As you may already know, we will be sunsetting our research services in September 2025, also marking the end of all our premium portfolios including the Focused portfolio. As communicated earlier, we are suggesting two alternative mutual funds that could serve as a suitable replacement for the Focused Portfolio. As the current market conditions may be giving some good opportunities to top-up into the equities.

With that in mind, we are here with a post about two funds whose strategies closely align with the Focused framework.

The focused portfolio has been around for nearly six years, including its earlier version as LT Multi Cap. Our investment approach is built on three key principles. First, we prioritize a company’s growth potential. Growth is central to our strategy, but not all high EPS CAGR stocks fit our criteria. We look for sustainable growth driven by market expansion or competitive gains. Understanding what fuels this growth helps us identify strong investment opportunities.

Second, we consider market sentiment and sector trends. Markets move in cycles, and while short-term fluctuations happen, broader trends matter. Factors such as interest rates, GDP growth, and FII flows shape overall sentiment, which can also be sector-specific. Finally, we weigh opportunity costs.

With that in mind, let us begin with what we all are here for, ‘The two alternative funds’.

Kotak Emerging Equity Fund

The Kotak Emerging Equity Fund is an equity mutual fund managed by Kotak Mahindra Mutual Fund, primarily focused on large and midcap companies—where “large” refers to the top 100 stocks. Launched on January 1, 2013, the fund has consistently been one of the better performers in its category. As of February 2025, its AUM is worth ~ 49,000 Cr.

In January 2024, the fund underwent a management change, with Atul Bhole taking over as the fund manager. Bhole, who previously worked with DSP Asset Management, brings 18 years of experience to the role.

The fund follows a Growth at a Reasonable Price (GARP) strategy, integrating both top-down and bottom-up approaches in stock selection, with a strong focus on quality and growth.

*Source: Morning Star. Click on the image to enlarge.

*Source: Morning Star. Click on the image to enlarge.

The fund maintains a diversified portfolio of about 80 stocks, with top-weighted stocks ranging from 3.5-4%.

Below is a table that classifies the portfolio holdings in terms of market cap.

*Source: Kotak Mahindra Mutual Fund. Click on the image to enlarge.

Let us also have a look at its Factor Profile as well as Sector Allocation.

*Source: Morningstar. Click on the image to enlarge.

As seen in the chart above, the fund has historically leaned towards growth, momentum, and quality while maintaining low volatility—an approach we appreciate. The size factor also falls somewhere in the middle, striking a balance that aligns well with our preferences.

*Source: Morningstar. Click on the image to enlarge.

The fund has a diversified sectoral allocation with multiple sectors that we are bullish on focused too including Consumer Cyclical, Real Estate, Energy, Industrials, Healthcare, and Utilities, among others.

Let us now move to the second fund.

PGIM India Midcap Opportunities Fund

PGIM India Midcap Opportunities Fund is another Equity Mutual Fund managed by PGIM India Mutual Fund, again focussing on large and midcap space. The fund was launched in Dec 2013, and as of Feb 2025, its AUM has grown to ~10,400 Cr.

The fund maintains a cost advantage over its competitors, being priced within the lowest quintile among its peers. Strategy-wise, the fund seems to be overweight on growth while having a low exposure to yield.

*Source: Morningstar. Click on the image to enlarge.

Another notable strength is the size of its portfolio management team, with four portfolio managers overseeing the fund, the fund seems reasonably well-resourced compared to many of its peers. Puneet Pal is the longest-tenured manager, bringing over 20 years of experience in listed portfolio management.

Here are its holdings classified across size:

*Source: PGIM India Mutual Fund. Click on the image to enlarge.

Similar to the previous fund, the PGIM Fund also has a portfolio allocation heavily skewed towards growth stocks, reflecting its strong emphasis on capital appreciation over time.

*Source: Morningstar. Click on the image to enlarge.

Its factor profile too, aligns well with our preferences, with a strong tilt towards growth, momentum, and quality, while yield and volatility remain on the lower end. Size, on the other hand, sits somewhere in the middle, maintaining a balanced exposure.

*Source: Morningstar. Click on the image to enlarge.

Comparative Analysis

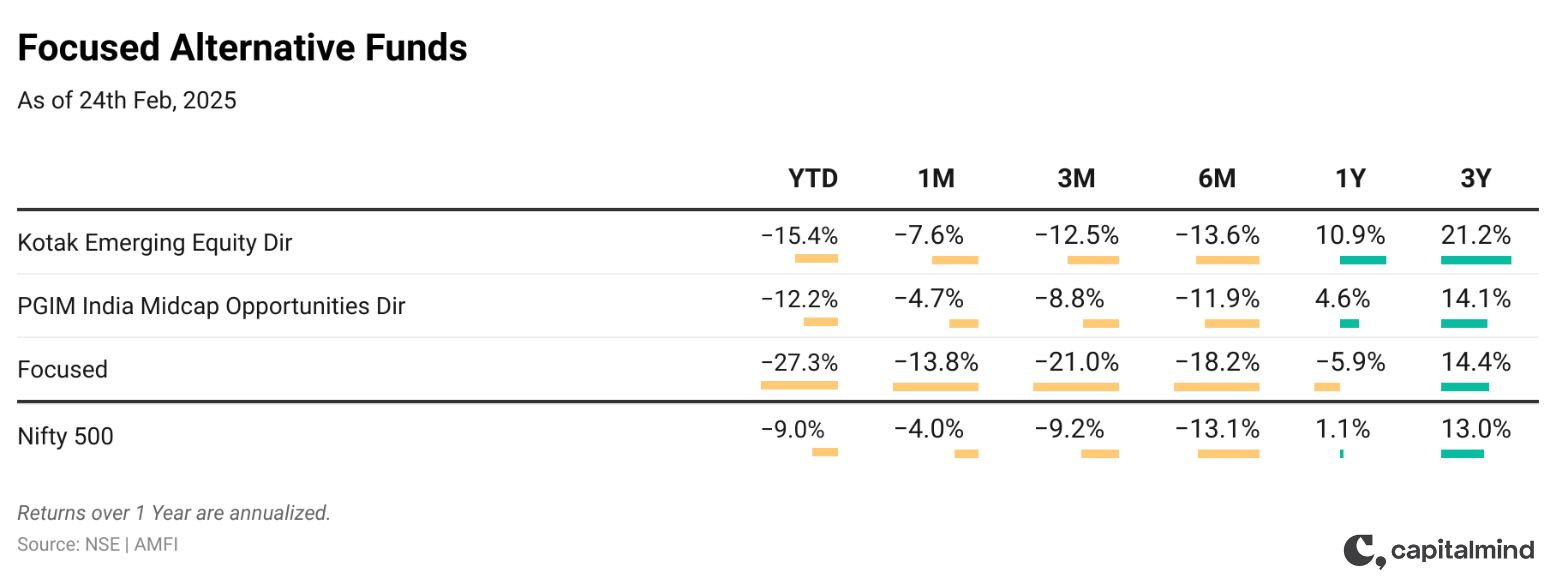

Let us now do a comparative analysis of both the funds along with the Nifty 500 as a benchmark. We are considering the Nifty 500 as the benchmark as it best aligns with the investment universe of both funds.

*Click on the image to enlarge.

*Click on the image to enlarge.

Both the funds have felt the heat in recent times due to the ongoing market correction. However, over a three-year period, both have successfully generated alpha, with Kotak Emerging Equity Fund outperforming PGIM India Midcap Opportunities Fund. That being said, when looking at one-month, three-month, and six-month performance, the PGIM fund has experienced a lower drawdown compared to Kotak.

Let us also have a look at its 1-year rolling return curves in the last three years. *Click on the image to enlarge.

*Click on the image to enlarge.

Why These Two Funds?

As we said at the start of this post, nothing could have been better to continue this journey together. However, this is not the case, and for the same reasons we have identified these two funds, which can be potential alternatives to the Focused portfolio when it ceases to exist.

The reason behind choosing these two funds? Short and Simple – The Framework – in terms of the type of approach it follows, sector preferences as well the universe of investment closely aligns with what we try to do in Focused.

Alternate Option 3: Surge India PMS

Not a plug, but if you are looking to own direct stocks, take a look at Surge India—our fundamental PMS strategy. If interested, let us know here, and our team will get in touch.

before we wrap up,

A quick note from Krishna

It’s been a tough couple of months—no doubt about it. And we don’t know when this downturn will end. Right now, there’s nowhere to hide—every stock, every sector is under pressure. The only thing that keeps us steady in times like these is our conviction in the businesses we own. Are they still on the growth path we projected? Has anything fundamentally changed? If the answers remain the same as they were six months ago, then our job is to stay the course, hold tight, and let the market find its bottom. That’s exactly what we are doing.

There always comes a moment when it feels like nothing will go right, tempting investors to give up. Ironically, those moments are often the best times to stay put. Right now, sentiment is overwhelmingly negative, and your gut might be telling you to sell everything and sit on cash. But that may not be the right strategy. In the near term, volatility and underperformance could persist as global uncertainties—trade wars, tariffs, and macro concerns—play out. However, history has shown that the right move in such periods is to ride out the volatility, navigate the panic, and position for the future.

Looking a year ahead, we still expect our portfolio holdings to deliver above-average earnings growth. While the current market correction is painful, it doesn’t shake our core principles. These are strong businesses with solid earnings visibility. Ultimately, the market follows earnings, and once stability returns, recoveries tend to follow.

For existing investors, you may consider deploying fresh capital into the mentioned funds while continuing to hold existing Focused holdings. Let’s see how things evolve in Q4.

This too shall pass!

Disclosure: I, Sidhanth Paul, Research Analyst, author, and the name subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific view(s) in this report.

Research Analyst or his/her relative or Capitalmind Research LLP does not have any financial interest in the subject company. Also, the Research Analyst, his relative, Capitalmind Research LLP, or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further, Research Analyst or his relative or Capitalmind Research LLP or its associate does not have any material conflict of interest at the time of publication of this research report.

Capitalmind Research LLP is a SEBI Registered Research Analyst, having registration no. INH000014003.