While the pandemic has hit the travel and tourism sector the most, this New-Delhi-based travel-tech company – Easy Trip Planners Ltd. has reported multifold growth in its profits. Easy Trip Planners, the holding company for online travel portal easemytrip.com, offers a range of travel booking services such as flights, hotels, visa processing, insurance, etc.

In a year, where the airline and the hotel industry have been reeling under losses, what helped Easy Trip – which earns commissions of them – to almost double its profit and how far is it sustainable? Let’s find out…

Easy Trip Planners is India’s second-largest Online Travel Agency (OTA) and generates most of its revenue by selling air tickets.

The company earns revenue in the form of commissions and incentives from the airline tickets booked by customers. Commissions and incentive payments include performance-linked bonus, which is paid by distribution service providers and certain airlines as well as credit card companies on a periodic basis, generally based on the volume of sales. It also earns revenue from convenience fees, cancellation service charges, rescheduling charges, and advertisement revenue.

Industry: Fragmented & Competitive

The OTA industry is fragmented, competitive, and with hardly any customer loyalty.

The segment is flocked by numerous established and emerging competitors, including other online travel agencies, traditional offline travel companies, travel research companies, payment wallets, search engines, and meta-search companies, both in India and abroad. Along with these, even large established internet search engines have also launched applications offering travel products in various destinations around the world.

Air ticket booking is a highly price-sensitive business. Customers run to the cheapest venue and loyalty is generally low.

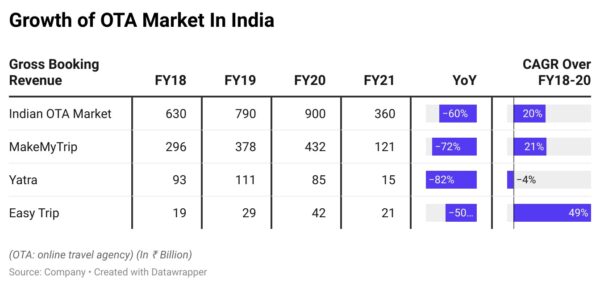

The Indian OTA market measured by gross booking revenue has grown at a CAGR of 20% over FY18 to FY20. The growth was led by a rapid increase in affordable access to the internet, increasing smartphone penetration, growing awareness and comfort of online transactions, competitive prices offered by OTA players to attract consumers, and a growing network of service providers on OTA platforms.

The air ticketing segment accounts for approximately 51%-53% of the Indian OTA industry. This is because the OTAs started operations by selling airline tickets as the airline services industry is organised with a limited number of players and it is relatively easier to list airline ticket inventories online. On the other hand, the hotel industry is fragmented with several branded and unbranded players. Hotel bookings account for 37%-38%, while the remaining is from rail, bus, etc.

In FY18 MMT/Yatra’s air ticketing gross booking revenues were 9.2x/4.2x that of Easy Trip. This has eventually reduced to 3.5x/0.6x, in FY21. This means that the gap is narrowing, and Easy Trip has been continuously gaining market share.

What’s Different

The bootstrapped tech company provides customers with the option of no-convenience fees when there are no alternative discounts.

Generally, other OTAs and airline websites charge a convenience fee of ₹ 300 per person, while booking a domestic flight ticket. EaseMyTrip waives this fee. However, other OTAs, most of the time, offer either an internal discount or some external discounts. When it comes to external discounts, there are various terms and conditions – specific accounts with a bank or payment gateway and/or credit cards and minimum booking value.

Sometimes, internal discounts offered by other OTAs set-off’s the entire convenience fees. However, internal discounts vary route-wise and airline-wise

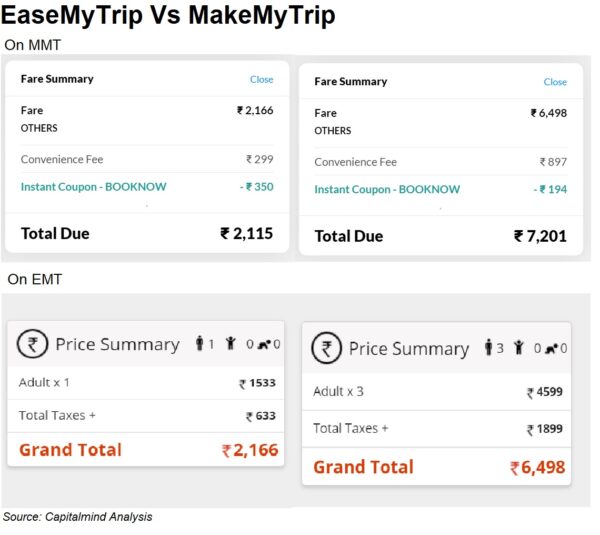

For instance, we tried to book a Mumbai to Bangalore flight on EMT and MMT (MakeMyTrip, a US listed competitor) for one person and three people to see the price difference. While booking for one person, the ticket price on MMT turned out to be cheaper as compared to EMT, because of the internal discount offered. However, while booking for three people, the final ticket price on EMT was cheaper as the internal discount offered by MMT did not completely set-off the convenience fee charged.

MMT, while booking for one person, offered an internal discount of ₹ 350 and charged a convenience fee of ₹ 300. In case of three people, MMT offered an internal discount of ₹ 194 and charged a convenience fee of ₹ 897.

When it comes to EMT not charging convenience fees, there is a catch to it.

If an individual avails of any other external discounts, then he/she will be charged a convenience fee and if an individual cancels the ticket, then he/she will be charged a cancellation fee.

Every booking made on EaseMyTrip is subject to cancellation charges levied by the airline, which may vary with respect to flight and booking class. EaseMyTrip.com levies negligible amount of ₹ 300 per passenger/per sector for domestic and ₹ 500 per passenger/per sector for international air tickets as cancellation service charges.

EaseMyTrip Website

If an individual has not paid any convenience fees, then this is not different from what other OTAs do. They just don’t refund you the convenience fee charged if a flight ticket is cancelled.

Thus, usually, a person benefits from booking tickets on EaseMyTrip in case of group bookings and when the internal/external discounts are much lower than convenience fees – which is the case most of the time.

Hence, the company has witnessed a higher growth in air ticket bookings on its website.

The Growth In Financials

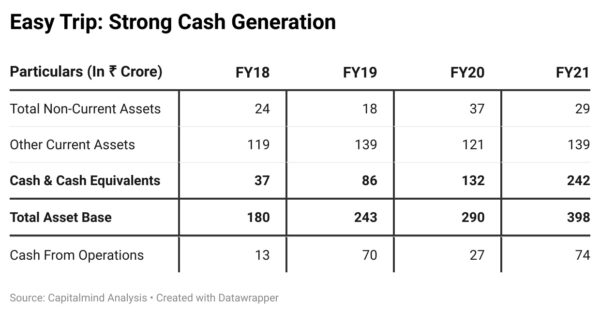

Easy Trip has been a profitable and cash-generating company, unlike other listed players in the industry.

Its cash balance as of March 31, 2021, stood at ₹ 242 crore, translating to a cash value of ₹ 22.3 per share on a diluted basis. As it is an asset-light business, cash forms nearly three-fifths of the total asset size. The company has also been generating cash flow from operations.

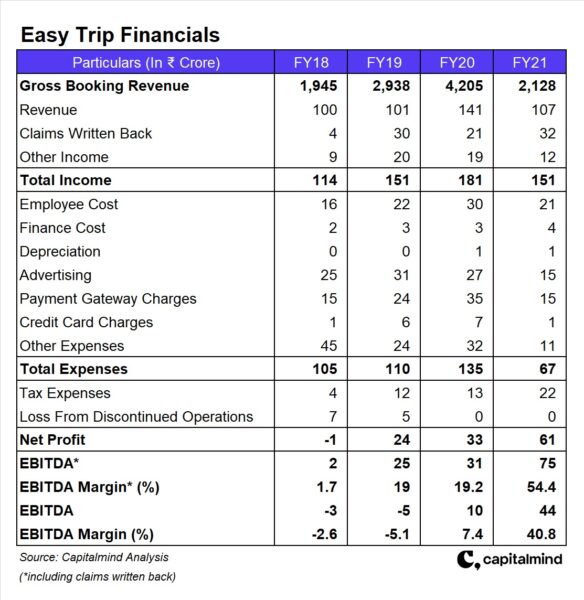

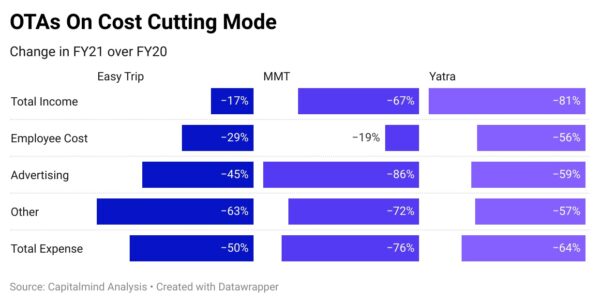

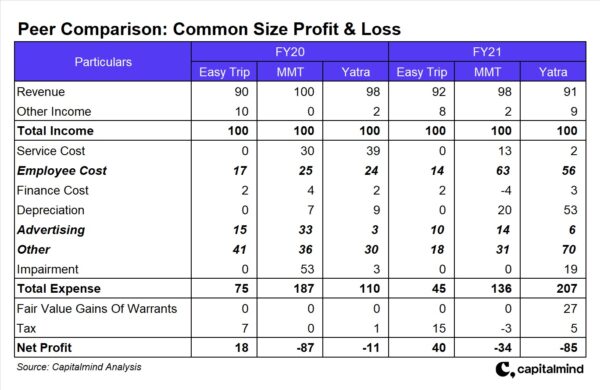

The profits of Easy Trip have seen a big boost in FY21 on the back of lower expenses. Lower employee, advertising and other costs, credit card and payment gateway charges almost doubled the company’s net profit in FY21.

Employee costs were lower as the company reduced its workforce and had cut salaries for few months during the first covid wave. Credit card charges reduced as customers have been opting more for UPI payments. Payment gateway charges have fallen drastically due to lower bookings done during the year. However, payment gateway charges as a percentage of gross booking revenue have been reduced by only 13 basis points to 0.7%.

Advertising is a discretionary spend. Due to Covid-19, the company took a cautious call to spend less on advertising. Other expenses were lower as the company from FY21 has stopped paying commission to its traditional travel partners.

On the income side, other than the regular revenue, claims written back also form a major part.

Claims written back is unadjusted credits from airlines related to the cancellation fee, which the company records as revenue after two years from the refund date. The company claims the same to be a regular income and a normal revenue line item. However, due to accounting policies, it is shown under other income.

What Exactly Is Claim Written Back?

It does consist of the cancellation fee, but mostly it consists of claims which usually a passenger fails to collect from airlines in case of a missed flight or no-show – ticketed passenger does not show up for their flight. In case of a missed flight/no-show, a passenger is entitled to a refund of all statutory taxes and user development fee (UDF)/airport development fee (ADF)/passenger service fee (PSF).

Easy Trip allows a passenger to claim these refunds for a period of two years from the date of cancellation. It is only post that, they consider it as revenue.

Thus lower the cancellations/missed flights/no-show, lower is the revenue from claims written back.

In earlier years, the company did get involved in other business activities like coal trading, movie production, and share trading. However, the same has been stopped and in FY20 and FY21, the company was not involved in any other activities other than a travel agency.

What Makes Easy Trip Profitable Compared To Peers?

Its lean cost structure compared to peers. In FY21 compared to FY20, even MMT and Yatra were able to reduce their costs. However, they still reported losses.

Easy Trip’s lean cost structure is on the back of lower spending on the service cost, employee cost and marketing, and other expenses, as compared to MakeMyTrip and Yatra. The service cost line item is missing as Easy Trip does not have any major income from hotel bookings.

Final Thoughts

The OTA space has and could continue to remain competitive. However, without any external funding, Easy Trip has survived and increased its market share. In fact, it is now the second-largest in air-ticketing after MMT. The segment will remain competitive but given the fact that Easy Trip has already successfully built its business, it will grow with the growing travel and tourism segment. Moreover, the company is also looking to acquire and expand in non-air bookings – hotels, buses, etc. It aims to generate one-fourth of its revenue from the non-air ticketing segment in the next 3-5 years, from current 2-3%.

On the financial side, the topline was subdued as fewer people traveled in FY21 due to Covid-19. The same is expected to be the case at least in H1FY22. With no third wave of covid virus, travel could be boosted in H2.

On average 1.7 lakh people flew daily in FY21. So far in FY22, the number is lower at 1.23 lakh. This is because of the second covid wave and monsoon season when air travel is generally low. We do not expect much change in its financials in FY22.

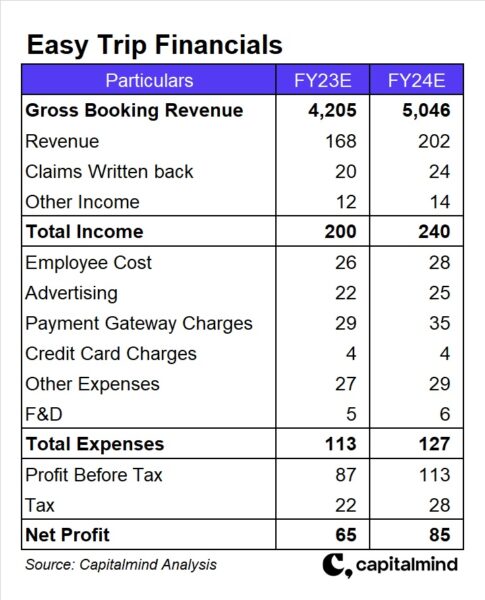

We expect travel to reach pre-covid levels in FY23. So, we have tried to predict what profits the company could earn in FY23, keeping FY21 and Q4FY21 expenses as the base.

In FY21, the company earned a commission of 5% on gross bookings. For FY23 and FY24 we expect the same to moderate to 4%. Income from claims written back is also expected to be lower in FY23 and FY24 as fewer people flew in FY21 and FY22.

On the expenses side, employee, advertising, and other expenses are assumed to be equal to the amount spent by the company in Q4FY21. Payment gateway charges are generally 0.7% of the gross booking amount. Finance cost and depreciation are expected to be at the same level.

For FY24, gross booking is expected to increase by at least 20%. While major expenses are expected to be 10% higher compared to FY23. The tax rate is assumed at 25%.

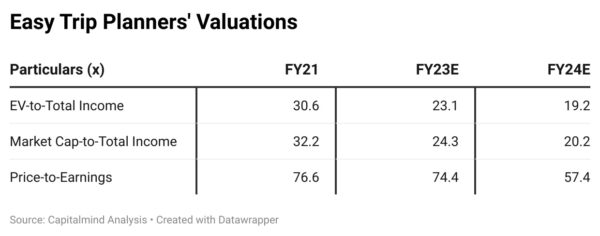

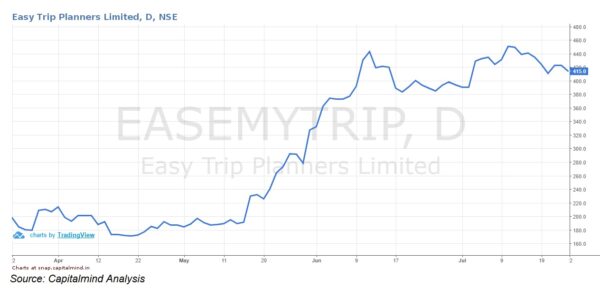

On the back of the reopening narrative, Easy Trip’s shares nearly doubled since listing. This had made the relative valuations a bit high. Among the facts that it is the first company from OTA space to be listed in Indian markets and it is the only profitable listed OTA, the buoyant mood on the street has also worked in the favour of its share price.

Even based on FY24 expected earnings, the valuations look pretty much full. Especially, when there is no incremental information given by the company which could have increased the visibility. Expanding in the non-air ticketing segment could drive growth, but the same could also bring in additional expenses.

We like the business, its lean cost structure, and the growth opportunities. However, the valuations seem to be on the expensive side right now. We will be closely tracking the stock and wait for a better entry point.

Other Related Posts:

June – A month of slapshots for CM Focused & CM passive

Which is the best REIT in India?

An Experimental Trade: Rising Oil Enough For A Rerating?

Xelpmoc: The X factor of India’s start-up ecosystem

Mahanagar Gas: Stands out among City Gas Distributors

This article is for information only, and should not be considered as a recommendation to buy or sell any stocks. Stocks mentioned maybe part of Capitalmind Premium Model Portfolios

For immediate access to probably, the best platform in India for active investors, join Capitalmind Premium: Model Portfolios, Premium Research, and a vibrant member community.

For any questions, tweet / DM us on twitter or email us at premium [at] capitalmind [dot] in.