[This is a Premium article, unlocked for unrestricted access]

Kalyan Jewellers has come up with its IPO of Rs 1,175 Cr on March 16th. The offer is a mixture of OFS and a fresh issue. Proceeds from the issue will be primarily used to meet working capital requirements.

Kalyan has a market share of 5.9% and 1.8% of the organized and overall Indian jewellery market. Key developments in the jewellery industry over the past few years open up opportunities for players in the organized market. Kalyan is well placed to capitalise on these tailwinds through its “My Kalyan” network.

What are these tailwinds? How does the “My Kalyan” network help the company? We reviewed the Kalyan Jewellers IPO to see if investors should consider subscribing.

The Offer

Link to Kalyan Jewellers RHP

Issue size – 1175 Cr off which

- Fresh Issue – 800 Cr

- Offer for sale – 375 Cr – 125 Cr by promoters and 250 Cr by Highdell

Price band – 86-87/share

Offer for retail – 35% of the issue

Outstanding shares prior to the offer – 93,80,99,035

Market lot – 172 shares/ Rs 14,964

Dates – 16th March – 18th March

Objects of the Issue

The fresh issue will be used for meeting working capital requirements to the tune of Rs 600 Cr. The working capital requirement and utilisation of funds is shown below

Source: Kalyan Jewellers RHP

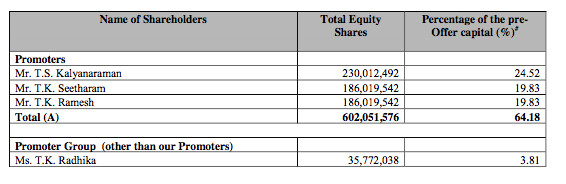

Promoter Holding

Promoters hold 67.99% of the company, below is the promoter shareholding as on the date of the RHP.

Source: Kalyan Jewellers RHP

Highdell is a investor shareholder, they own 30,02,75,421 shares or 32% of the equity share capital.

On March 4th 2021, 11,90,47,619 CCPS held by Highdell were converted to 9,88,57,435 equity shares at Rs 50.58/share.

Source: Kalyan Jewellers RHP

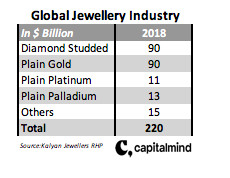

Jewellery Industry

The global jewellery market was $ 220 billion in 2018. The market consists of several types of jewellery, the break up of the market by types of jewellery is shown below

China, India and USA are the top jewellery markets in the world. In terms of demand India is the second largest market with 24% market share, followed by the China with a 31% share.

Indian Jewellery Industry

The Indian jewellery retail market was $ 64 billion in FY20. 32% of the market is organized, while 68% is with the unorganized players. The unorganized market comprises of over 5,00,000 local jewellers and goldsmiths.

The unorganized market in 2000 was 95%. Up until 2000, the market was catered by local/family jewellers. The offerings were restricted to local designs and there was no transparency on pricing and purity. It was in the year 2000, with the launch of Tanishq by Titan that organized retail in the jewellery market started picking up. Factors like trust and transparency, certificates of authenticity, product quality and buy back schemes tilted in favour of the organized players.

Off late demonetisation, GST, mandatory PAN card disclosure over purchases of Rs 2,00,000 have helped the organized market. Compulsory hallmarking, which will be effective in 2021 will increase costs and process requirements for unorganized players, this should further benefit the organized market.

The organized market can be classified into 4 types, the description of each is shown below

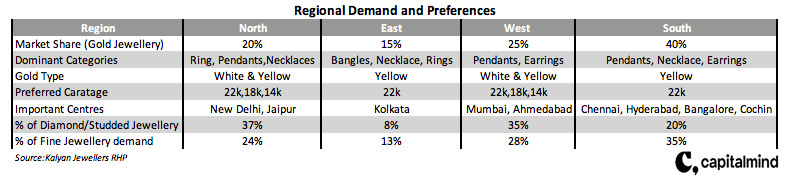

Demand by region and usage

The demand for gold jewellery is mainly from southern states, these states make up 40% of the Indian gold jewellery market. In the southern states consumers prefer traditional plain gold jewellery, margins for these products are lower. Consumers in the north and west prefer studded and light weight jewellery. Plain gold jewellery has gross margins of 10-14%, while diamond studded jewellery enjoys GPMs of 30-35%.

Demand for gold jewellery and preferences of customers across regions is shown below

India’s gold demand in 2019 was 690 tonnes, 79% or 544 tonnes was towards jewellery demand and the rest 23% was investment lead demand. The Indian jewellery demand is highly skewed towards gold jewellery. The diamond jewellery market is 13% of the total jewellery market by value.

In terms of usage, 60% of the jewellery demand is for weddings, 30% for daily wear and 10% for fine jewellery – light weight gold, silver and studded jewellery.

Gold carries a strong cultural affinity for Indians. It is widely used for consumption (jewellery) and investments (bars/coins). Marriages alone lead to 300-350 tonne of gold demand, many people in India start purchasing gold well in advance for future weddings. People purchase gold jewellery, coins, bars during festivals and auspicious occasions like Akshaya Tritiya.

Rural appetite for gold jewellery is more pronounced than urban India. Rural India accounts for 60% of gold jewellery demand in the country, its share in retail expenditure is 50%. Farm incomes, output and commodity prices have a strong relation to gold and jewellery demand.

Jewellery business in India is seasonal in nature. Jewellery demand peaks up in run up to the marriage months in May-June, September – January. Monsoons and agricultural output impacts demand in rural areas. Demands rises during occasions like Diwali and Akshaya Tritiya.

Value Chain for Organized Jewellers

- Gold is imported by nominated banks and agencies and diamonds are imported by traders

- Jewellers procure their gold from banks, customers and use recycled gold. In the case of organized and large jewellers, they directly procure their diamonds/precious stones from global suppliers

- Jewellers use the metal gold loan facility for procuring some of the gold used to manufacture jewellery. We will see how the metal gold loan facility works later in the post. Hedging instruments like forwards and futures are used to hedge their gold inventory

- Gold jewellery manufacturing is outsourced to contractors, the jewellers provide raw materials to these contractors and monitor the manufacturing process as quality of the final product is very important. In the case of studded jewellery, manufacturing is in house

Competition

Larger part of the jewellery industry is unorganized, as a result there are a lot of local and regional players in this business.

Thangamayil and Khazana are prominent players in South India. PC Chandra in the East and PN Gadgil in the West. There are few multi regional players like TBZ, Malabar, Joyalukkas, PC Jeweller and Senco, these players are focussed on one region but have started venturing to other regions in a small way.

Tanishq and Kalyan are pan India players. Tanishq (Titan Company) is the leader in the Indian jewellery market with 3.9% share of the overall market and 12.5% of the organized market. Kalyan on the other hand has 1.8% of the overall and 5.9% of the organized market.

Sales of jewellery from the E Commerce channel is $1.3 billion, 2% of the total market. The E Commerce channel can be driver in the future, although customers would want to physically see and purchase their jewellery. The E Commerce channel can drive sales for low value jewellery.

Interesting facts

Here are couple of interesting facts about usage of jewellery across parts of the country, this highlights the consumption patterns across these regions

- Gross weight of gold worn by a bride in Kerala is more than 2X the weight of gold worn by a bride in Gujarat

- Gross weight of wedding jewellery purchase is 200 Gms in Uttar Pradesh, while it is 350 Gms in Kerala

The Company: Kalyan Jewellers

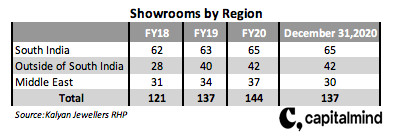

Kalyan jewellers was started by Mr. T.S Kalyanaraman in 1993. It set up its first showroom in Thrissur, Kerala. It currently has 107 showrooms spread across 21 states and union territories in the country. It also has 30 stores in the Middle East. All of the stores are operated and managed by the company.

In the Middle East, laws provide that local nationals should hold a certain percentage of shares of companies incorporated in those countries. The shareholding requirements in the GCC countries are shown below

Source: Kalyan Jewellers RHP

Although the local national has to own 51% in majority of the countries, Kalyan jewellers has entered into shareholder arrangements with local shareholders which provides management control and majority of the profits in the entity. The local nationals are entitled to an annual fee for acting as nominees.

Network

The 107 showrooms located in India cover a total aggregate area of 4,65,235 sq ft, translating into 4,348 sq ft per store. Kalyan has 32 staff per store in India. The 30 showrooms in the Middle East cover a total aggregate area of 38,056 sq ft, translating into 1,269 sq ft per store.

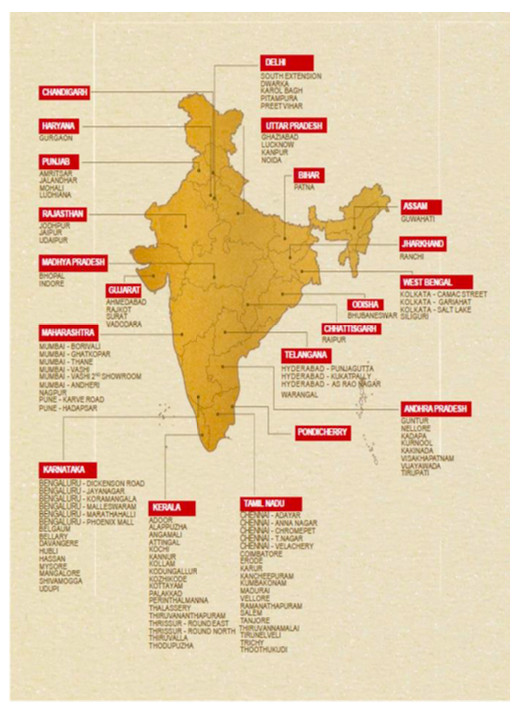

Network of Kalyan is spread through out the country with focus on the south as can be seen from the below image

Source: DRHP, Kalyan Jewellers

USP

Kalyan’s USP is its hyper local strategy that it follows to conduct its business.

What is the hyper local strategy and how does it help the company?

Customer tastes and preferences are different across regions. Jewellers have to offer products that meet the local tastes and preferences. For instance the company hires local artisans as contract manufactures to manufacture jewellery meeting local tastes, hiring brand ambassadors with national, regional and local appeal, hiring employees who speak the local language and who understand the culture of that region.

The company has a “My Kalyan” network to help in its hyper local strategy.

My Kalyan is a customer outreach network consisting of smaller centres that are located around the companies showrooms. As of December,2020 the company had 766 “My Kalyan” centres and 2,699 dedicated “My Kalyan” employees.

The functions of the “My Kalyan” network are

- Undertake door to door campaign and other marketing initiatives with local communities to promote the brand, showcase product catalogue, enroll customers in purchase advance schemes and help drive traffic to showrooms. No sales happen from these centres

- The employees in these centres build relationships with astrologers, caterers, event managers, make up artists, marriage halls and other vendors to identify jewellery customers

The network contributed 17% of domestic revenues and 31% of enrolment into its purchase advance scheme in FY20.

The key to running a jewellery business is inventory management and mitigation of gold price fluctuations. Majority of the cost in setting up a jewellery business is inventories.

The company procures gold from banks in India and the Middle East, it also sources gold from customers directly. Part of the gold sourced from the bank is bought and part of it is procured through gold metal loans.

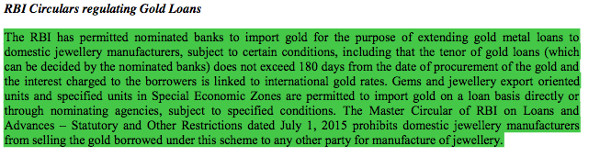

What are gold metal loans?

In the case of gold metal loans bullion is loaned to the company at specified interest rates. The company needs to post security along with margins for the gold loaned. Margin requirements have to be meet on a daily basis on the outstanding gold metal loans. When the company sells the gold procured through this model they fix the rate of purchase to align with the buying and selling rate of the underlying gold. Procuring gold through this method acts as a hedge.

Metal gold loans are regulated by Ministry of commerce and RBI regulations.

Source: RHP, Kalyan Jewellers

For gold purchased from the customer and banks, company enters into forward contracts. For FY20 and 9MFY21, 27% and 32% of revenue from operations included customer’s exchange or sale of their old jewellery.

In the case of managing inventory efficiently, the company has the network to move inventory from one store to another, so if a piece of jewellery is not selling in a particular store that can be moved to store where there is demand for that particular product. Inventory checks for sections of jewellery are done on a daily basis.

Jewellery design and manufacturing is an important aspect of this business. All designs are developed in house based on insights that the company gets from various sources – market research, data analytics and customer feedback. Manufacturing is carried out through a network of artisans spread across the country. These artisans work as contract manufacturers and have been associated with the company for long periods of time. Under the contract manufacturing agreements, the company controls the entire manufacturing process and the risk of raw materials and products lies with the company.

Other factors that have helped the company gain a stronghold in the market are

- Kalyan is one of the first companies to sell BIS hallmarked jewellery. BIS jewellery is expected to become mandatory in India in 2021. 40% of the jewellery sold in India today is hallmarked

- Detailed price tag on the ornaments – metal weight, stone weight, stone price and making charges. This brings in the much wanted transparency in the industry

- Offering Karatmeters in showrooms to verify the purity of gold jewellery sold by the company and procured by the customer from outside

- Wide range of product offerings under various sub brands

- Investments in Ennovate lifestyle which gives the company an online presence

At the end of December 31,2020 the company had 7,230 employees. 3,748 were employed in showrooms, 2,699 in My Kalyan centres, 108 in Ennovate lifestyle and 675 at corporate offices.

Financials

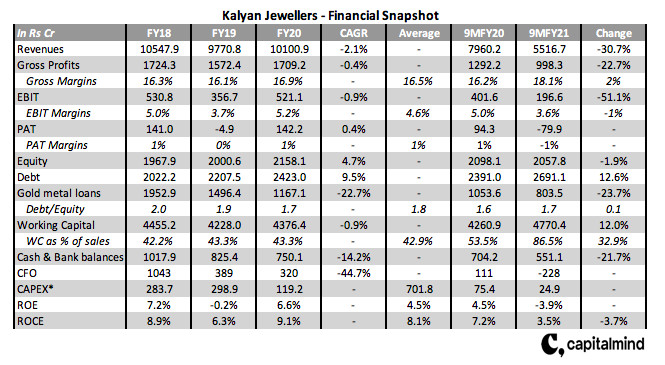

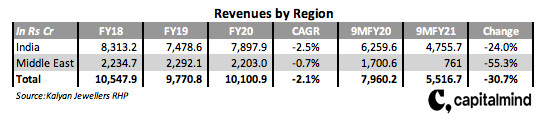

The pandemic has effected the company and that is visible from the revenues, these have fallen by 31% in 9MFY21. 80% of the revenues are from India and the rest from the Middle East. Below is the trend in revenues by region over the last 3 years

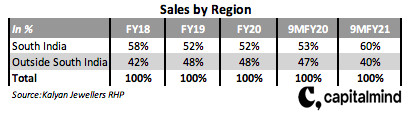

South India contributes to more than 50% of domestic revenues. However for 9MFY21, the split between revenues from South India and ROI is in ratio of 60:40.

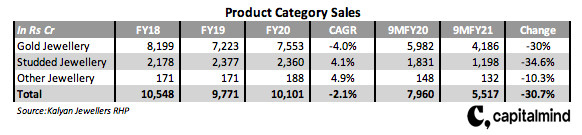

In terms of product category, the gold jewellery segment contributes 75% of revenues. Revenues from this segment have been in the range of 74-78% over the last 3 years.

Revenues from purchase advanced schemes was 27% of total revenues in FY20.

What is the purchase advances scheme?

Under this scheme customers make monthly payments over a period of 11 months to purchase jewellery within a period mentioned in the scheme (not exceeding 365 days from the commencement of scheme). Instalments paid by customers are not refundable in cash, these have to be used in the store to purchase jewellery. Revenues from these schemes are sticky in nature as the customer has to purchase jewellery from Kalyan stores. The company offers various purchase advance schemes such as “Kalyan Akshaya” “Kalyan Sowbhagya” and “Kalyan Dhanvarsha”.

The company has not faced any regulatory action in relation to collecting monies under this scheme, any regulation in the future can hamper the revenues of the company.

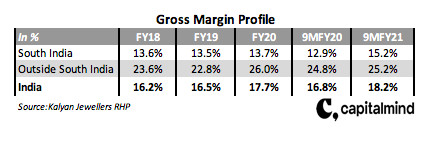

Kalyan’s gross margins over the past 3 years have been in the range of 16-18%. One of the primary reasons for these GPMs is due to the fact that majority of revenues come from the gold jewellery segment. Margins in the gold jewellery segment are lower than the studded jewellery segment. GPMs also differ by region, below is the trend in gross margins in South India versus the rest of India over the last 3 years.

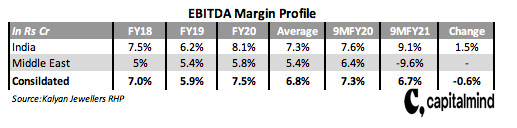

Operating margins in India are higher by 200 bps on an average as compared to the those in the Middle East. Below are the EBITDA margins over the last 3 years for India and the Middle East.

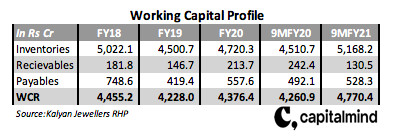

The business is working capital heavy, for every 1 Re of sales that the company generates it requires 0.43 or 43% in working capital to generate sales. Inventories constitute the major portion of working capital as can be seen from the below table.

The debt/equity has been greater than 1 in all of the last 3 years. The ROE and ROCEs are well below the cost of capital

Overall, there is a huge scope to improve the financial health of the company.

Our View

The good

Kalyan has a pan India presence and its “My Kalyan” network helps it deepening its presence in the market place and venture into newer markets.

Key trends like – GST, KYC compliance and hallmarking will help organized players like Kalyan. 68% of the market is still with the unorganized players. The transition from unorganized to organized may take time, however there exists an opportunity for players like Kalyan when the shift happens.

The not so good

The pandemic has effected this industry and it is visible from the 9M revenue numbers, which have fallen by 31%. Jewellery purchases are an essential part in Indian marriages and people also look at gold as an investment. However during tough times which we have seen in the last 1 year, customers postpone purchases of non essential items. Alternate avenues for the same investment like SGB can also lead to people moving away from buying physical gold.

There is a lot of scope for improving financial metrics of the company – from all the three profitability margins to the ROE and ROCE’s.

What matters

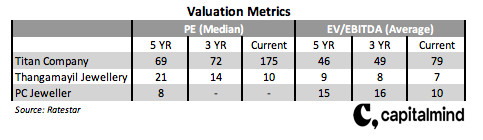

The FY20 EPS was Rs 1.49 and at the issue price of Rs 87/share, the company trades at 58X earnings.

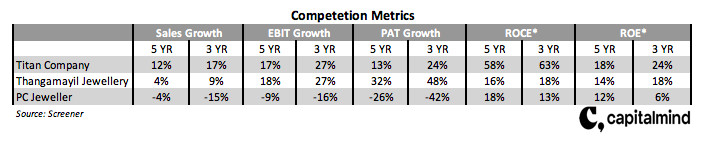

Let us look key metrics of other listed jewellery companies. We look at Titan, Thangamayil and PC Jeweller

For Titan the sales, EBIT and ROCE’s are for the jewellery vertical, the PAT and ROE’s are for the entire business. ROCE and ROE’s for all the companies are averages.

Titan and Thangamayil have had healthy sales, operating and PAT growth over the last 5 and 3 years. In comparison, Kalyan’s sales and profit growth over the last 2 years has been -2% and 0.4%. ROE’S and ROCE’s of Kalyan are also way below Titan and Thangamayil.

Looking at the current environment, current financials and the valuations at which the company is issuing its shares, we would give this issue a pass.

Other recent IPO’s we reviewed

For access to probably the best platform in India for active investors, join Capitalmind Premium. Model Portfolios, Premium Research, and a vibrant member community.