After Budget 2014, there has been talk of using arbitrage funds instead to get a reasonable post-tax return. How do these funds work? What kinds of arbitrage can you do, with different levels of risk, in the markets? In a series in Optionalysis, we will address this situation.

The Cash Future Arb

[level-capmind-pro]

If you buy stock in the cash markets, and sell the future, you will be able to “lock in” the difference between the two. Your cost is the cost of the stock (cash). Futures require margin, but you can provide the stock to your broker for margin. (Some brokers only allow 80% to 90% in stock, so you will need some cash too).

Let’s say the stock moves up 10%. The cash stock goes up and the short-sale on the future loses – by about the same amount.

Note: When you lose money on the future, you have to pay the “mark-to-market” cost to your broker. This adds to the total amount of money you deploy on this strategy.

Eventually, by the expiry date, the future will converge on the stock price. At this time, you would sell the stock and buy the future and thus realize the arbitrage.

Rollover: If, on expiry day, there is a good arbitrage between the subsequent month’s future and the cash price, then you can simply roll-over; meaning, you buy back the current month’s future and sell the next month’s future. This will save you the transaction costs you incur on the cash part of the deal.

How much can you make?

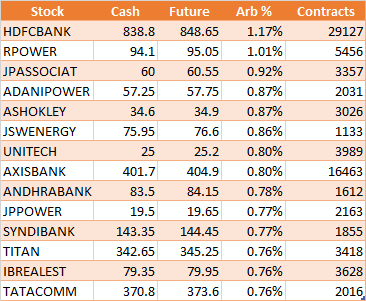

While we could start anytime, here’s the list of arb opportunities available as of the 30th of July, for expiry on the 28th of August. (Remember, expiry is typically on the last Thursday of the month).

So at the upper end you could lock in 1.17% for the month on HDFC Bank, buying cash and selling the future. For a lot size of 500 shares, that’s an outlay of around Rs. 420,000 for a return of Rs. 4500 by August end.

There is convergence of the two prices, on expiry day. The future expires at the cash price on the day of expiry.

This is easily said in theory. In practice, though, there are many risks involved.

Operational Issues

Can you actually lock in the difference? You have to buy the stock and sell in future at the same time. You can’t do a single order that does both. This means that between the two legs there is a time gap, and in that time, the stock can move fast, making the situation difficult for you.

Secondly, what we look at is the end-of-day price; this is the weighted average price of the last 30 minutes of the day. This may not apply at all when you look at prices in the market.

Finally, liquidity is a key issue in India. What sounds juicy can be unavailable because there is no one on the other side. For example, in the list above, we had to remove MRF because there were just 152 contracts traded the whole day!

The costs

• STT on Stock: 0.25% of the stock’s value (buy and sell stock). You can reduce this if you “roll over” the arb for the next time.

• STT on Future: 0.01% of the future value.

• Mark-to-market on the Future. If the stock goes up, the short position loses money, and the future will require payment of mark to market margin (in cash, not in stock). This can reduce your return since the money you will need will be higher, with the cash stock purchase and the mark-to-market payout.

• Brokerage. Most discount brokers ask you to pay Rs. 20 each way, which will add up to Rs. 80 on a four legged traded (2 legs on entry, 2 legs on exit).

• Slippage: Assume that you will lose about 0.1% to 0.2% on each trade. However, if you were to automate the trade (many brokers now allow this) you can reduce this cost too.

Mark-To-Market Override: Write In the Money Calls Instead of Futures

Paying a MTM every day (when the stock goes up) is a pain. What if you write deep in the money call options instead? Options have no MTM payouts; they only require a margin to be placed with the broker – that margin can again be in stock. Of course since part of the margin is in cash, you still will need more cash, but it will be for a fraction of the increase rather than a payout for all of the increase.

This increases efficiency of your capital.

Deep in the money calls give you protection on the down side only as much as the premium you receive. Which means if you write a 760 call on HDFC Bank at Rs. 88, that’s as effective as selling a future at 848. But it only protects you until the stock goes to 760, below that you have no protection!

(One way to handle that is to buy back the 760 call and write something further below)

But this adds a small layer or risk. Remember, arbitrage with a "little" bit of risk is like picking pennies in front of a road-roller – if the road roller moves, it can wipe out more than a few months of profit! Or, if you prefer, this is what they call a "tail risk" – a massive move that isn’t expected to happen, but does more frequently than statistics imply.

Cost Optimization: Writing In The Money Puts Instead of Cash

On the other end, if write deep in the money put options, it’s equivalent to buying a stock.

If you write a HDFC Bank 930 put option (August) at Rs. 100 and sell the future at Rs. 847, you can “lock in” Rs. 17 as a partial arbitrage.

The option gives you a complete risk protection on the downside. That is, even if HDFC Bank fell to Rs. 700, you would still make Rs. 17. (You make Rs. 147 on the future, Rs. 100 as premium, and pay Rs. 230 as option premium on expiry)

The risk is on the upside – if HDFC Bank went to Rs. 930, the arb protects you no further. So for that much risk, you get a semi-arbitrage. Again, you can offset this by buying back the 930 put and selling, at that time, a 1000 put or such. (But you do understand that the nature of the return will change, and you might end up with a sub-par number)

Inverse Cash Future Arb

Some stocks trade at a premium to the future price. This could be because of dividend, where the future will account for the dividend immediately, but the cash price remains elevated until the “ex-date”.

But it could also be due to a structural imbalance. On 30 July 2014, IFCI trades at Rs. 37.7, but the August future trades at Rs. 37, which means a near 2% arbitrage.

This can only be bridged if you can sell the stock and buy the future. But you can’t sell the stock if you don’t own it! One way to do so is to “borrow” the stock through the SLB system, which many brokers do not allow their retail customers to participate in. But hopefully this avenue will improve; like we said in our earlier post, you can earn money from stocks you own by lending them out too, for such opportunities.

Better Left to Funds?

While mutual funds can do standard cash-fut arbitrage, they can’t write options, so they can’t do the last two “optimizations” that are available.

But remember that if you do this arb yourself, you might end up with different taxation structures – while holding an “arb fund” for a year gives you no taxes (since it’s an equity fund), doing the arb yourself will mean you will pay short term capital gains tax, which can lower your net effective return by 10%.

However, for larger funds, it pays to automate such transactions and get in an out as neces

sary.

You can see a list of arb funds from Value Research Online. We would choose a fund through a direct plan (gives you 0.50% more per year) and one which has a reasonable portfolio size (300 cr.+)

More Arb Gyan

We will have more on this topic. Here’s the topic list:

• Inter-exchange arbitrage

• Stocks-Index Arb

• Put-Call Parity

• Higher Risk Arb: Mergers and Delisting

• Non-convergence: ADRs and Indian Stock

• Stat-arb: Pair Trading

Do let us know what you think. We aren’t recommending trades, and this is not portfolio advice. Please do understand the risks before you trade.

![]()

Disclaimer

Nothing in this newsletter is financial advice and should not be construed as such. Please do not take trading decisions based solely on the matter above; if you do, it is entirely at your own risk without any liability to Capital Mind. This is educational or informational matter only, and is provided as an opinion.

Disclosure: The authors at Capital Mind have positions in the market and some of them may support or contradict the material given above, or may involve a direction derived from independent analysis.

[/level-capmind-pro]