The Budget for FY 2022 is here, and it’s incredible in one thing: Not too many higher taxes. We thought there would be a corona cess, and there wasn’t. An increase in personal tax rates, and there wasn’t. In that context, the budget’s more about what it did not do, rather than what it did. So, here’s the a summary of top 10 things in the budget (with annexures).

The Top 10 Things in Budget 2021 that matter

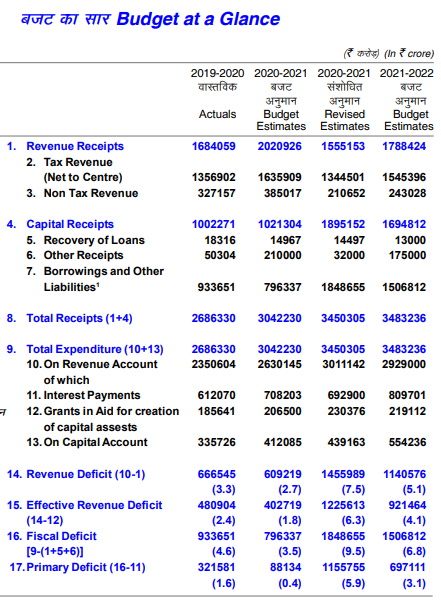

1. The government continues to spend.

34 lakh crores to be spent in the next year, about the same as this year. They expect to collect much lower tax+non-tax revenue compared to the previous year (about 17.9 lakh crore) The deficit was a massive 9.5% this year, and will still be about 6.8% for next year. This is actually fairly decent – they expect lower tax revenues, will spend about the same, and the deficit at 15 lakh crore will be a reasonable percentage of GDP given it’s a post Covid year.

2. Borrowing 12 lakh crores: Bond Markets Aren’t Liking It

The gross borrowing for the next year is 12 lakh crores. This is a very large amount, but it’s overshadowed by one thing: this year. The current year’s borrowing is already substantially more.

There’s going to be a net additional borrowing (net of repayments) of over Rs. 9 lakh crores. This is a ludicrously large sum, and the government will find it difficult to finance it unless the RBI steps in. And we do expect the RBI to step in strongly in the next year.

Bond markets didn’t like it much. Yields rose from 5.9% to 6.05% which means bond funds would have lose money – anywhere from 1% on longer term bonds to 0.2% in shorter term funds.

However, this is not that bad. Because:

- Part of the higher “spend” is because the government used to not pay the full subsidy for food. This has now been changed.

- FCI now gets money from the government and a whopping 200,000 cr. now gets paid from the government to the FCI (rather than a loan from NSSF)

- The fiscal math may slightly change but it’s more transparent this way. This difference results in a hit of 1% of GDP, so technically we would have been lower in terms of actual deficit.

The end-result: They haven’t increased taxes. They will increase spending. This is good for the economy.

Positive for: Infrastructure players which is where the government spends.

3. The Income tax department will pre-fill your capital gains data into your tax returns.

Note that because of the fact that the income tax department usually doesn’t get anything right, this will only hurt your tax return process. But in the next decade when they start to get it right, this will be a big boon. Just stay alive till then and you’ll enjoy it, eventually.

4. There is a Bad Bank Plan

The governmnt has said they will create an Asset Restructuring Company (ARC) and an Asset Management Company (AMC) to hold the bad loans of the banks so that the burden of bad loans is reduced. This will then sell these bad loans to an Alternative Investment Fund (AIF) that will buy those loans.

This has given huge enthu to the banking sector. But the details aren’t yet clear. Who creates the AIF? It’s quite likely the AIF will need private investment (from banks and foreign investors) who can then buy these loans and clear them over time. What are bad loans? Only those that were bad already? Can new loans becoming bad also qualify?

Will banks use this as an excuse to dump bad loans forever? And let taxpayers take the hit? The answer should be no, because this will be gamed and abused. We have to see how such a bad bank will work. Since this is not an actual bank, it may be structured as an AIF which can be privately funded. RBI will get involved in how the dispensation will work, but hopefully the loans are purchased by a private entity and not through a government funded effort.

Secondly, they will also create a fund that will buy bonds of “stressed investment grade” companies. This is actually not great. If it’s really stressed, it won’t be investment grade, but rating agencies can be arm-twisted into anything. However, this means that a fund set up by the government can buy these “stressed” bonds. It would make more sense to set this up as a pass-through mutual fund with minimum Rs. 50 lakh per investor as an investment, in order to allow HNIs to fund the purchase of highly stressed securities. Such a fund can also be bought by banks, private investors and foreign investors. We’ll have to wait and see how this comes about.

Positive for: Banks and NBFCs.

5. Reducing tax pains

- They can send you an income tax notice only within four years (used to be seven years) of the end of the financial year. After that, no. Unless they think you have concealed more than 50 lakh in income. In which case the limit is 11 years.

- New dispute resolution panels, “faceless” Appeal tribunals and ending of assessment within 9 months (meaning: within 21 months after the end of the financial year).

- No advance tax for dividends if they are declared after the corresponding advance tax dates.

6. Silver and Gold Get Cheaper, Despite /r/WallStreetBets Perhaps

Gold imports have been rising despite high duties on the shiny metal. The duty has been 12.5%. This has now been reduced to 10%. (Actually to 7.5% and there’s now a 2.5% cess of sorts)

This is a good thing. Gold prices will come down and the duty does nothing to deter people from importing. All it does is increase the smuggling of it. I had proposed this anyhow, a slow reduction of duties in our post on this: Let Us Cut Gold Imports This Way

7. Voluntary Vehicle Scrapping Policy

If your car or bike is more than 20 years old, or a commercial vehicle is more than 15 years old, it’s possible that the government may allow you to get a credit to scrap your vehicle.

Details will come soon, but the credit may allow you to buy a new vehicle in a cheaper way, if the current one is turning into scrap. This should help auto manufacturers, and also help create more steel scrap in India.

Positive for: Auto players.

8. Big Disinvestment

Even though the market is at sky high levels, the government has not been able to sell its stake in its companies for much. This next year, there will be:

- Disinvestment of LIC

- Selling off of BPCL, Air India, Shipping Corp, ConCor etc.

- Two more public sector banks to be privatized

- Another general insurance company to be privatized

This is all good to hear, but let’s not get ahead of ourselves. Talk is cheap.

One good thing is that they expect only Rs. 175,000 cr. out of this exercise. That much should be there from just two or three of the above (LIC + BPCL for example). So the target in terms of amount may be easier to meet.

Positive for: Media companies, because so much noise and so little actual progress.

9. A 0.1% Tax Deducted at Source If Big Businesses Purchase Goods

In what is a big pain for companies selling goods, a 0.1% TDS has been introduced for buying “goods” worth Rs. 50 lakh or more. This applies to companies (or LLPs or even proprietary businesses) who have a turnover of Rs. 10 cr. or more.

This is a tiny TDS, but it means that businesses buying goods online now have to deal with this TDS thing differently. This will however not apply to:

- Services

- Goods on which they have to collect TDS or TCS anyhow (such as car sales of more than 10 lakh rupees)

- HNIs who don’t have business income of Rs. 10 cr. (even if total income is more than 10 cr)

This is a boring little provision but can hurt a lot of businesses that do a lot of trading, including ecommerce buyers. All public trading companies that buy from “residents” will pay this tax at source. It’s a pain for cash flow, but won’t hurt profits that much. However, it should curb some situations where a very high payment is perhaps made, back and forth, to avail GST offsets and thus abuse the tax code.

There’s no benefit to this other than hurting the good companies. The bad ones will find another way out.

10. Other points

- ULIPs, at least the high premium types, will be taxed when you exit. We have more details in this post.

- EPF: Higher contributions will see interest taxed. Limit: Rs. 2.5 lakh per year. More in this post.

- Big push to fishing as five ports will be set up for fisheries

- Customs duties increased: Steel duties have been reduced, even as the ministers complain there is too much cartelization of steel. Long and flat steel imports see a cut in both regular duties and anti-dumping duties.

- Duty hiked for Carbon Black. Companies like Balkrishna who have their own Carbon Black plants will benefit. As will Philips Carbon Black which makes the substance.

- PCB, Cameras, Compressors, Parts of Lithium batteries, and even Solar lanterns and inverters see a big duty increase. This is the standard process of adding duties on anything we import, but is in general bad because it’s taxing the raw material, not the finished good.

- Even though they cut retail fuel taxes, the government introduced an Agriculture Infrastructure and Development Cess on petrol and diesel of Rs 2.5 and Rs 4 respectively. However, this will not increase the retail fuel prices as this Cess will be adjusted against the existing taxes being charged by the government.

What they didn’t do

- Did not increase cigarette tax (Positive for ITC, one such budget)

- Did not increase income tax (positive for everyone)

- No Covid Cess

- Did not try to limit expenditure in a hurting economy

- Did not give free money to everyone

- Did not have too many poems (a minor relief for us listeners)

Overall, very reasonable budget. Markets are up big time, and perhaps quite linked with world markets as well. Good start to a February.

Our Massive Budget 2021 Tweet Thread

Click the tweet below to start:

The Big Massive Thread on #Budget2021 – our take at @capitalmind_in pic.twitter.com/KmmDvFtFtW

— Deepak Shenoy (@deepakshenoy) February 1, 2021

Also, you can read the whole thing as an article .