🔆 Saturday Coffee Newsletter

- Market Overview: Marketcap analysis & asset classes

- World View: Banking is a game of confidence

- Good Reads: 5 articles on investing & more

- Pop Quiz: Answer and win a cool prize!

What’s up with markets? 📉📈

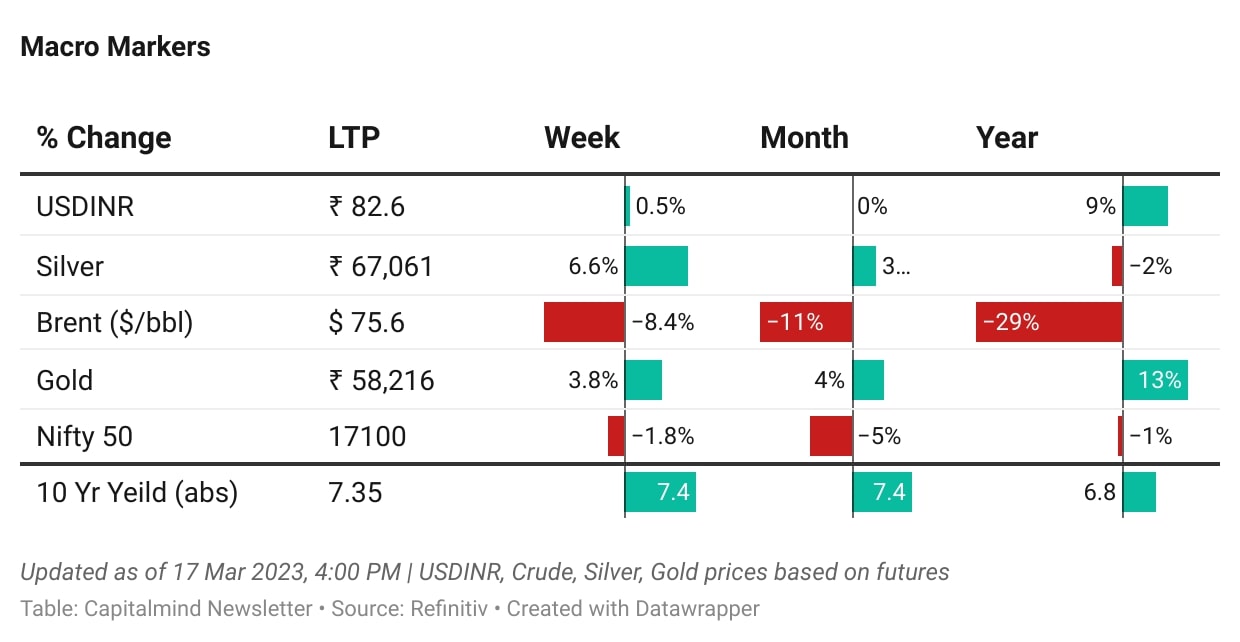

While the US economy struggled with a banking crisis of sorts, Nifty 50 also felt the turbulence as it corrected by 1.8% for the week. Crude was also down 8.4% over the last week and it’s down by 29% over the last year.

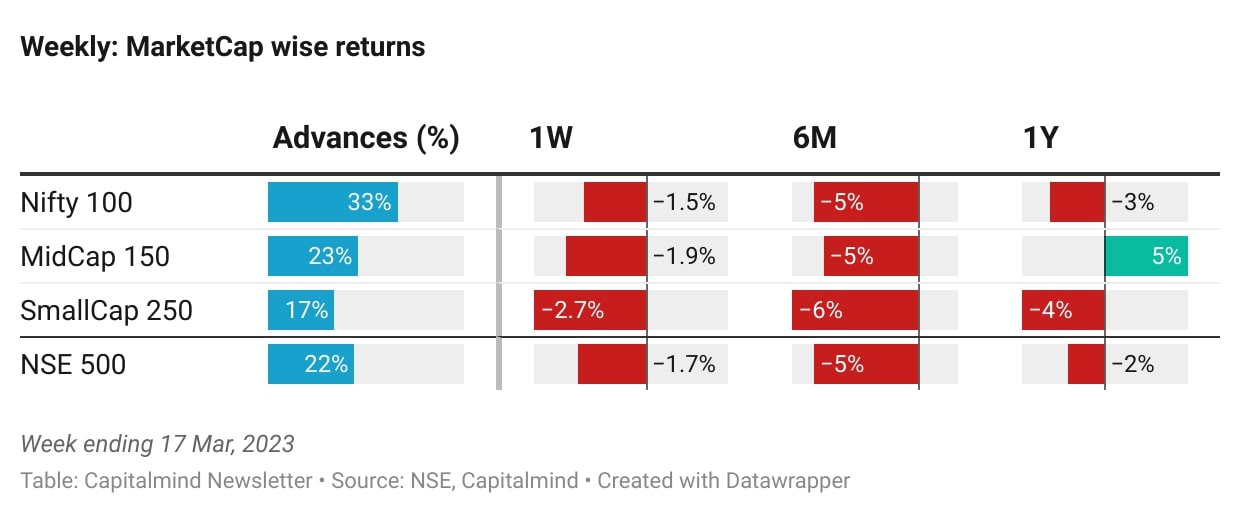

Looking at the broader market of top 500 NSE stocks, the NSE 500 index was down by 1.7%. 22% of all NSE 500 stocks advanced while 78% of them declined.

Breaking down the stocks as per marketcap, we see that Smallcap 250 index was hurt the most last week as it lost 2.7% with 83% of these stocks declining.

Banking – a game of confidence 🏦

Confidence in the bank’s competency to steward its customers’ money: Banks are highly levered businesses, which owe and lend much more money than their capital bases, inherently assuming these bases to not be enough to cover an exodus, but sufficient enough to cover normal withdrawals under normal conditions.

A typical bank takes in deposits, and loans out most of it at a higher interest rate than what it pays to its depositors. It invests what it can’t lend, again trying to make more than it has to pay its depositors.

But Silicon Valley Bank wasn’t a typical bank. SVB was the bank to startups, as it was tech-friendly, and because VCs nudged their startups to park their money with the bank. Thanks to a surge in funding during the pandemic, startups found themselves cash-rich. Thus, SVB’s deposits tripled to $189.2 billion by end 2021, versus $61.8 billion at the end of 2019.

With money flooding in, SVB couldn’t lend fast enough. Its loan book “only” doubled to $65.9 billion in 2021, versus $32 billion in 2019—prompting it to invest much of the $97.6 billion odd rest in credit-safe, but rate-risk heavy places, such as in long-term government bonds and mortgage-backed securities.

But here’s the precarious situation it found itself in: Central banks raised interest rates at a pace unheard of, causing the value of its investments to fall. And with startups facing funding difficulties, their withdrawals from SVB exacerbated the bank’s troubles.

All this while, SVB could see its deposits bleeding and investments frailing, but it did not come out of its paralytic state. Not until it was too late.

Confidence in bankers making smart decisions: When push came to shove, SVB finally acted by liquidating some of its investments at a $1.8 billion loss and announced its intent to raise another $2.5 billion. Given recent failures at another bank Silvergate, venture capitalists and their portfolio companies, effectively the bank’s major depositors, gave into a panic.

If you have to pick a moment marking the beginning of the “run” on the bank, despite its simmering issues for some time, this was it. In hindsight, it seems, a bank raising money when another has failed is asking for the first domino to fall in its proverbial downfall.

Confidence in claiming your money, and in the system: There’s just a natural tendency to feel safe about your money sitting in a bank deposit. Depositors know, or at least feel, that when all hell breaks lose, there are guardian angels in the sky watching over them. The only problem was, many of the deposits at SVB were beyond the $250,000 insured under such protections by the Federal Deposit Insurance Corp.

And yet, eventually, the FDIC ensured that all deposits, including the uninsured, would get their money. Because confidence in the system supersedes all else.

But what’s striking about this saga is just how quickly, it unfolded—the shakeout of confidence and the bailout, all happened within a 72-hour span.

In the Twitter age, with information and certainly panic spreading like wildfire, it just makes you wonder whether everything in finance will keep getting exponentially expedited.

And to reciprocate on the regulations front, William Isaac, ex-chairman of the FDIC, was quoted by Bloomberg saying, “It’s almost unheard of for the FDIC to come in and bail an institution as quickly as this.”

Read more: What we should not learn from the SVB crisis

What we are reading 📝

(If you’re reading this on the website and want to participate in the quiz, subscribe to the newsletter.)