[This is a Premium Unlocked Post]

In this post we look at the domestic mutual fund industry and UTI’s business and its prospects.

What we look at

- Offer by UTI – Shares on offer and expected inflows

- How has the mutual fund industry evolved over the years?

- Domestic mutual fund industry – competitive intensity, who is the largest player in the market?

- Which asset class is prominent among retail and institutional investors

- UTI – its roots and history

- Business verticals of UTI AMC

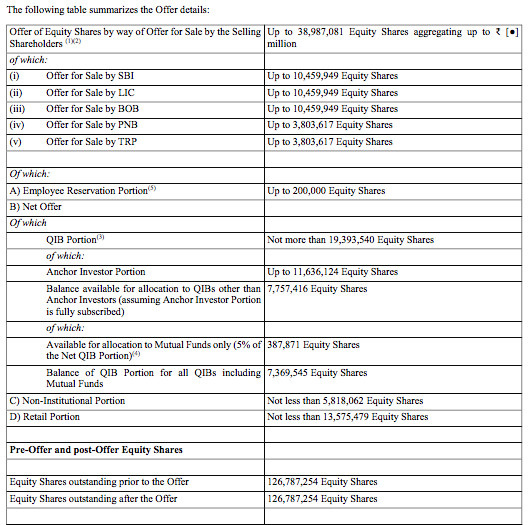

The Offer

Issue – Offer for sales (OFS) of 3,89,87,081 shares

Price Band – Rs 552-554/share

Offer value – Rs 2,160 Cr at the higher price band

Offer for retail – 35%

Equity post the issue – 12,67,87,254 shares

Offer dates – 29th September, 2020 – 1st October,2020

SBI, LIC and BOB will sell 1.04 Cr shares each and PNB and T Rowe Price 38 lakh shares.

Source: UTI AMC, DRHP

Industry

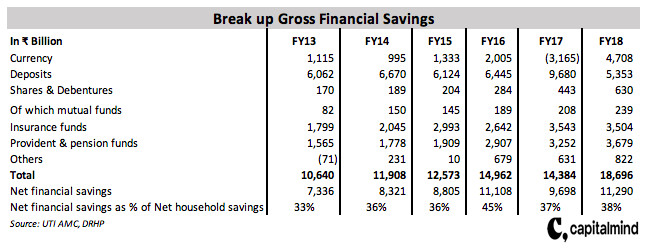

Household sector savings (net financial savings, savings in physical assets and in the form of gold and silver ornaments) stood at ₹ 29,382 Billion, 17.2% at the end of FY18. Gross financial savings were ₹ 18,696 Billion and the break up gross financial savings for the FY13-18 period is as below

Mutual fund are 1% of gross savings. The runway for mutual funds in the country is huge.

Mutual Fund Industry

The Indian mutual fund industry has history of over 50 years, starting with the formation of Unit Trust of India. UTI launched its first scheme, Unit Scheme 64 in 1964.

In 1987, public sector banks were allowed to enter the mutual fund space, SBI Mutual fund was set up in June, 1987 followed by the launch of of Canbank MF in 1987. Industry assets at the end of 1993 stood at Rs 470 billion.

The doors of the mutual fund industry were opened to the private sector in 1993. Kothari Pioneer MF was the first private sector MF launched in July 1993. The year also saw the first formal MF regulations, surprisingly UTI did not come under the ambit of these regulations. The industry body Association of Mutual Funds in India (AMFI) was set up in August, 1995.

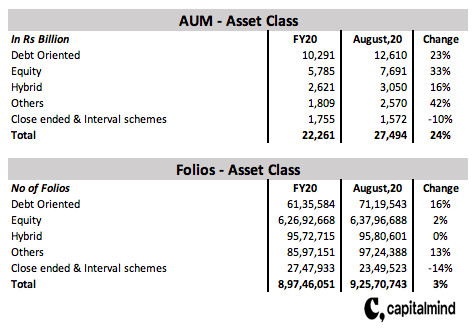

The AUM of the Indian MF industry has increased from ₹ 1,100 billion to ₹ 22,300 billion in FY20, registering a growth of 16%. The AUM for the last 5 years has increased from ₹ 12,300 billion to ₹ 22,300 billon.

Net AUM of the industry at the end of August,2020 stood at ₹ 27,494 billion. Debt oriented schemes formed 46% of the total assets. Below is the break up of the AUM by asset class for FY20 and August,20. The no of folios for each asset class is also shown below

Of the 12,610 billion of assets for debt oriented funds, 4,274 billion were liquid and money market funds. Others include – Index funds, Gold ETFs,Other ETFs,FOF overseas and solution oriented schemes. FMPs form majority of the close ended schemes.

ETFs are worth a mention here, they formed 0.8% of the industry AUM in FY14 and as on August,2020 were 8% of the AUM. In the four months between March,2020 and August,2020, the ETF AUM increased by 41% from 1,465 billion to 2,065 billion.

ETFs formed 0.8% of industry AUM in FY14. In August 2020 they are now 8% of AUM. In the four months between March,2020 and August,2020, the ETF AUM increased by 41% from 1,465 billion to 2,065 billion. Click To TweetThe surge in the AUM can be attributed to the EPFO monies investing in these ETFs. SBI and UTI are the major players in this space. This segment is dominated by Institutional investors, however retail participation is picking up (CPSE and Bharat 22). The ETF share in the US is 35-40% and there is a long runway for these products in India.

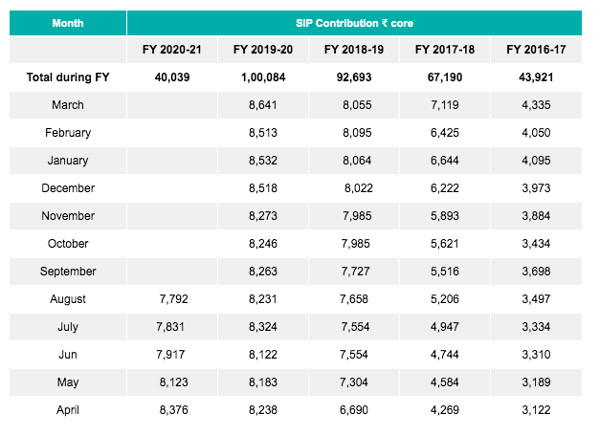

SIPs are a powerful and popular tool among retail investors. The SIP contribution has increased from ₹ 43,921 Cr in FY17 to ₹ 1,00,084 Cr in FY20. Below is the month wise SIP contribution for the FY17-20 period

Source: AMFI

Average AUM at the end of August,2020 was ₹ 27,781 billion. Some of the industry trends at the end of August,2020 are

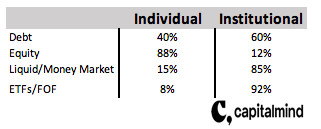

- AUM at the end of period is split in the ratio of 52:48 between Individuals and Institutions. Individuals held 53% and Institutions 47% at the end of August,19. Among the institutions corporates are 93% and balance is held by Indian and foreign institutions and banks

AUM of individual and institutional investors by asset class at the end of the period was

- Individual investors primarily hold equity oriented schemes, 68% of the individual investor assets are in equity oriented schemes. 75% of the institutions assets are held in liquid/money market schemes

- Value of assets held by individual investors in MF increased from 13.49 lakh Cr in August,2019 to 14.32 lakh Cr in August,2020. Value of institutional assets has increased from 12.25 lakh Cr in August,2019 to 13.46 lakh Cr in June,20

In September,2012 SEBI mandated mutual fund houses to offer their products through the direct route alongside distributors or the regular plan. This was a popular step and AUM’s under direct plans have grown at 25% CAGR over the last 6 years. Direct plans now account for 45% of the industry’s AUM, these plans accounted for 35% of the assets in FY14.

The split between direct and regular changes as per asset class and class of investors. Individual investors prefer hand holding and 86% of retail and 78% of HNI’s assets are through regular plans.

In terms of asset class,81% of the equity assets are through regular plans and 47% of the debt AUM is from regular plans.

Direct plan is the most preferred option for investments in ETFs and FOFs. 80% of the inflows come from the direct plan. Liquid/money market funds are popular among institutions and 72% of the inflows come through the direct plan.

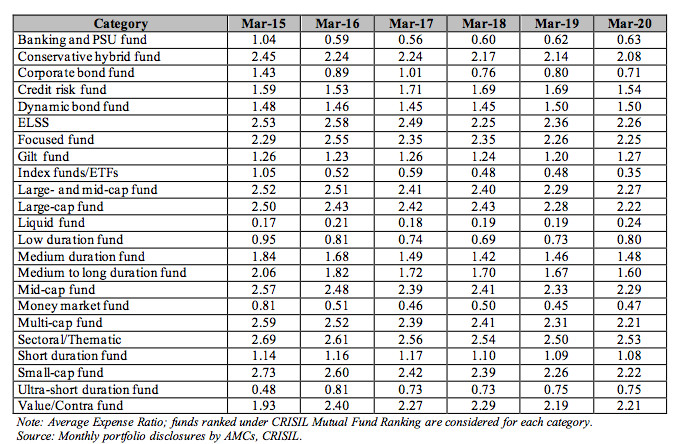

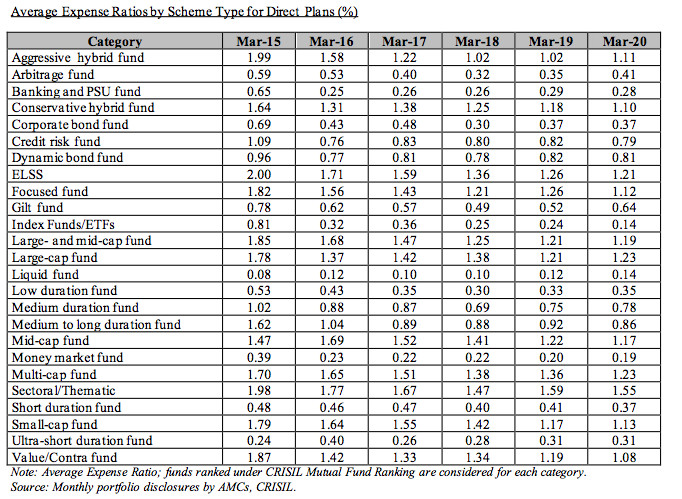

Below are the average expense ratios by scheme type of direct and regular plans

Source: UTI AMC, DRHP

Players in the Mutual Fund Industry

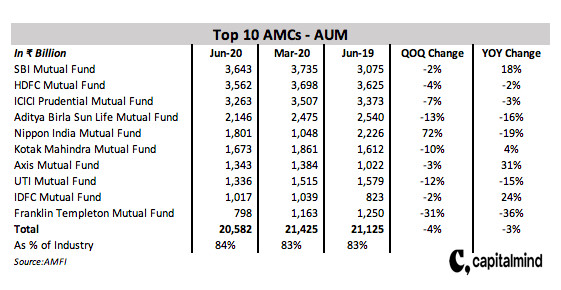

The MF industry is highly fragmented, there are 43 AMCs in the Indian market, however 84% of the AUM is with 10 players. Below is the split of the quarterly AAUM by AMC at the end of June 30, 2020

The largest AMC in the country is SBI with QAAUM of ₹ 12.68 lakh Cr, this is if we were to account for its PMS and NPS business as well. UTI is in the second spot with AAUM of ₹ 9.76 lakh Cr. We will talk about the PMS and NPS business of UTI later in the post.

If we were to consider only AAUM of the domestic MF industry, SBI is the leader with AAUM ₹ 3.64 lakh Cr, followed by HDFC with ₹ 3.56 lakh Cr. UTI is the 8th largest with AAUM of ₹ 1.33 lakh Cr.

Below is the AAUM of the top 10 players at the end of June,20 in comparison to March,20 and June,19

While we know that Franklin has been losing its AUM due to the shutdown of its 6 fixed income schemes, it is interesting to note that Nippon’s AUM has increased by 72% QOQ and Axis and IDFC’s AUM has increased by 31% and 24% YOY.

40% of the AUM of the top 10 players is in equity funds, 30% in debt, 23% in liquid/money market and 7% others.

The IPO Candidate: UTI

UTI AMCs predecessor Unit Trust of India was established in 1964. In 2002, Unit Trust of India was bifurcated into two separate entities – SUUTI, which would manage assets of Unit Trust’s flagship brand Unit Trust 64, the other entity was UTI Mutual Fund. It’s sponsors were SBI, LIC, PNB and BOB. UTI AMC was incorporated on November, 2002 and appointed by the trustees to manage the funds of UTI MF. In January 2010, T. Rowe Price Group acquired 26% stake in the company. UTI AMC has 4 subsidiaries.

Business Verticals

UTI AMC derives revenues from 4 streams – domestic MF business, PMS, Retirement solutions, Off shore fund management and AIF. Let us look at each of these verticals

Domestic MF

The company manages 153 domestic MF schemes across equity, hybrid, income, liquid and money market funds as on June 30,2020.

Below is the QAAUM of UTI for the last 4 financial years and on June 30, 2019 and 2020

Observations from the above table

- Equity AUM has increased primarily on the back of passive funds, share of passive funds in total AUM is 18% on June 30,2020 as compared to 2% in FY17

- Income funds formed 14% as on June 30,2020 of total AUM as compared to 37% in FY17

At the end of September,2019 close ended income funds had an QAAUM of 119 billion and there were 125 schemes offered by UTI in this space.

Below is the QAAUM and number of schemes as on June 30,2020 for the categories of domestic MF that the company manages

Fees: Source of Income for an AMC

AMCs generate income mainly from the fees which are based on specified percentages of the net asset value of the funds that they manage. These are called “Management Fees”. This fees covers fund management services and support services such as fund accounting and other administrative functions.

Fees charged for equity and hybrid funds (other than passive) are higher than fees charged for income, liquid, money market and passive funds.

In the case of domestic MF management fees is accrued to cover management fees and other expenses, based on regulation or internal limits set by the AMC. Management fees are paid by the funds to the AMC on a weekly basis and expenses accrued are used by the funds to offset other permissible expenses.

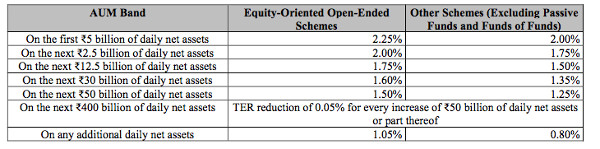

Percentages that AMCs can charge are regulated and are called Total Expense Ratio (TER). TERs are calculated by dividing the total costs of the fund by its average total assets.

Scheme expenses – including all management fees, distributor and agent commissions, RTA fees, custodian fees, audit fees, insurance costs, bank service charges, marketing and selling expenses and investor communication costs must not exceed the applicable TER for a scheme. New issue related expenses are borne by the AMC and not the scheme.

Passive funds have a maximum TER limit of 1% of daily net assets. Close ended and interval funds have maximum TER limit of 1.25% for equity oriented schemes (65% invested in equities) and 1% for other schemes. Open ended schemes (other than passive and FOFs) TER limits vary by AUM band, this is shown below. The below TER limits were set by SEBI with effect from April,2019

Source: UTI AMC, DRHP

In schemes where there are exit loads, incremental TERs of 0.05% are allowed. Incremental TERs increase by 0.30% in respect to sales in B30 cities.

Management fees with respect to the domestic mutual fund business forms about 73% of the company’s total income.

Other key features of UTI’s domestic MF business

- Distribution network of 163 UTI financial centres, 257 business development associates and 53,000 IFAs

- 44% AUM from individual clients and 46% from corporates

- 10.9 million folios, 12.2% folios of the industry as on June 30,2020

- SIP AUM of Rs 100 billion, average transaction size of ₹ 2,680 and 12.04 lakh live SIP folios at the end of June 30,2020

- 31% of distribution through IFAs and 55% direct. In the case of equity and hybrid funds the scales tilt – 61% through IFAs and 28% direct

PMS

The PMS business was started in 2004 and UTI offers discretionary and non-discretionary PMS. The company also offers research based advisory services for both domestic and overseas clients.

Below is the AUM for the PMS and other businesses for the last 4 years and June 30, 2019 and 2020

The increase in the PMS AUM is due to the CBT and EPF handing over additional portfolio of ₹ 3,283 billion on April 1, 2019. In September, 2019, UTI was selected as one of the two fund mangers to manage the corpus of EPFO for period of 3 years and in October,2019, UTI was approved to manage 55% of the corpus of CBT, EPF for 3 years starting November,2019.

UTI is also the fund manager to Postal life insurance fund and Rural post life insurance fund, it manages 8.3% of its PMS AUM for these entities.

The fees charged in the PMS business is based on the relationship with the client, fees charges is less than the domestic MF business.

Retirement Solutions

UTI was one of the three AMCs appointed by Pension and fund regulatory and development authority (PFRDA) in 2007 to manage pension funds for central and state government employees under the NPS. UTI has a subsidiary UTI RSL to manage such funds and since 2009, NPS contributions from citizens other than government employees are also accepted.

Offshore and AIF

UTI international offers funds to offshore investors who want to invest in India. There are 3 offerings in this segment.

In the AIF business, UTI seeks to invest across various sectors. The AIF business has varying fee structure around annual management fee and performance linked incentive.

UTI provides its services to SUUTI and generates 1.3% of revenues from these services.

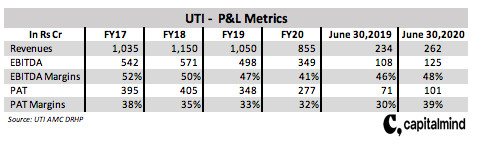

Below is the some important P&L metrics for UTI AMC

The average ROE and ROCE for the FY17-20 period was 12% and 16%. Average ROE of HDFC and Nippon in the same period was 38% and 21% . Average ROCE was 55% and 29%.

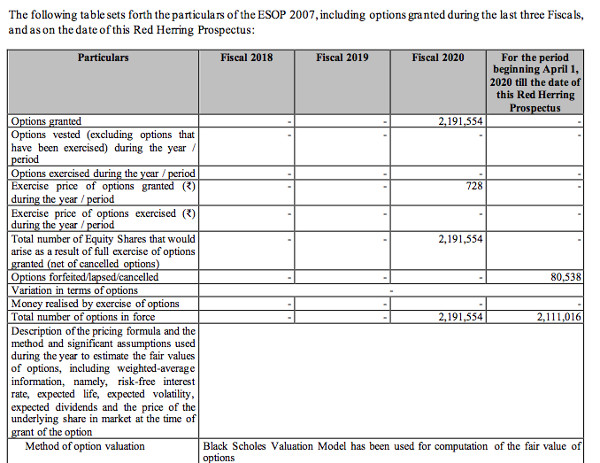

ESOP

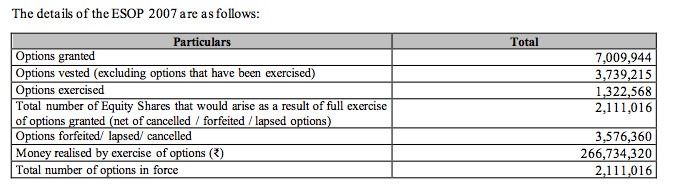

The company has an ESOP plan 2007, the details of which are shown below

Source: UTI AMC, DRHP

There have been options granted in FY20, details of which are as below

Source: UTI AMC, DRHP

In total 43.02 lakh options are outstanding, if all of these are exercised equity shares outstanding would increased by 43 lakh shares, 3% of the current shares outstanding. The options granted in 2020 have an exercise price of Rs 728/share, 31% higher than the offer price of Rs 554/share.

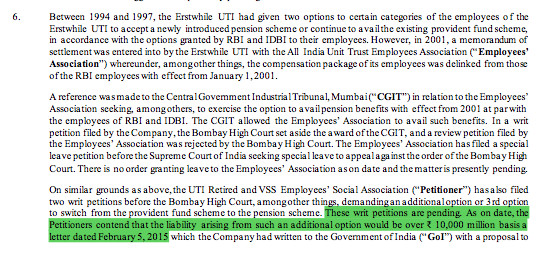

UTI Employees Association Versus UTI AMC

UTI retired and VSS employees social association has filed petitions in the Bombay high court demanding a switch from the earlier provident fund scheme to pension scheme. The estimated liability of this switch is Rs 1000 Cr. A third party agency has calculated the liability to be in the range of Rs 365 Cr – 721 Cr. Liabilities arising in the future will be borne by the government of India. Currently these petitions are pending. Although any liabilities arising in the future will be borne by GOI, we do not know how this will pan out, we will have to have a closer look at this development and see if any liabilities actually arise and who will actually bare it.

Source: UTI AMC, DRHP

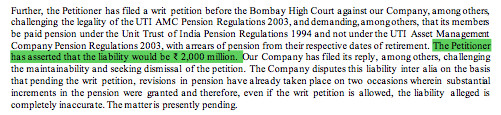

Another litigation is where the same association has filed a petition against the company is challenging the legality of UTI AMC pension regulation,2003. The demand is to be paid pension under UTI pension regulations, 1994. The estimated liability arising out of this is Rs 200 Cr.

Source: UTI AMC, DRHP

Final Thoughts

The EBITDA and PAT margins of the AMC business are very attractive, however we shouldn’t be lured by it. The industry is highly competitive as is evident from the number of AMCs in the country, the leader in the domestic MF space has a market share of 14%.

There are three key drivers which help the AMC generate revenues

- Price – Which is the expense that the AMC charges the customer, in the domestic MF industry it is TER

- Quantity – Size of the AUM

- Nature of the AUM – Split of the AUM among asset class. Equity and hybrid funds generate higher fees for an AMC as compared to debt funds. AMC make more money by managing active funds than passive funds

Below is the split of top 10 AMC’s AUM as on June 30,2020 by asset class.

Source: UTI AMC DRHP

Franklin and AXIS have +50% AUM in equity funds. As discussed earlier, equity funds generate higher fees than debt and passive funds. The other listed players HDFC and Nippon have similar percentage of their AUM in equity funds. UTI has 32% of its AUM in equity funds, 17% of its AMC is in gold and other ETFs.

However in the AMC business it is not only quantitative factors that matter, there are softer or qualitative factors that also matter. The AMC business also depends highly on trust, transparency and honesty. Take the case of Franklin Templeton, its AUM at the end of June,20 was ₹ 798 billion as compared to 1,250 billion a year ago, after it decided to shut its 6 schemes earlier this year, investors started withdrawing from its other schemes. Its equity fund manager had to come and assure investors about the safety of their equity investments. Reputational risk in this business is more than other businesses.

Stability of AUM is another important aspect of the business. Companies with strong brands will find it easy to retain customers and AUM. In the table posted earlier in the post we can see that changes in HDFC and ICICI’s AUM is a narrower band as compared to the other AMCs. In tough times customers would want to stick to stronger and trusted brands.

Other risks that AMCs face are regulatory risks, credit risk, liquidity risk. This was evident from the recent Franklin episode.

There are two listed AMC players, below are their key metrics in comparison with UTI for the FY18-20 period.

HDFC trades at an EV/EBITDA of 27 and Nippon 24. The margins of HDFC are superior to Nippon and UTI.

UTI expects to garner ₹ 2,160 Cr from the sale of 3.89 Cr shares at the price of Rs 554/share. At this rate the market capitalisation of the company would be around ₹ 7,025 Cr. If we were to consider UTI’s EBITDA of ₹ 349Cr in FY20, this translates into EV/EBITDA multiple of 20. UTI has an added advantage of sticky money in the form of EPFO inflows. The EPS for FY20 was Rs 22, at the offer price of Rs 554/share, investors are paying 25X earnings.

UTI expects to garner ₹ 2,160 Cr from the sale of 3.89 Cr shares at a price of Rs 554/share. This means a market capitalisation of ₹ 7,025 Cr. With FY20 EBITDA of ₹349 Cr in FY20, that's 20x EV/EBITDA. Click To TweetThe active equity AUM of UTI as on June 30,2020 was Rs 333 billion, this is the same as it was in FY17. Growth in equity AUM has mainly come from managing passive funds. PMS and retirement solutions business have also helped in increasing the companies AUM, these however earn less than active equity funds.

We would like to see growth in the active equity AUM and steps that the company takes in improving its EBITDA margins, margins have been falling since FY18. We will skip this issue and wait for important metrics to pick up.

NOTE: There is no other relationship between Capitalmind and the above company. Please do not consider this article as a recommendation, It is purely for information purposes only.