[This is a Premium Unlocked article]

Burger King opens for subscription on 2nd December,2020. In this post we look at the the IPO and the food services business in India.

Burger King has been a late entrant in India, it set up its first restaurant in 2014. It has been aggressive in setting up outlets across the country having 249 operational outlets currently. Revenue growth has been impressive at 54% CAGR over the past 3 years, however it hasn’t been profitable. It has had to resort to debt and equity dilution to fund its expansion.

COVID has impacted the business as seen from the latest numbers ending September,2020. Given the current environment it wouldn’t be a bad idea to see the business stabilise after it lists and then take positions.

The Offer

Link to Burger King RHP

Issue Size – 135,000,000 shares, Off which

Fresh Issue – 75,000,000 (450 Cr at Rs 60/share)

Offer for sale (OFS) – 60,000,000

Price Band: Rs 59 to 60/share

Offer Value: Rs 810 Cr

Offer for Retail: 10% of the Issue

Outstanding shares post the IPO: 381,654,605 shares

Market Lot: 250 Shares/ Rs 15,000

Dates : 2nd December – 4th December

Prior to coming to the markets, the company has undertaken Pre IPO placement, details of which are as below

- Rights issue of 1,32,00,000 to promoters on 23rd May 2020 at Rs 44/share amounting to Rs 58 Cr

- Preferential allotment of 1,57,12,820 to Amansa Investments Limited in November,2020 at Rs 58.50/share amounting to Rs 91.91 Cr

Earlier in the year 1 Cr of CCPS (compulsorily convertible preference shares) were converted to 1,11,11,111 equity shares at price of 90/share to QSR Asia, the promoter.

The proceeds would be used to

- Repayment of outstanding borrowings obtained for setting up of new company owned restaurants and

- CAPEX for setting up new restaurants

- General corporate purposes

Breakup of the spending is as below

Food Services Market

The Indian food services market is classified into two segments – organized and unorganized. Key characteristics of “organized” outlets

- Accounting transparency

- Organized operations with quality control and sourcing norms and

- Outlet penetration

Outlets that do not meet the above criteria fall into the unorganized segment and include dhabas, roadside eateries, hawkers and street stalls.

The organized market can be further classified into

- Standalone outlets and

- Chains (domestic or international outlets that have more than 3 branches across the country)

Chains can be divided into six sub segments based on average price per person, service quality and speed and product offering

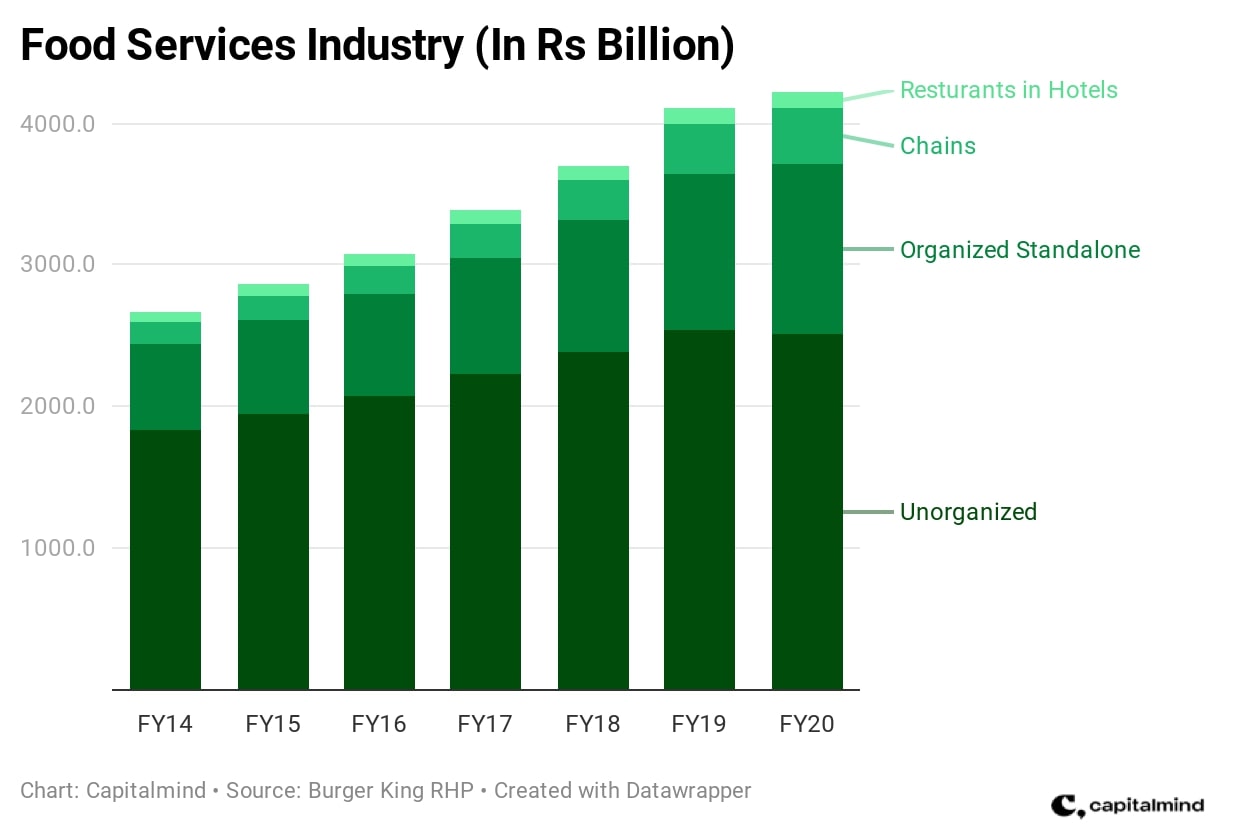

The food services market is estimated to be Rs 4,235 billion in FY20. Breakup of the market into various categories for the FY14-20 period is as below

Observations

- Total market has grown by 8% CAGR. Organized market has grown fastest – organized standalone at 12% and chains at 18%

- The unorganized market constitutes majority – 59% of the total market. However this is on a declining trend – 69% in FY14 versus 59% in FY20

- The organized market (Standalone + Chains) stood at Rs 1,600 billion. Both these have gained substantial market share over the 6 year period

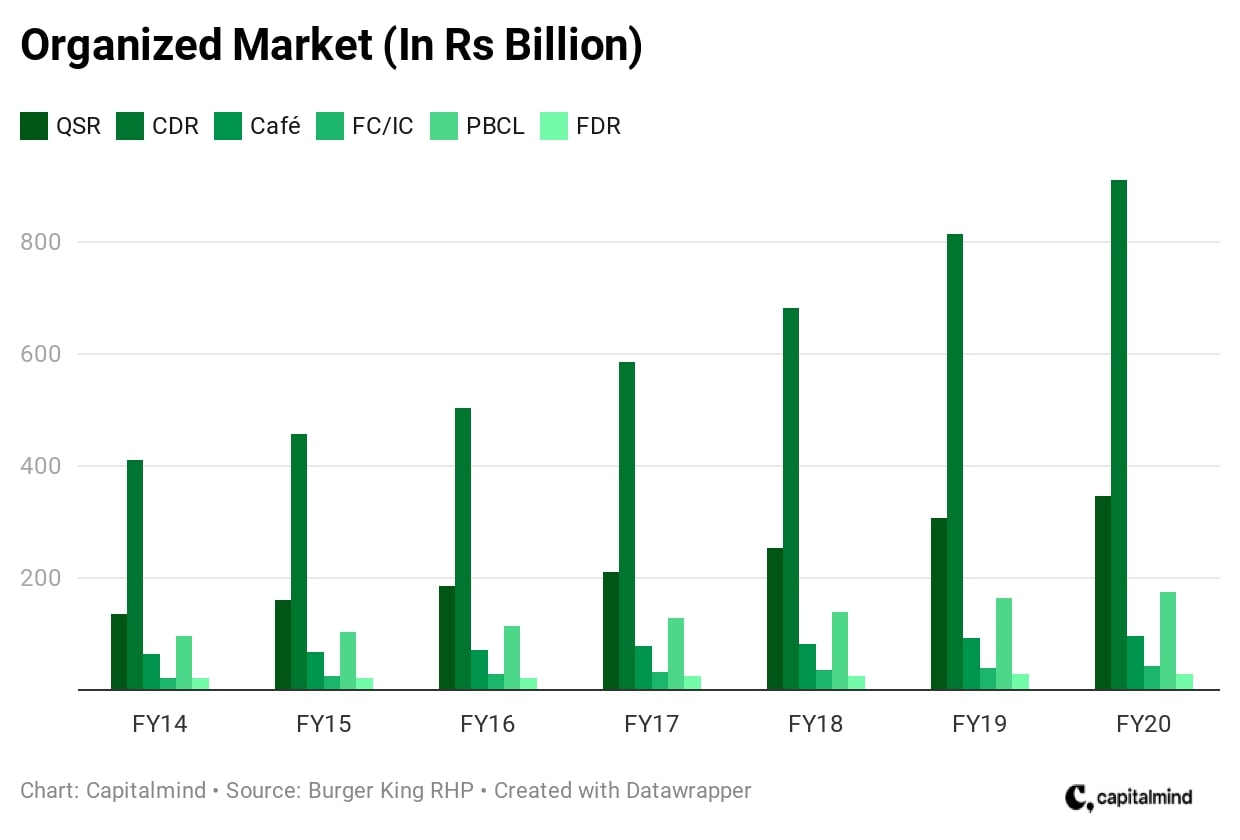

The organized market (standalone + chains), which was Rs 1,600 billion market can be broken down into the below segments

QSR: Quick Service Restaurant

CDR: Casual Dining

FDR: Fine Dining

FD/IC: Frozen Dessert & Ice Cream Outlets

PBCL: Pubs, Bars, Clubs, Lounges

Key takeaways from the above chart

- Total market has grown by 13% CAGR. The QSR and CDR segment have seen the fastest growth – 17% and 14% respectively

- Casual dining (CDR) constitutes 57% of the market followed by QSR which is 22%. Together these markets have 79% of the market

- Fine dining (FDR) has seen the lowest growth 3% in the above period

- QSR has seen the highest market share gains in this period at 4%

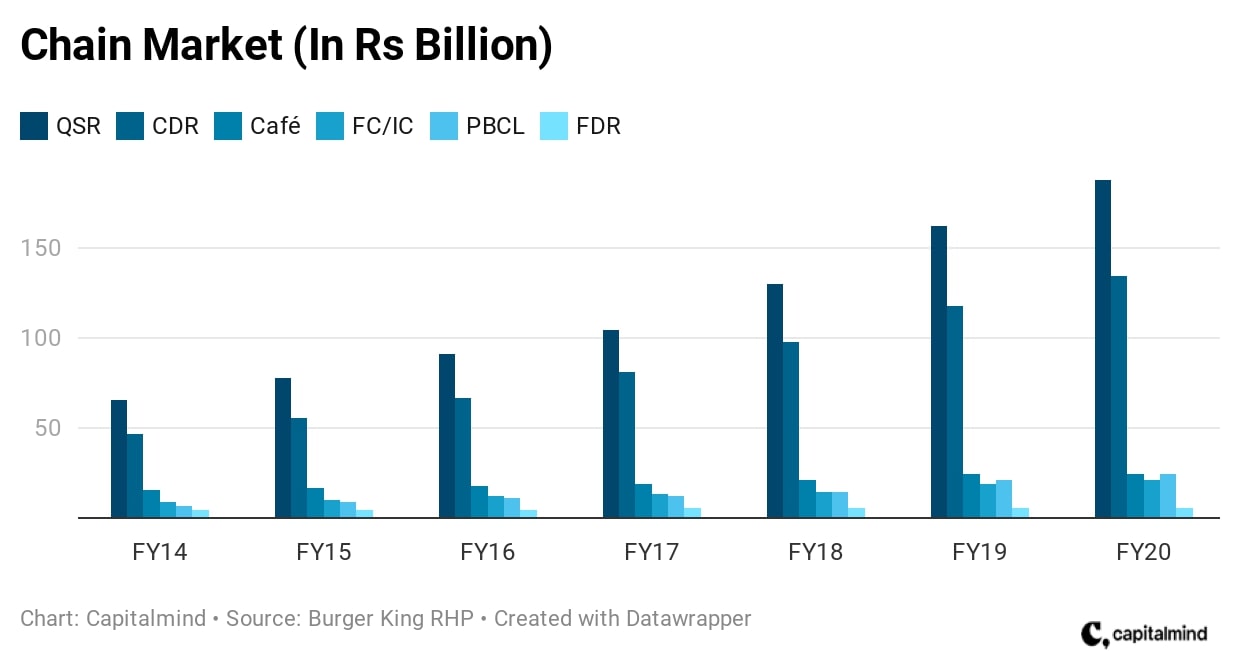

The chain market was Rs 398 billion in FY20, Burger King operates in this market under the QSR category. Trend and breakup of the market by various categories

Observations from the above data

- The market has grown by 18% CAGR. All segments except the Cafe and FDR segment have seen double digit growth

- QSR segment has 47% of the total market. QSR and CDR segment together hold 81% of the chain market

- QSR and CDR have registered growth of 19%, PBCL has seen the highest growth at 23%, though this is on a small base

- Highest market share gains of 3% and 4% have been clocked by the QSR and CDR segment

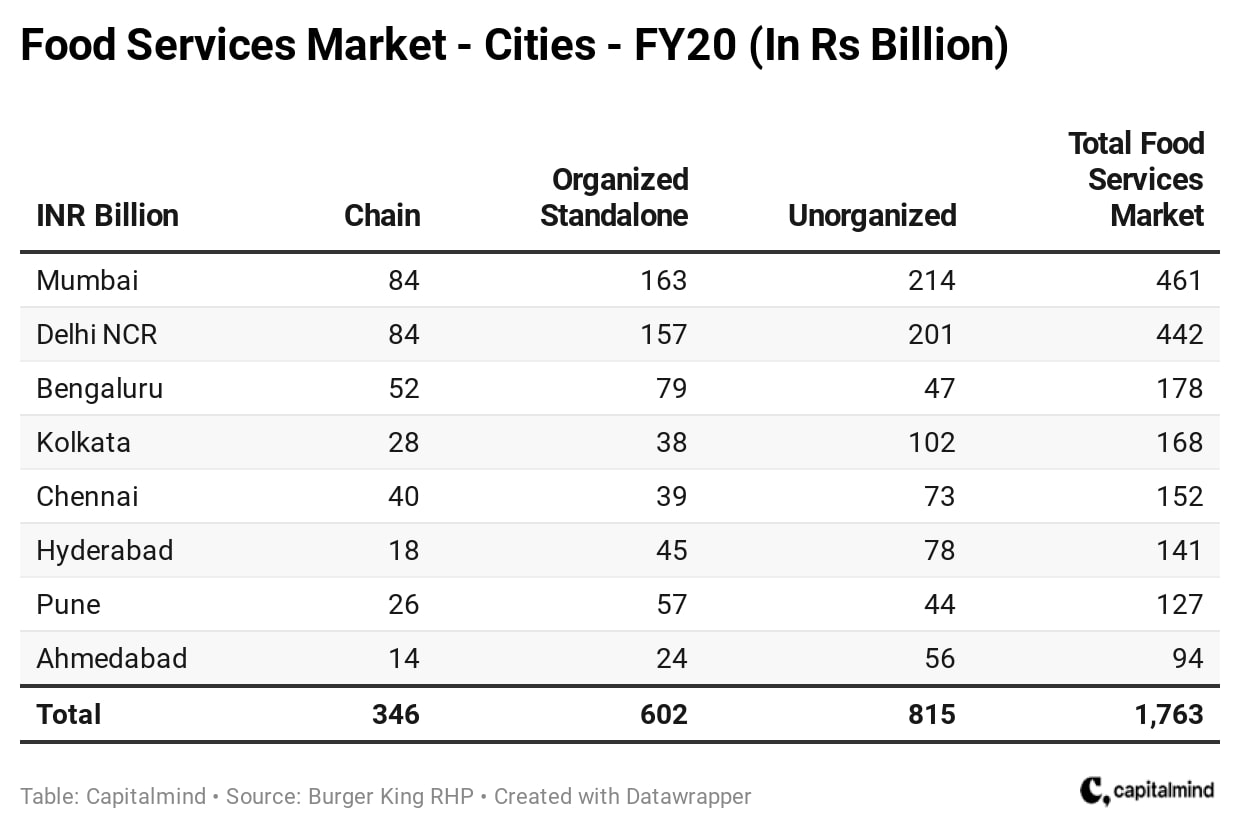

The top 8 cities constitute 42% of the food services market. Mumbai leads the chart with market size of Rs 461 billion, followed by Delhi NCR with a market of Rs 442 billion. The below table shows the market size of the 8 cities classified into chains, organized and unorganized markets for FY20.

Observations from the above table

- Ahmedabad and Kolkata’s unorganized market is +60% of their total food services market

- Bangalore and Pune’s chain and organized market is 71% and 63% of their food services market

- Split in organized and unorganized in the Mumbai and Delhi NCR is 50:50

The IPO Candidate: Burger King

Burger King was founded in 1954 in the United States and is owned by the Burger King Corporation, a subsidiary of restaurant brands international inc. Restaurant brands international holds portfolio of fast food brands around the world that include – Burger King, Popeyes and Tim Hortons. Burger King is the second largest fast food brand globally and has a global network of over 18,675 restaurants in more than 100 countries as on September,2020.

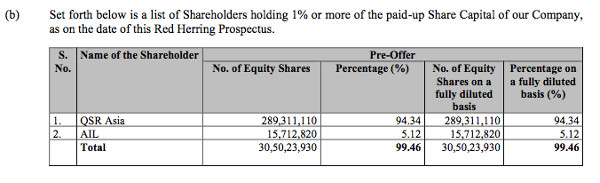

The promoter of Burger King India is QSR Asia Pte Ltd and owns 94.34% of the company. It has a master franchise and development agreement with Burger King Asia Pacific, which is an affiliate of Restaurant Brands International Inc.

Key features of the master franchise agreement are

- Exclusive right to develop, establish, operate and franchise Burger King restaurants in India

- Obligated to develop and open at least 700 restaurants by December 31,2026, 60% of these at any time should be company owned company operated

- One time non refundable fee upon opening of each restaurant, starting with $15,000 increasing to $25,000 from calendar year 2020 to 2022 and $35,000 thereafter. Renewal fee will have to be paid at the time of the renewal of the licence

- Monthly royalty on % of sales, royalty fee ranges from 2.5% to 5%, depending on the opening date of the restaurant

- Minimum contribution of 5% of sales for marketing and advertising

- Authority to establish local menu for restaurants and pricing for products, however these must be approved by BK Asia Pacific

- The master franchise and development agreement is valid until December 31, 2039

As on the date of the RHP, the company owes BK Asia Pacific outstanding monies with respect to royalty, franchise fees, travel expenses and subscription fees to the tune of $ 14,55,535. These will be paid in three instalments in Q4FY21.

The company operates in the QSR segment and was a late entrant in the Indian markets. It opened its first restaurant in November,2014. As on the date of the RHP the company has 268 restaurants across the country, 9 of these are sub franchised and the rest are company owned. 51% of the restaurants are in North, 25% in West, 21% in South and 3% in East India. Off the total restaurants 249 are operational as on the date of RHP.

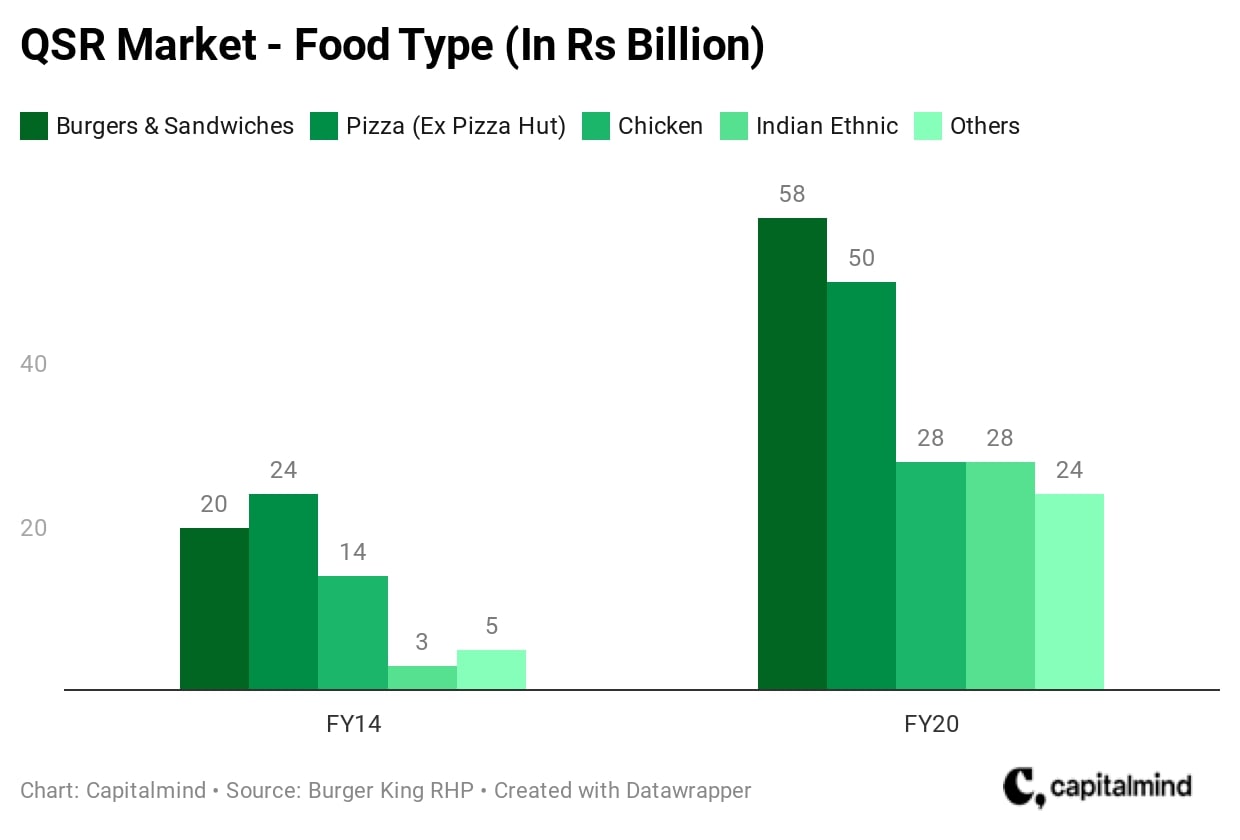

The company operates in the QSR segment and break up of the market by food type is shown below

Burgers & Sandwiches account for 31% of the market, followed by Pizza with 27%, however this does not account for Pizza Hut (which is classified as CDR and not QSR). Chicken and Indian ethnic had a market share of 15% each.

The chain market has shown impressive growth in the last 5 years – 18% CAGR. Some of the reasons for this are

- Increased eating out and ordering in behaviour – 60% of Indians eating out are millennials (15-34 age group), companies including Burger King target this market segment

- Increased internet and smartphone penetration

- Offering exclusively suiting the Indian palate – like the Mumbai Indian masala whopper offered by Burger King, wraps by Domino’s, KFC rice bowl

- Rise of platforms like Zomato and Swiggy – delivery market has increased from $4.7 billion in FY16 to $10.2 billion in FY20, projected to reach $18 billion by 2025

- Increase availability of retail space enabling expansion of food services outlets

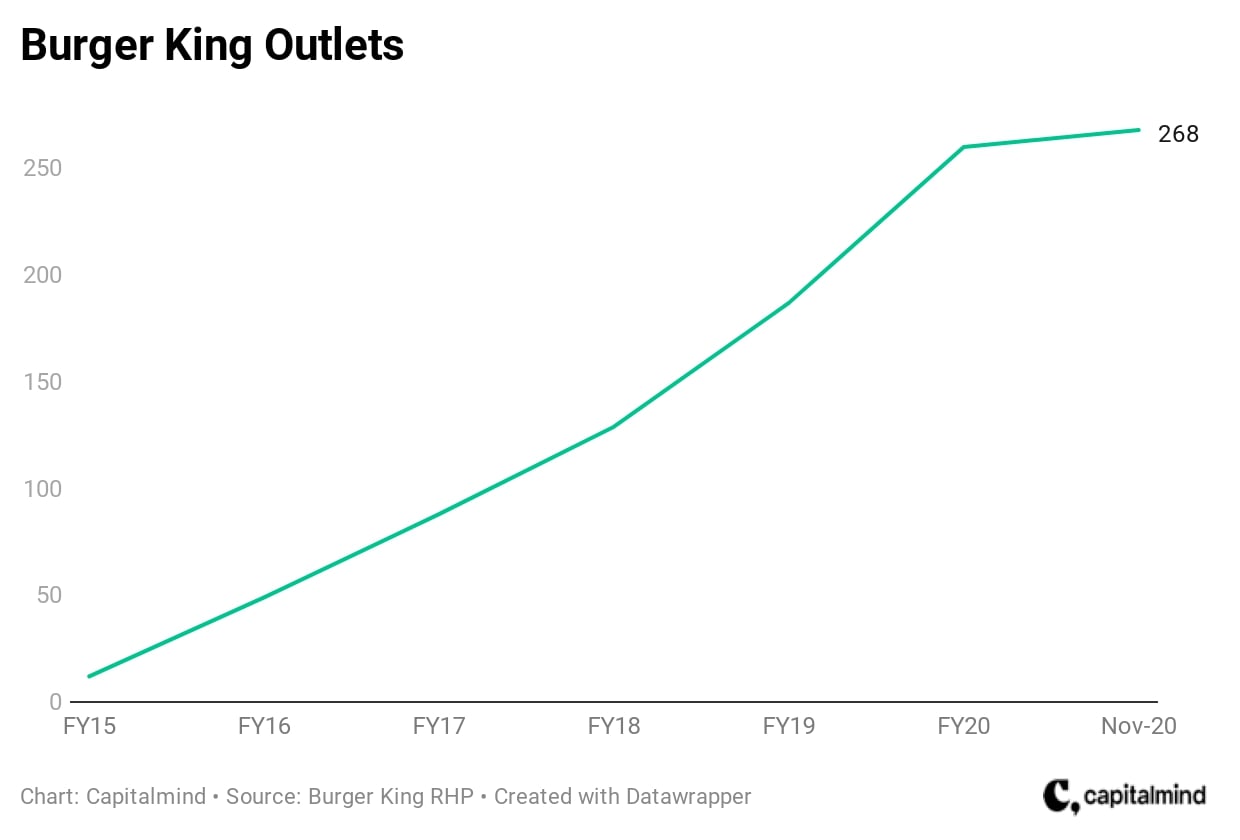

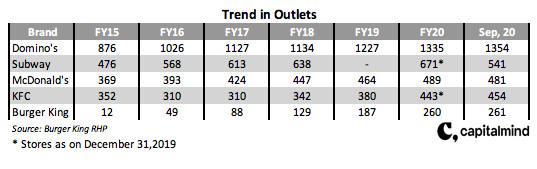

Although Burger King has been a late entrant in the Indian market, it has been the fastest-growing international QSR chain in the last 5 years. The below chart captures the growth in the number of outlets of Burger King from FY15.

Restaurants are spread across India as shown below

Source : Burger King DRHP

Restaurants vary across sizes from 400 square feet to 4,000 square feet. Standard restaurant template size ranges from 1,300 – 1,400 square feet.

The USP or the value proposition of Burger King is to provide quality products that suit the Indian palate and are not to heavy on the pocket as well. For instance, the company has a lot of products which are under Rs 100 and runs promotions like 2 crispy veg burgers for Rs 69. The company also has a wide variety of product offerings, it has a range of 22 different vegetarian and non-vegetarian burgers covering both value and premium segment. The incremental pricing between products is also kept low – 10-20 Rs, this enables the customer to upgrade easily.

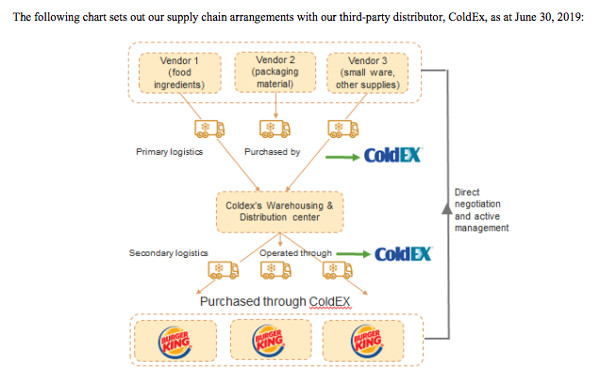

Some of the suppliers of the company include – Hyfun Foods, Mrs Bectors, OSI Vista, Pepsi Co, Schreiber, Veeba and Venky’s. Supply chain is an essential piece of the business, it is very important for the company to get its supplies on time and in the right condition. The company manages its supply chain through a third-party distributor – ColdEX. The third-party distributor buy supplies from the vendors and Burger King then buys it from ColdEX. This arrangement gives the company access to ColdEX’s warehousing facilities and extensive logistics network across the country. In addition, the company saves on investing in working capital, as the third party distributor keeps all the supplies on its books before the company purchases it.

Source : Burger King DRHP

Competition

The organized chain market has more than 100 brands with over 7,000 outlets spread across various cities in India. Competitors of the company are other international QSR chains such as McDonald’s, KFC, Domino’s Pizza, Subway, Pizza Hut and other local restaurants operating in the QSR segment.

Some of the important metrics with regards to the competition are shown below

Outlets of McDonald’s operated by South and West Franchisee

Observations from the above table

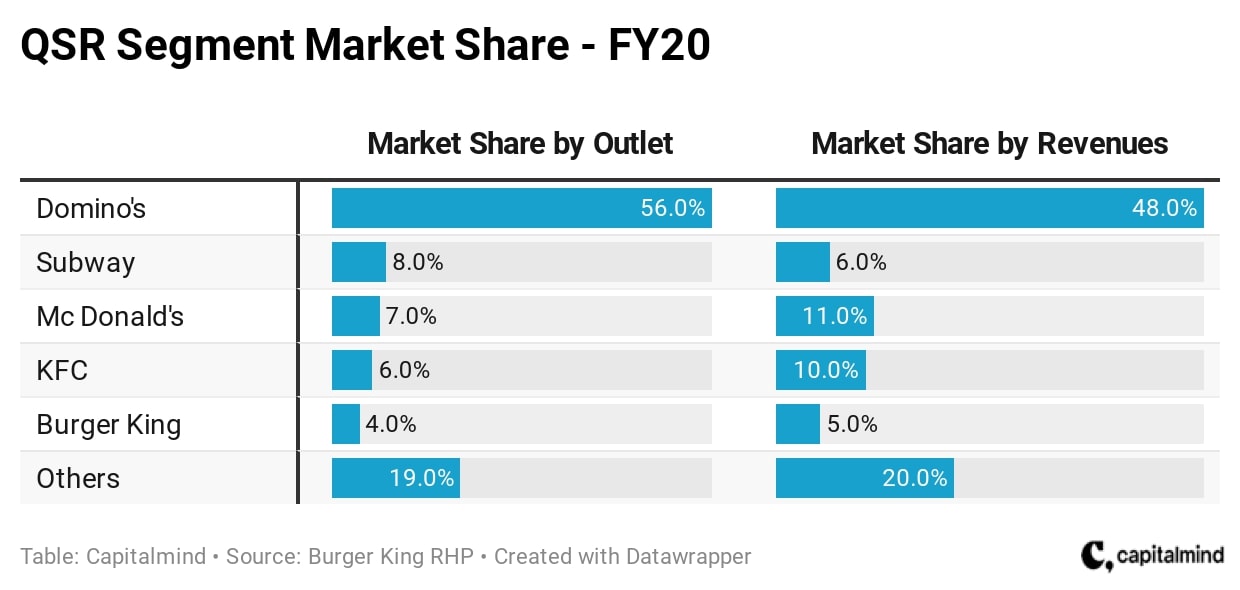

- Domino’s dominates the market in terms of no of outlets – 1,354 across the country

- The average price per customer (APC) is lowest for Subway, 175-200 Rs. Average size of Subway stores are the lowest 750-1000 square feet

- All companies enjoy high gross margins with Dominos leading the pack with margins of 77-78%

- Advertisement costs are in the range of 4-7% for all companies. Companies operating in this space have to constantly spend on advertisements

- All companies do pay royalty to the parent company. Royalties are in the range of 3-8%

- Burger King has the lowest store EBITDA margins at 12-14%

- CAPEX ranges from 1.5-5 Cr in setting up new outlets

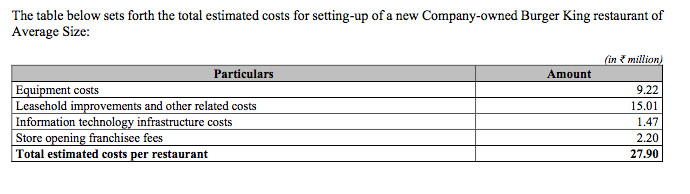

Average cost of setting up a Burger King restaurant of 1,300-1,400 square feet is Rs 2.79 Cr. Breakup of the costs are shown below

McDonald’s is the category leader in the Burger & Sandwich segment with 42% market share. In Pizzas in the chain QSR segment, Domino’s has a market share of 80%.

Market share of organized players on outlets and revenues at the end of FY20 is as below

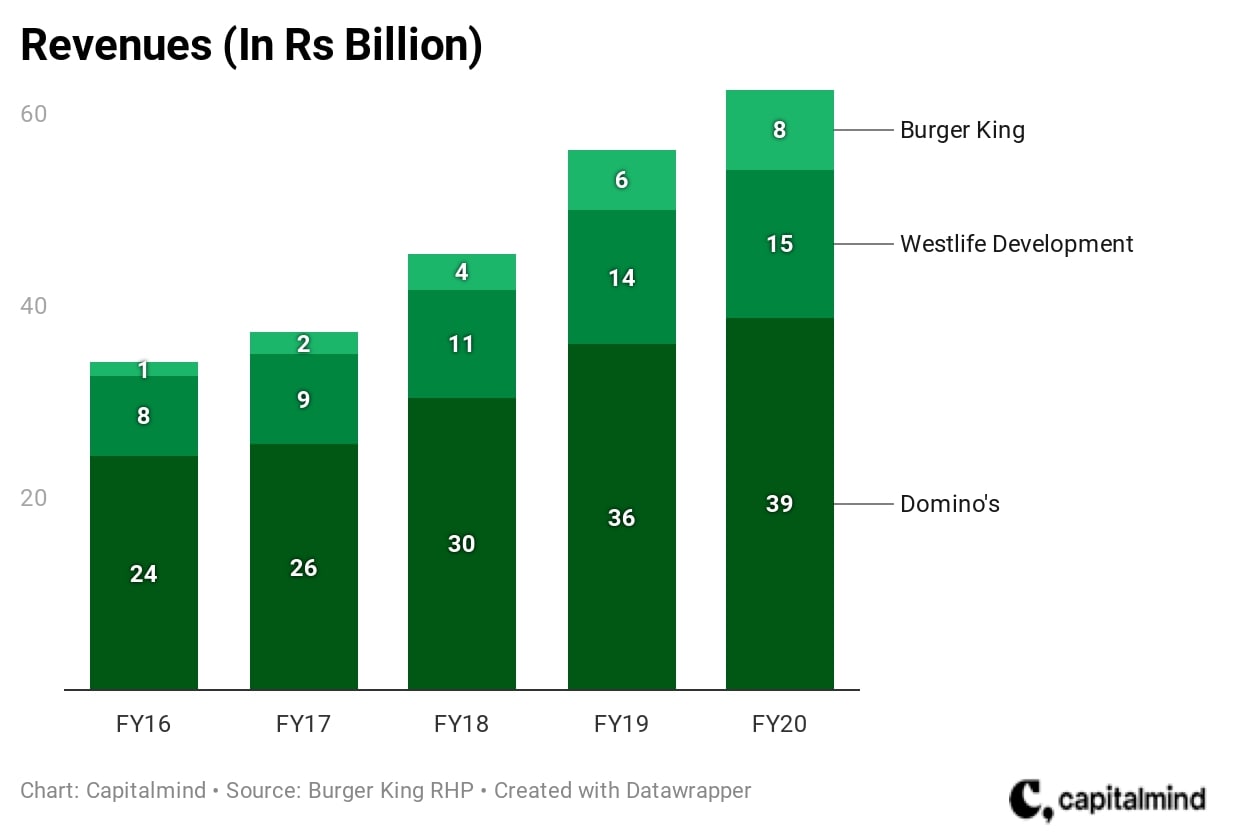

Below are the revenues of key international brands in INR Billion

Domino’s is the leader in terms of revenues, the company posted revenues of Rs 39 billion (3,900 Crores) in FY20. Westlife Development, which runs McDonald’s outlets in the south and west grew had revenues of Rs 15 billion, sales have compounded by 17%. Burger King’s sales for FY20 was Rs 8 billion, revenues have compounded by 57% in the FY16-20 period.

Below is the trend in number of outlets opened every year since 2015 among the various players in the industry.

Burger King has expanded its outlet base at 85% CAGR in the above period.

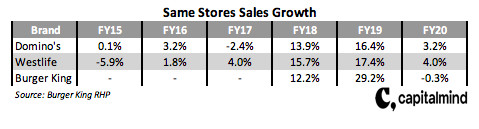

Same-store sales growth (SSSG) is an important metric in the food services business. It is growth in sales that the company registers from stores that have been open at least one year. The SSSG for key brands are shown below

The SSSG for Burger King in FY18, 19 and 20 was 12.2%, 29.2% and -0.3%.

Financials

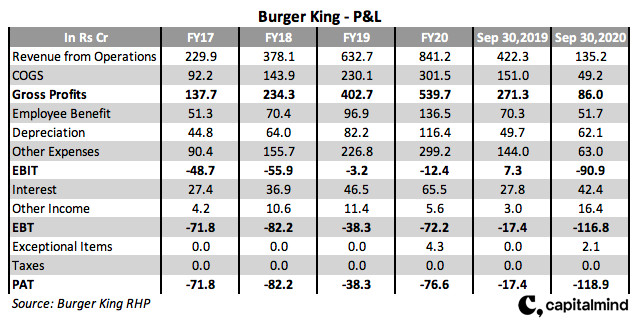

Revenues stood at Rs 841 Cr at the end of FY20. Revenues and gross profits have compounded by 54% and 58% in the 3 year period. GPM stood at 64% in FY20, margins have averaged at 62% in the 4 year period. The company has posted operating losses in every year since FY17, other expenses form a major portion of expenses and its major components are – advertising, power & fuel, commission and delivery expenses, royalty and rent.

Revenues have been hit for period ending September 30,2020 due to COVID 19. 55% of Burger King’s restaurants are in malls and these were the last to open. The company has seen pick up in its delivery business, however since more than half of its outlets are in malls, performance has been heavily impacted.

On the balance sheet, majority of the assets are PPE and right to use assets. The financial statements have been reinstated to account for the new accounting standard IND AS 116, which pertains to leases. Under IND AS 116 lessees have to recognize a lease liability reflecting future lease payments and right of use asset for almost all lease contracts. This is different from the earlier standard IND AS 17 where there was distinction between financial lease (on balance sheet) and operating lease (off-balance sheet).

Companies will have to recognize assets and liabilities for all leases with a term of more than 12 months unless the asset is of low value. As a result, depreciation is charged on the right to use assets and interest on the lease liability portion.

On the liability side, the majority is in the form to lease liabilities. Debt on the books as on September 30,2020 is to the tune of Rs 196 Cr, the debt/equity ratio is 0.90. Due to the losses incurred in all these years, there is a hit on the retained earnings, total equity (Share capital + retained earnings) stood at Rs 219 Cr at the end of September,2020 as compared to Rs 368 Cr in FY17. The company has a negative working capital, working capital at the end of September,2020 was – 111 Cr, this is because the inventories are in the books of ColdEX as mentioned earlier and there is no credit extended to customers for its products. On the other hand, the company does not pay its suppliers immediately.

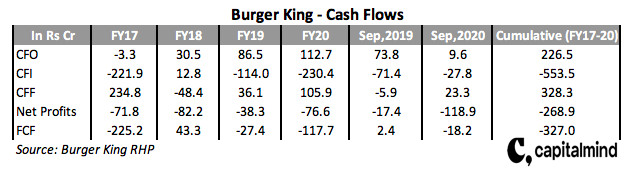

The cumulative cash flow from operations (CFO) are positive as compared to the cumulative net losses of -269 Cr. This is primary due to adding back of depreciation and interest costs to arrive at the CFO. Cash flows from investing have been Rs 554 Cr, as CFO haven’t been enough to meet this, the company has had to resort to borrowings and issuing equity to fill this gap. Cumulative cash flow from financing over this period was Rs 328 Cr.

Risks and Challenges

Some of the risks and challenges that the business faces are

- Food services market is fragmented in India, 62% of the market is with the unorganized players. In this kind of an environment it is a challenge to retain customer loyalty and companies have to constantly spend/carry out initiatives to gain footfalls

- There is shortage of skilled labour and attrition rates in the industry are 35-40%, the cost of manpower is also high. This can impact the quality of products that the restaurant offers

- Rentals are the 2nd highest cost component, the average rate is 12-15% of revenues and in some cases can go upto as high as 20%. This is a fixed cost and monthly payments have to be made irrespective of how the restaurant does

- There are lot of regulations and over licensing to start a food service business. It is estimated that players wanting to enter the food services market require 12-15 licenses from various authorities

- Awareness among the public for healthy food may hamper businesses of companies operating in this space offering pizza, burgers, sandwiches

- Cloud kitchens offering the same type of food will be more profitable than walk-in restaurants as there is no major CAPEX in setting this up versus a fully furnished restaurant

- Delivery aggregators may charge higher commissions to restaurants which will impact the profitability of the players operating in this space

COVID 19 has impacted the business, we do not know how the business model will evolve coming out of this pandemic. Ordering online and delivery through third party vendors like Swiggy and Zomato have gone through the roof. Whether this trend will continue and will there be a structural change to the business is to be seen. On the other hand, since the real estate market has been hit badly, the company can set up restaurants at a lower cost. Infact, the company has re negotiated its rents on its existing outlets.

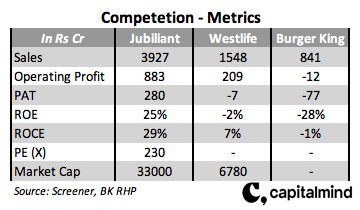

Peer Comparsion

There are two other listed players in this space – Jubliant Foodworks (Domino’s) and Westlife Development (McDonald’s).

Below is a table showing important metrics for listed players in comparison to Burger King for FY20

Drivers like higher incomes, people eating out more frequently and women joining the workforce will drive the demand for the offerings that companies make in this space. The price at which retail investors can participate in this story will be the decider.

Our Take

The IPO of Burger King is now ready. The price is Rs. 59-60 and the IPO is between December 2 and 4.

They will raise Rs. 450 cr. and sell another 6 cr. shares of the promoters. This effectively is a Rs. 810 cr. IPO which is relatively small. Since our initial writing of the post, Burger King had a rights issue, in which they gave their promoter 1.3 cr. shares at Rs. 44, and then sold 1.57 cr. shares to AIL at Rs. 58.5 per share.

The last three quarters too have seen miserable earnings, with a loss of 119 cr. in the 6 months ended Sep 2020. The company is valued at 1745 cr. pre-money at the IPO price of Rs. 60, and has about 200 cr. of debt . They will raise 450 cr. more into the company which should give them some breathing space and value it post-IPO around 2,200 cr.

Revenues were up another 30% and the company was operating cash flow positive to the tune of 110 cr. in FY20, so there’s a longer term operational turnaround visible. However, they continue to reinvest that cash into further growth.

Given the tiny size of the IPO, it may see a huge oversubscription. So it may be best to apply for one lot only, and let it list. Once it finds a price, and gives results in a few quarters, the Covid Impact will be done with and we can consider larger positions.

NOTE: This article is for informational purposes and should not be considered as specific advice. Our recommendations are part of the Premium portfolios and experimentals specifically called out as those. For full access to premium articles, model portfolios, and member forum, subscribe to Premium.