of their rating.

STPL is a part of Essel Group belonging to Mr Subhash Chandra and family. The company primarily acts as a holding company for the group. The Company has two directors on board -Mr. Sanjeev Chaudhary and Mr. Amol Deshmukh who are nominees of the promoters. The Company intends to use the proceeds of the NCD towards General Corporate Purposes as well as for the repayment of the existing debt. For FY13, STPL reported revenue of Rs. 83.5o Cr, loss of Rs. 473.56 Cr, Total Debt of Rs. 2279.23 Cr (Secured & Unsecured) and negative networth of Rs. 0.30 Cr.

Get this. The company has NO OPERATIONAL CASH FLOWS. Means, it really does nothing. And still, it has more than Rs. 2,200 cr. of debt. And a negative net worth!

How does it service that debt? By pledging shares, apparently.

The given rating essentially captures performance of ZEEL and DTIL, since STPL does not have operational cash flows and the NCD structure involves pledge of ZEEL & DTIL equity shares provided as security. Security cover of 1.75 times provides cushion to investors.

So exactly how many shares of ZEE and DTIL does Sprit Textiles own? Answer: 300 shares of each. Together, they are worth less than two lakh rupees. See the latest shareholding pattern:

Obviously some of the other promoters of Zee and DTIL has pledged their shares to cover the loan because Rs. 1 lakh worth of shares cannot be used for crores and crores of debt.

So how is the rating agency providing a rating of “A+” On it? (suffixed with SO, meaning structured obligation). Thisis like the third highest rating that signifies “adequate degree of safety regarding timely servicing of financial obligations”. But how? The company itself owns very few shares, it has nearly no operational cash flows, and is loss making and has negative net worth. The rating is ENTIRELY based on the valuation of Zee and DTIL shares. What if they crash like Amtek Auto tomorrow?

There is no corporate guarantee by the Zee and Dish TV companies themselves, only a promise of further shares to be placed on pledges. But if these shares tank, that is a massive amount of debt that depends on those very share prices!

And there’s another one: Essel Corporate Resources

Again, Brickwork rates them A+ (SO).

ECRPL is a promoter company of Essel Group belonging to Mr. Subhash Chandra and family. The Company has two directors on board — Mr. Sunil Singhal and Mr. Ashok Sanghvi, who are nominees of the promoters. The Company mainly acts as a holding company investing in the group entities. The revenue sources for the company are rental income from owned building and dividend income from investments. For FY13, ECRPL reported revenue of Rs. 32.89 Cr, loss of Rs. 106.12 Cr, Total Debt of Rs. 1355.22 Cr (Secured & Unsecured) and negative networth of Rs. 1096.65 cr. The Debt is majorly in the form of NCD’s, unsecured loans from financial institutions and NBFCs and ICDs from group companies. The source of repayment would be refinancing/ promoter funding.

And Who’s Lending To Them?

Have you heard of Franklin Templeton Mutual Fund?

FT Mutual Fund has bought a very large amount of the debt given by Sprit Textiles. In its latest portfolio it shows over Rs. 800 cr. of bonds bought from Sprit Textiles and Rs. 580 cr. from Essel Corporate Resources Pvt Ltd.

Most holdings are relatively small percentages (3% or so ) of the total portfolios but it still calls to question why these bonds should figure at such a high level of interest.

Now there’s probably a good reason for Franklin Templeton (FT) to buy these bonds, but in then, in funds like Short Term and Ultra Short term funds? If the prices of Zee/Dish TV crash, then these funds have no other assets to claim and recover the money.

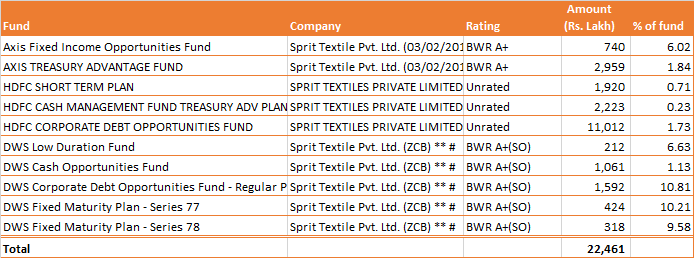

And they’re three other fund houses that have invested in Sprit Textiles’ debt: Deutsche, Axis and HDFC. HDFC has larger amounts but for some of the others, this investment is a large percentage of the fund:

What To Do?

This was just an example. Just one company – apparently and implictly backed by the Zee promoters – has garnered over 1000 cr. of debt from mutual funds, with nearly no operations, and with only shares as collateral.

It is your right to demand an explanation of a fund manager – they do not have access to any liquidity and if a fund that is “short term” in nature ever sees investors exiting, you will find redemption gates becoming common; because let’s face it, these above companies and bonds are very illiquid.

There is no indication of any default of any sort by Sprit or Essel or whoever. But as a bond holder, you don’t care about a default – you should only care about whether Zee and Dish TV stock prices are falling – if they fall too much, then this is going to be a dud investment.

If I had the above funds in my portfolio my choice would be to diversify away from them. At this point it makes very little sense to buy a debt instrument that effectively gives me a fixed upside but the downside of a stock.

What’s important though is:

- Check the portfolio of the funds you own, even those that say they are short term or liquid

- See if there are companies you don’t recognize or like in there (anything that is government or sovereign is okay, bank CDs are okay for now and large listed companies like Shriram Transport finance etc. are fine)

- Specifically are there private limited companies there?

- If so, check the rating document online. If the rating document has flimsy rationale like depending on stocks pledged, then you want to reconsider that fund in the first place.

- Don’t trust ratings. Credit rating agencies are the worst people to rely on in a crisis, and you should do your own diligence, and demand answers of your fund managers.

Note: There is no credit issue with the above mentioned Zee promoter companies that I know of. So don’t go around thinking there’s a default at all.

But given that all the money they have borrowed is based on sound collateral and there is no real business to speak of, this kind of debt should be rated in the low B’s for risk and should definitely not be held in treasury or ultra-short-term portfolios.