Few years back a wise investor told me – “Money is not in Power generation, but in transmission”.

Today we have, India’s largest power transmission company coming up with an InvIT IPO.

InvITs are new to Indian markets. We had seen two listings in the last few years. While IndiGrid InvIT had a decent run, IRB InvIT failed to gather investors interest.

So, Should you subscribe to the Powergrid InvIT IPO?

Short Answer: Yes. The IPO is well priced & provides a decent yield. However, the cash flows are due after 3 years which is a risk. We think it is a decent long-term bet.

What is an InvIT?

An InvIT is a hybrid instrument that owns & manages infrastructure assets like roads, power plants, transmission lines, warehouses, ports.

Think of it like a mutual fund that collects money from investors, to invest in long-term revenue-generating assets. It enables individual investors to invest in large infrastructure projects to earn profits in the form of dividends & capital appreciation.

InvITs usually get listed on stock exchanges through an IPO. This serves as a channel to raise equity & debt from the capital markets. The capital is used for growth by acquiring more revenue-generating assets.

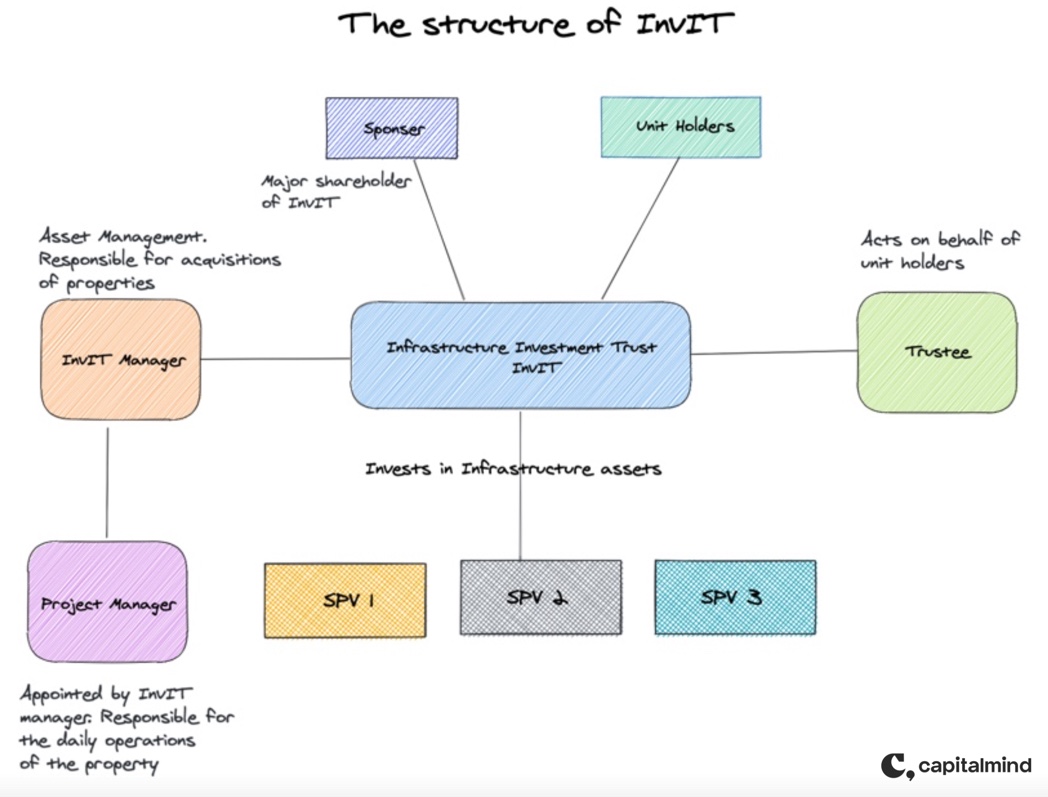

Key parties involved in an InvIT

SEBI requires an InvIT to have a trustee, sponsors, an investment manager, and a project manager. Each of these players has a crucial role to play in the running of an InvIT.

The Sponsor: An InvIT can only be established by a sponsor & cannot have more than 3 sponsors.

- It should have a net worth of 100 Cr

- 5Y experience in development of infrastructure or fund management

- A minimum stake of 15% in the InvIT

Investment Manager: They are responsible for asset management activities like investments & divestments.

- It should have a net worth of 10 Cr

- 5Y experience in fund advisory or infrastructure development

- If the sponsor or the investment manager is not Indian-owned, then any investment by the InvIT will be considered as foreign investments.

The Trustee: It is responsible for holding the assets of the InvIT for the benefit of the unit holders. It supervises the activities of the investment manager and the project manager.

Project Manager: This entity is appointment by the Investment manager. It responsible for managing the assets of the InvIT & to ensure that projects get completed on time.

Predictable cash flows: As per SEBI, InvITs are required to invest at least 80% of their assets in completed & revenue-generating projects. It should not invest more than 10% in under-construction projects. This ensures predictable cash flows & maintaining healthy financials.

High DPU: SEBI requires InvITs to distribute a minimum of 90% of their net distributable cash flows to investors. This results in high distribution per unit (DPU) or simply put – dividends.

Blend of both Debt & Equity: The regularity of payments gives it a touch of debt instrument. At the same time, the unitholder participates in the growth trajectory of the company much like an Equity investor. The growth comes from

- Capital gains

- Increasing DPU

- New asset acquisitions

About the IPO – PowerGrid InvIT

PowerGrid InvIT is sponsored by Power Grid Corporation of India. PGCIL is the largest power transmission company in India with 169,829 km transmission lines & 257 sub-stations. The company is conferred with ‘Maharatna’ status in 2019. GoI owns 51.34% stake in the company.

PowerGrid InvIT owns, constructs, operates & maintains power transmission assets in India. This is India’s first PSU InvIT & second listed power transmission InvIT after IndiGrid InvIT. The offer proceeds will be utilized towards providing loans to Initial portfolio assets for repayment of debt.

Key features of PowerGrid InvIT

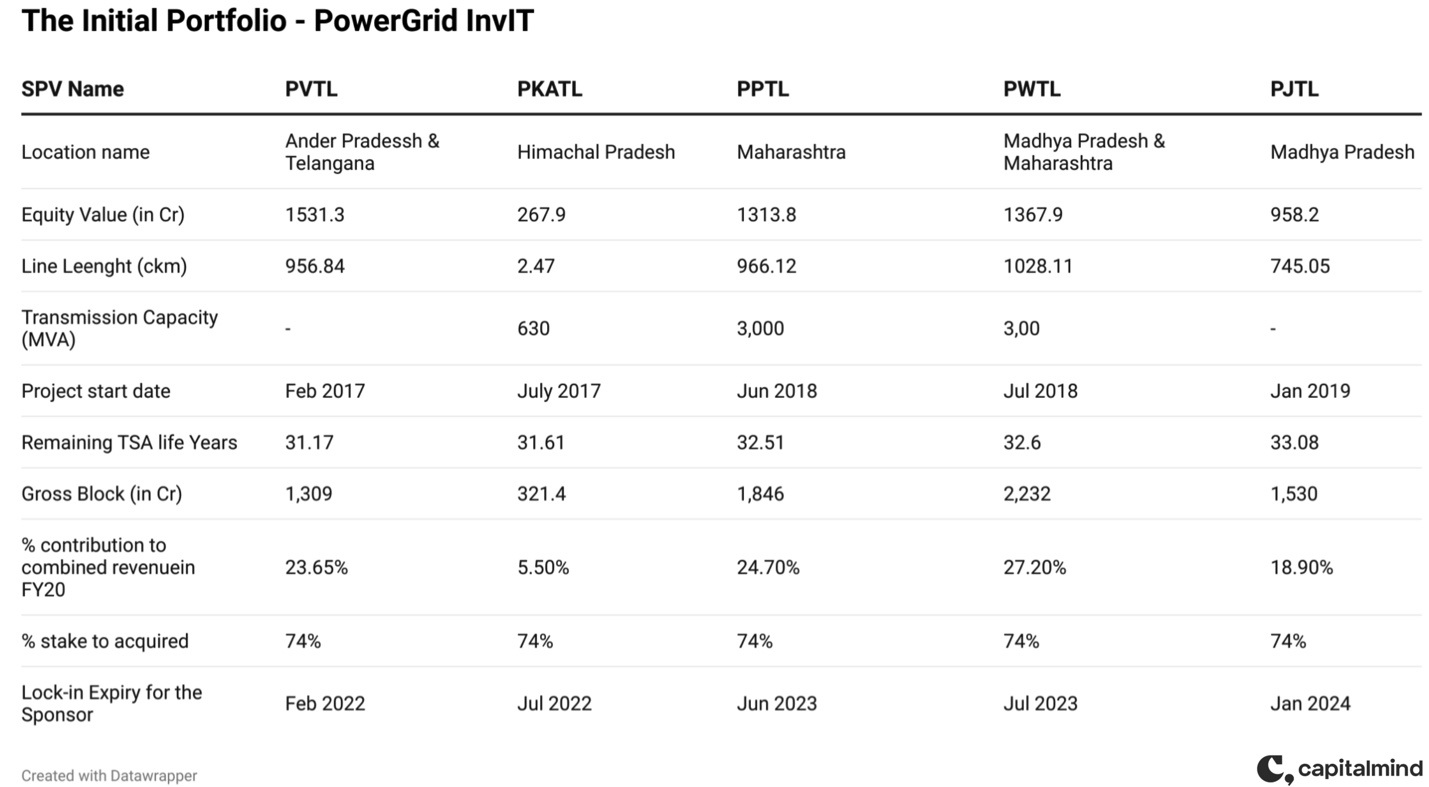

- The current AUM is at 10,384.8 Cr across 5 transmission lines.

- No development risk. The initial portfolio assets are fully operational & revenue-generating.

- As per the TSA (transmission service agreement), the tariffs are not linked to the power transmitted, but to the availability of the grid. The company had historically maintained above 98% availability.

- All the assets are built under BOOM (Build, Own, Operate & Maintain) model. It gives perpetual ownership of the asset to the Trust. Unlike roads which are transferable back to the government after the period of the toll collecting concession.

- The average tenure of TSA is 32 years & extendable up to 50 years. This ensures predictable cash flows for the InvIT.

- The transmission charges are pooled by CTU (Central Transmission Utility) & paid to licenses. Hence reducing the counterparty risk.

- Low debt InvIT with AAA credit rating.

How does this instrument work?

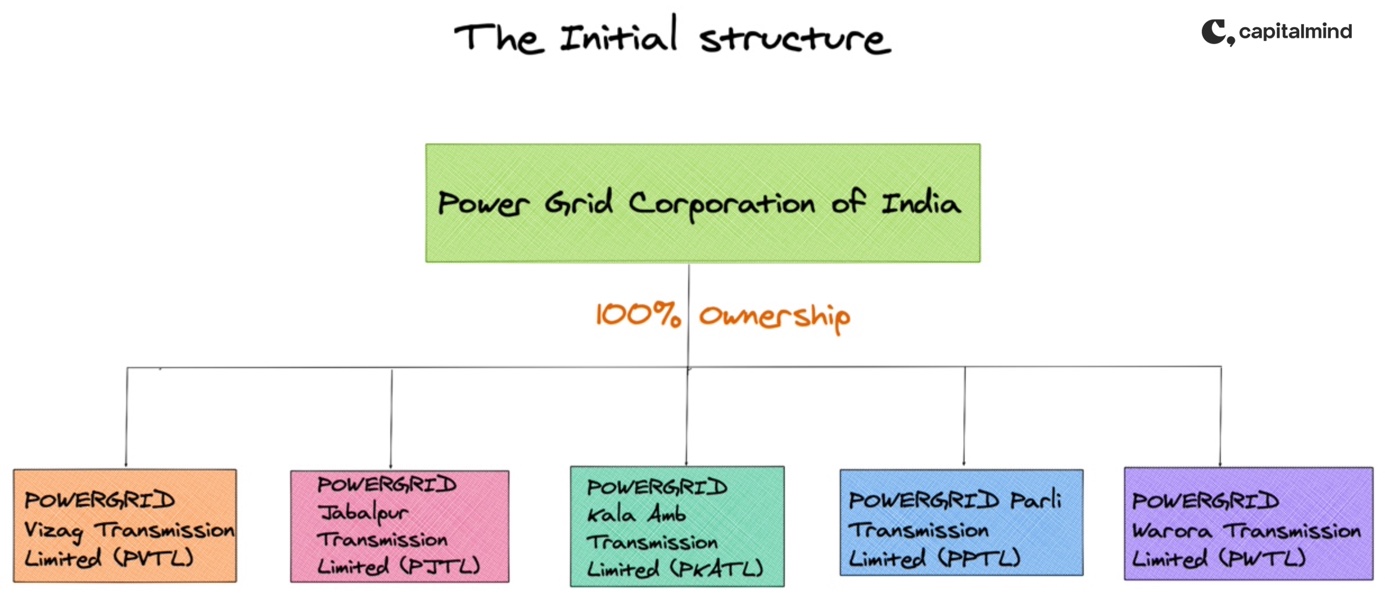

Step 1: Identify the Initial Assets Portfolio

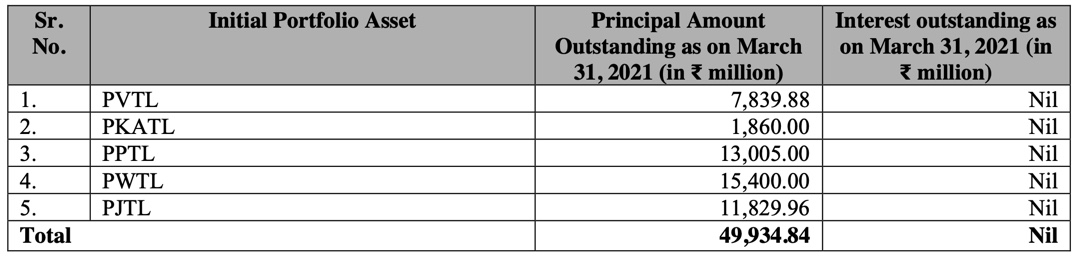

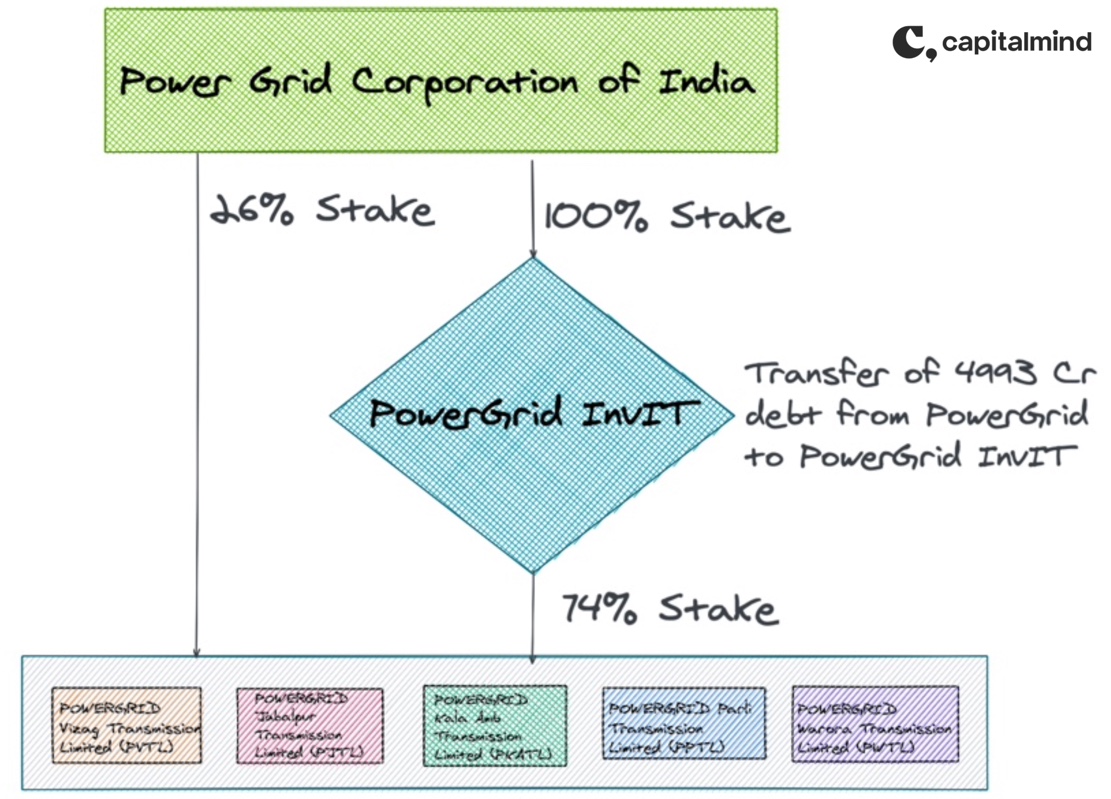

PowerGrid Corporation of India owns 100% stake in 20 subsidiaries. Out of which, the company had initially identified 5 SPVs to monetize.

These 5 SPVs put together has a total debt of 4993.4 Cr.

These 5 SPVs put together has a total debt of 4993.4 Cr.

Step 2: Create an InvIT & transfer the assets

PowerGrid wants to monetize these assets through InvIT route by:

- Transferring of 74% SPVs equity ownership from PowerGrid Corporation to PowerGrid InvIT

- Transferring 4993.4 Cr of debt from SPVs to PowerGrid InvIT

- The remaining 26% stake in the SPVs will also be acquired by PowerGrid InvIT in the next 1-3 years.

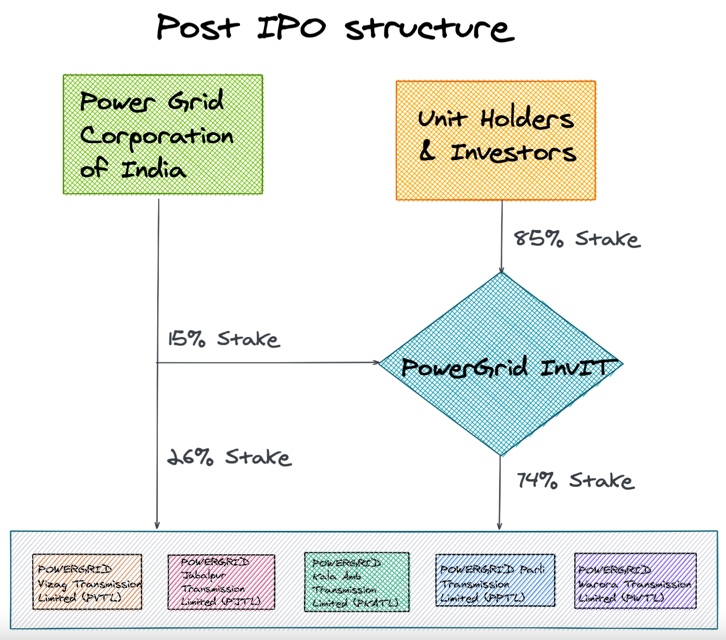

Step 3: Go for the IPO & sell the stake in the InvIT

PowerGrid Corporation is offloading 85% of its stake in the InvIT in the IPO.

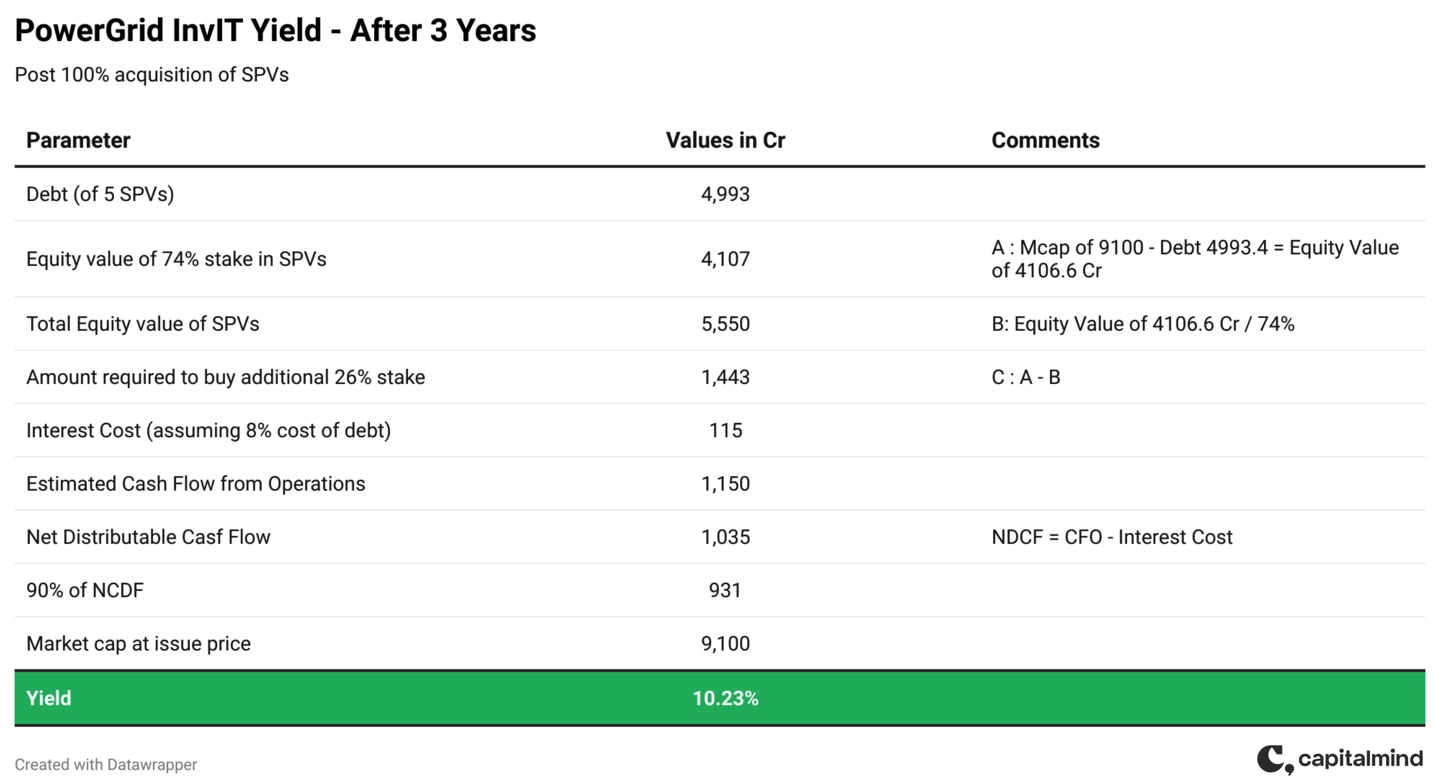

What is the current yield?

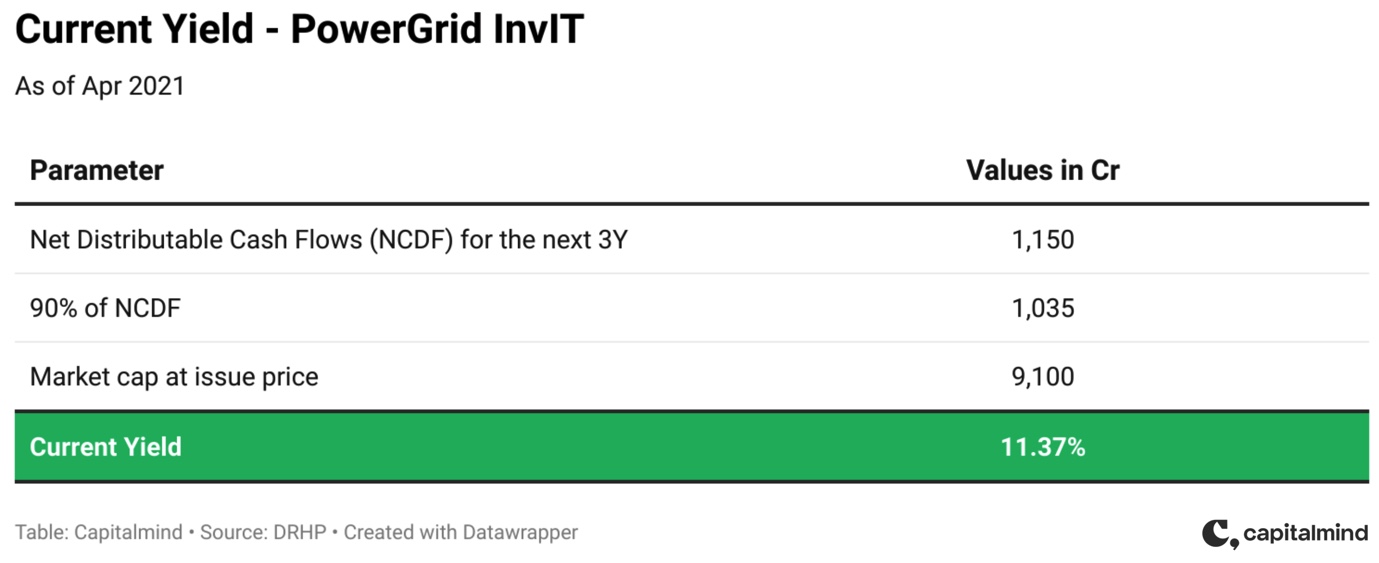

- The Trust is estimated to generate 1313.7 Cr in revenue & 1208.5 Cr in Cash flow from operations in FY22E.

- The Net Distributable Cash Flows (NCDF) will be approx 1150 Cr for the next 3 years. Unitholders are entitled to receive 90% of NCDF i.e 1035 Cr every year.

- At an IPO price of 100/- per unit, the market cap stands at 9100 Cr. This gives us the current yield of 11.37%

11.37% yield is juicy right. Well, let’s not get too excited.

Remember we discussed that, “The remaining 26% stake in the SPVs will also be acquired by PowerGrid InvIT in the next 1-3 years.”

InvIT has to raise debt to fund these acquisitions. This will increases the finance costs & decrease the net distributable cash flow (NCDF). So, let’s see what will be the yield post 100% acquisition.

10.23% still looks good right. Sorry to say, we are not there yet.

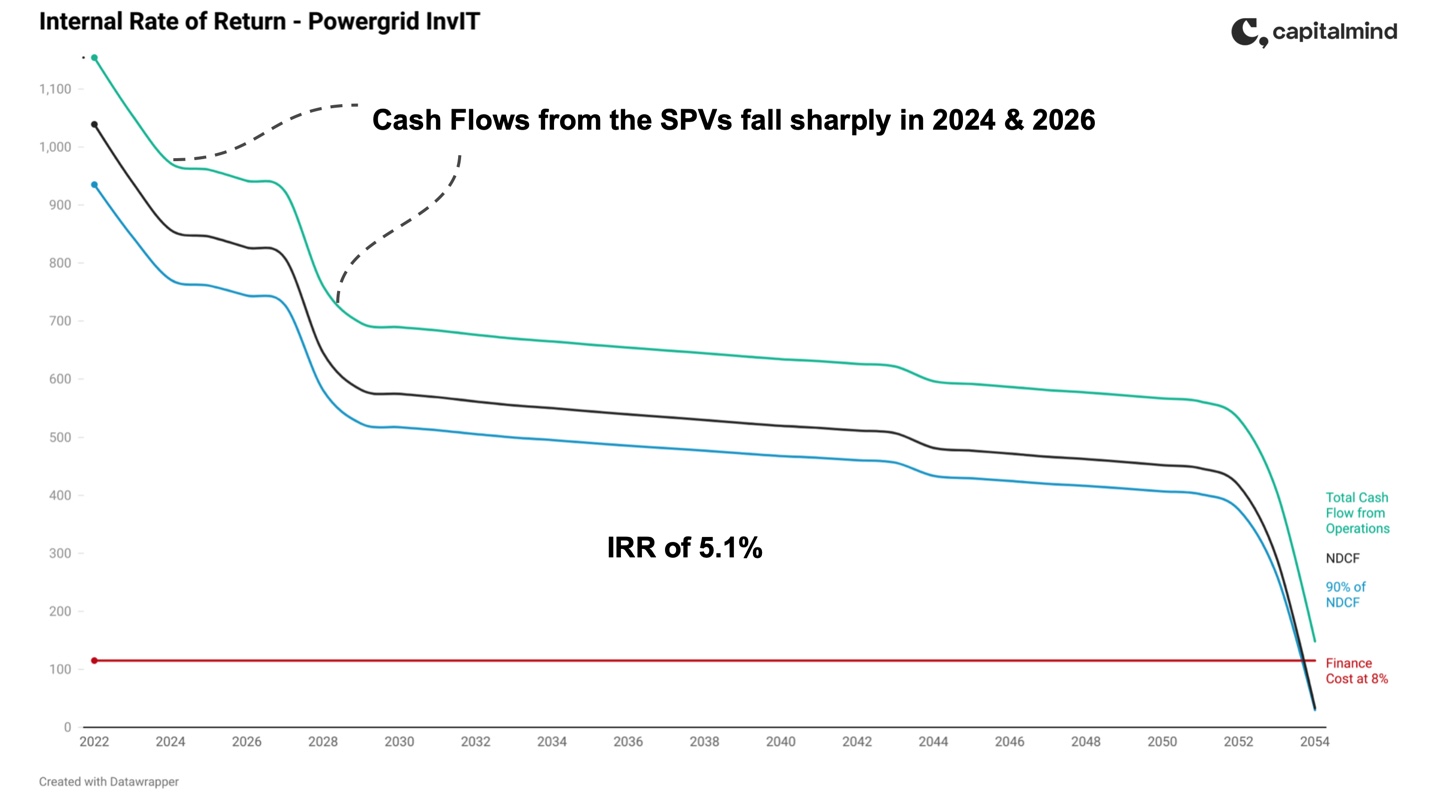

Now let’s look beyond 3 years. What is the expected IRR if we held on to this asset till perpetuity?

- The company is going to witness huge drop in cash flows from 2024 & beyond.

- Assuming that the InvIT is not going to acquire new assets, the IRR comes to around 5.1%.

This IRR is based on holding to maturity with the current assets. This information was gleaned from the valuation document as part of the DRHP, but is an estimate of a third party.

The reasons cash flows come down is that there is both maintenance capex and inflation based increase of costs but revenues are fixed for the period. So distributable cash flows will reduce over time.

Growth triggers for the InvIT

The sponsor (PGCIL) has a large portfolio of assets that are available for monetization.

- Operational Projects: 2

- Under construction: 11

InvIT has a potential pipeline of ~22,500 Cr assets in various stages of construction. The InvIT can increase the leverage from current 0% to 70% of asset value. Significant headroom available to finance acquisitions.

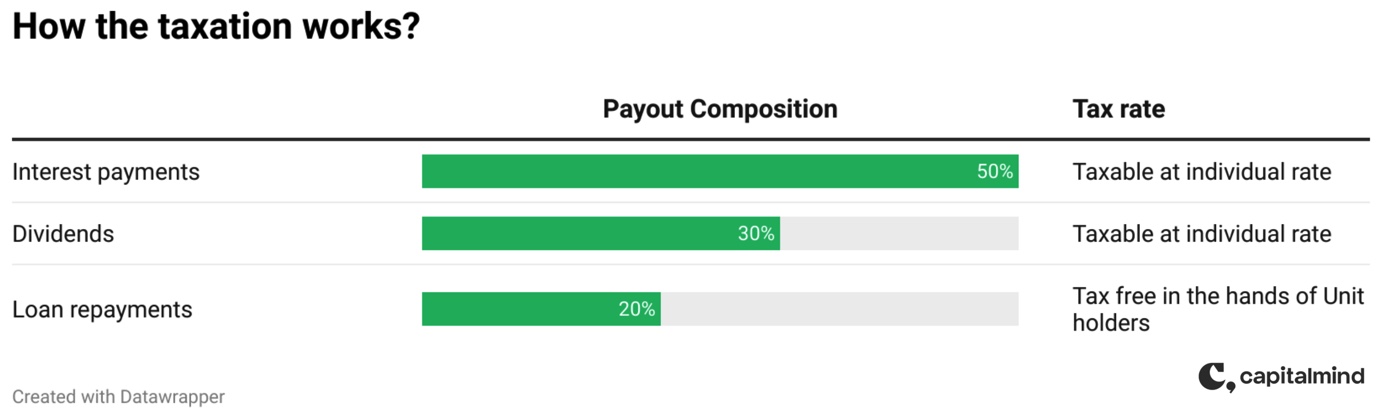

Taxation

The distribution from the Trust to the unitholders will have the same structure as the distributions it had received from SPVs.

So the cash inflows in the nature of interest will be treated as interest. Dividends as dividends. Repayments as repayments.

Note: the components of distribution will change over the years. This is only our first year estimate.

Principal is not protected

Note that many people think of this as a fixed income instrument. The principal however is not protected. For many reasons:

- Interest rate risk: A long term product will see a fall in price if market interest rates rise. This happens even for long term government bonds.

- Market risk: The stock exchanges have their own flow of liquidity. If the markets have a problem then prices of this could fall to low levels regardless of the fundamentals of the Invit.

- Technology changes: In a 30 year period, what if the technology for electricity transmission changes dramatically which either needs the Invit to invest more, or that they are made redundant (Wireless transmission for example). This will hurt the distributable cash flows, and thus people will price the Invit lower.

- The risk of a short term view: when, after three or four years of 1000 cr. cash flow if the Invit starts seeing a falling cash flow, you could see the market react in panic and take prices downwards. Case in point: the IRB Invit, which is trading at 50% of its IPO price now that a few assets go out, and the new assets coming in will take another two years.

Our View:

When compared to its peer, PowerGrid is on par with IndiGrid InvIT. Both have long-term cash flow visibility & strong pipeline of assets. IndiGrid is currently trading at 9.86% yield vis-a-vis PowerGrid InvIT yield of 11.3%.

We are ignoring IRB InvIT, as their Surat Dahisar project is going out of the concession period in FY23. This asset contributes around 32% of Total income & 34% of EBITDA.

The InvIT looks interesting with strong parentage & healthy financials. We should not be enthused with the current yield of 11.3% as the cash flows are going to fall from 2024. However, this will be compensated by the acquisition of new assets by the company, and the relatively low interest rates that it is likely to raise debt at.

We recommend a subscribe for the IPO & a Hold for the long term.

This article is for informational purposes. Investors should consider their specific asset allocation requirements to decide whether this is the right investment for them.

For access to Capitalmind Analysis, Model Portfolios, and the incredible Capitalmind Members’ slack forum, subscribe to Capitalmind Premium.

Join the best platform for active investors in India.