This is an archive for Capital Mind Premium subscribers.

Options are a strange beast. Most options expire worthless, and this has been demonstrated in the US (read: Do Options Sellers Have a Trading Edge?) If this is true, then let’s make a big assumption. Assume there is a Mr. Market, who is a big force and can move the market. He is an option seller.

As we come closer to expiry Mr. Market moves an index or stock so that sellers get hurt the least possible.

For the option Buyer, this is therefore the most painful. The idea of hurting as few option sales as possible is like saying lets see where the option buyer is hurt the most.

Remember, option buying and selling are assymetric. Option buyers have limited risk and unlimited profit. Option sellers have unlimited downside but a limited upside. Since most of the “dumb” money wants limited risk for unlimited profit, it can be stated that much of the sales side consists of “smart” money. Smart in this context means they usually have more money – and it might be that they can, with their money, manipulate the market to move in the direction of their highest profit (or least loss).

How to Think of Max Pain

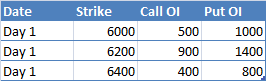

Assume you had just three strike prices. At each strike price, you have set of trades for calls and puts. There is an “open interest” (OI), i.e. the number of open positions of calls and puts that each have a buyer and seller. Let’s sum up the OI for calls and puts, per stock price, on every day before the expiry date. Let’s take two days before expiry in an example.

On the first day, let’s say the Nifty is at 6198. Here’s the positions of all the strike prices.

Where’s the pain?

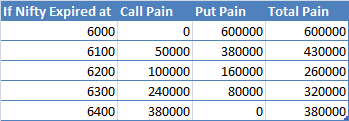

If the Nifty were to expire today at 6,198 (today’s price) what would the impact be?

- The 6000 call is “in the money”. The other two are not. (Their strike prices are above the expiry price). Therefore, we take the Call OI at strike 6,000 (500) and multiply it with the amount of money these call owners would make (Rs. 198 per position) to get a “Call pain” value of Rs. 99,000.

- For puts, we see that the 6200 is in the money (2 rupees above the expiry price) and 6400 put is as well (202 rupees above). So again, we take the Put OI at 6200 (1400) multiplied by Rs. 2, and the Put OI at 6400 (800) multiplied by 202. Thus the Put Pain = 2800+161600 = 164,400.

- If you add these two, you get a Total Pain Value of 263,400.

This is if the Nifty expired at 6,198.

What if it expired at 6300? We can calculate different Pain values, and we’ll see a pain of Rs. 320,000.

Doing this for multiple strikes gives us:

You can see here that the lowest pain is around the 6,200 number. This is in fact the “Maximum” pain level where option buyers will see the least profits. (and option sellers, the least losses).

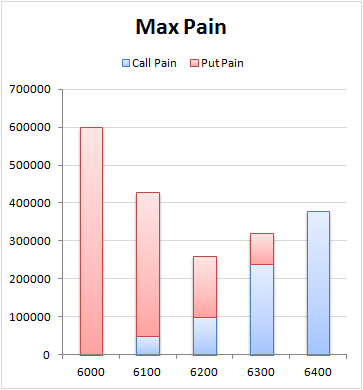

We can see this better graphically:

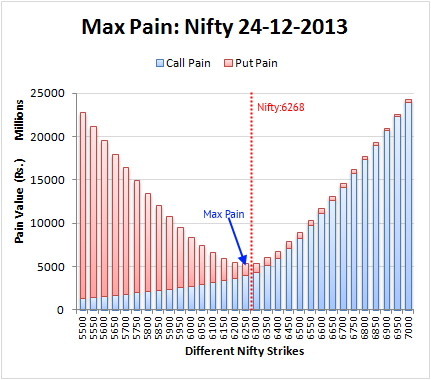

How does this look like, today, for the Nifty?

The option chain for the Nifty derivatives gives me an easy way to calculate this, from the NSE Bhavcopy that is downloadable every day. Nifty options are very liquid, and let’s just take options with expiry dates of today. We can use the above method to get the Pain Graph, which is:

The max pain value is around the 6250 levels. The Nifty is at 6268, which is a tad higher.

So is the Nifty Going To Fall?

Wait wait. The only way to know is to see if the Nifty converges with Max Pain value by

a) The Nifty Moving towards it

b) the Max Pain Value moving towards the Nifty.

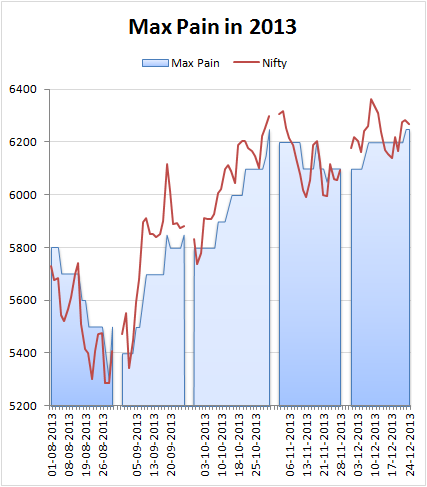

Let’s quickly look at the max pain value in the previous F&O period (November) to see how it moved with the Nifty.

The Answer

While the correlation exists, the Max Pain value has not been a good leading indicator. October is a case in point – till two days ago, the Max Pain dicated a close of 6100, but the market closed above 6250. In November, the Max Pain did give a solid indication. September was a basket case as the Nifty remained firmly above the Max Pain rates for most of the month.

The Max Pain numbers aren’t sacrosanct for pointing out direction. One of the reasons I did not do this post earlier was that the Max Pain number has been misleading.

The December Expiry is on Thursday, with a holiday tomorrow. We don’t see a major move with Max Pain in any case.

However, this is useful information to know; if you hear that “Options Indicate a move to X” – a quote often made using Max Pain statistics – you will know that recently at least, the data doesn’t give us the correct picture.

But the Option MaxPain seems to act as a good “barrier” for support or resistance, so the short term move might be limited on the upside or downside by the Max Pain value. This is useful information to take on call or put spreads closer to expiry.

Note: I’ll add more computing power and will plot a more longer term picture of expiry versus Max Pain values for the last 3 years, in a subsequent post.

![]()