There’s a “high yield” market in India. Some of it is of shady companies. But some of it is for reasonable good corporates, whose bonds are listed on stock exchanges.

So does this provide an opportunity? We will get into details, but let’s see how bond pricing works.

Historically the yields of bonds have been related to majorly three major factors.

- Prevailing Yields on G-Sec

- Credit worthiness of the firm (Credit Risk)

- Specific features of the bond (call option, secured/unsecured etc)

- Duration of the bond

G-Sec Yield As Benchmark For Bond Yields

Government Securities (G-Secs) have always been the navigator of sorts for interest rates prevailing in a country. This is basically taking out one factor (credit worthiness) since we know the government has the ability to pay back or even print money to pay back if required.

G-Secs are guided by the repo rate (decided by RBI). RBI takes a call on repo rate in its bi monthly monetary policy meets. Since G-Secs have no credit risk, the yields on the corporate bonds – which have a risk of default – have a spread over the G-Sec yield.

A “spread” is the difference between the G-Sec yield and that of the corporate bond.

The spread is mainly on account of chances of default (as corporate entities are not guaranteed to be risk free). The spread differs from entity to entity. The higher the spread the more riskier the bond is.

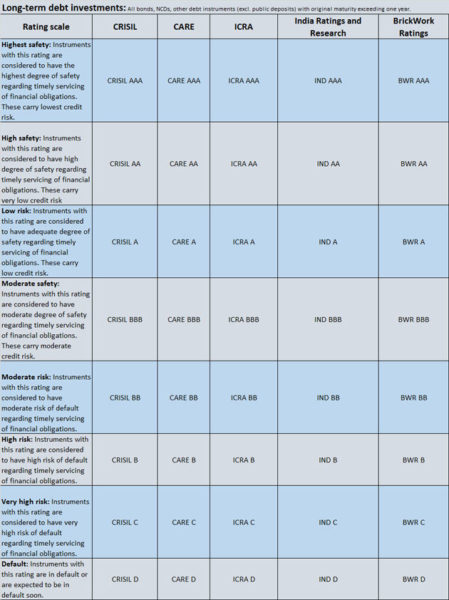

The Credit Worthiness Of the Firm

A credit rating gives us SOME indication. AAA rated bonds will have lower yields compared to a AA bond. The rating agencies periodically check for the credit worthiness of the firm in terms of cash flows, profitability etc and assign a rating. A rating downgrade will increase the spreads and a rating upgrade will contract the spreads. A low rated (BB-) and high yielding bond might not actually default on its payment. The low rating only means the chances of default are higher.

Image Source: Economic Times

Duration

Yields are also dependent on the amount of time remaining on the bond. The longer the duration the higher the risk. As the duration increases, the uncertainty increases or the vision of foreseeable future diminishes thus creating higher risk.

That’s the reason a bond issued by a same firm with a maturity of 8 year and 2 year have different yields. 8-year maturity bond will have slightly higher yield compared to a 2-year maturity bond. The difference in the yield will be marginal.

At the fag end (may be 2-3 months before maturity) of the maturity of the bonds, investors tend to sell bonds just before the maturity on account of a potential tax arbitrage. If you hold a bond till maturity then the earning is considered as interest and if you exit in before maturity it comes under capital gains. Capital gains tax can be offset by capital losses, so it’s a relatively lower tax (taxation of interest income will be in line with your tax slab)

The Current Context.

In the current context we will consider the above three factors and how it has impacted the bond yields.

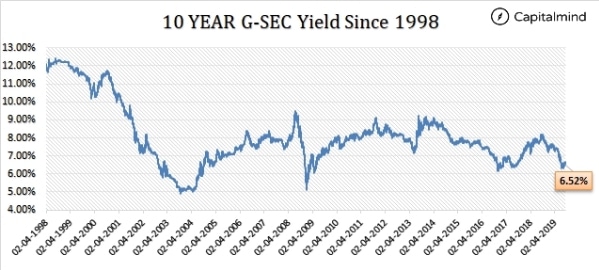

The yields on G-Sec have been tapering off as the RBI is going for rate cuts owing to low inflation. The current yields on a 10 year G-Sec are at roughly 6.52%. The yields have been dropping post October 2018. Meaning the bond yields of corporate firms should follow suit.

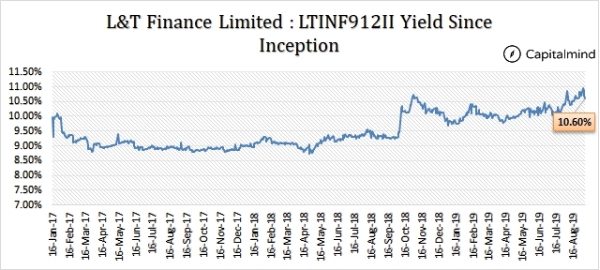

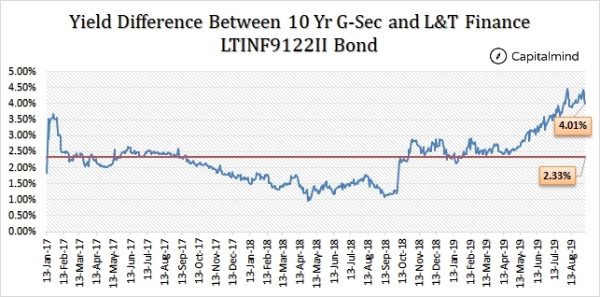

Corporate bond yields (as traded in the market) have bucked the trend and are going in the reverse direction. The yields of the bonds have been increasing in the same period. For instance bond yields L&T Finance Limited 912II Series have increased in the same period of time.

Its not only L&T, the trend has been followed by most of listed corporate bonds. For instance the government backed PFC bond yields have been hovering around 9% (same as last year). The yields have increased or have remained same since October 2018. The lower yields across G-Secs is not been followed by the corporate bonds. So we need to check for the second question viz. have the ratings or creditworthiness of the firm changed?

L&T Finance is still a AA+ rated bond, same as it was last year. If a bond has a rating BBB and above (BBB, A, AA and AAA) are considered investment grade. A rating of AA+ is believed to be of high quality. Then why is a AA+ rated bond yields are increasing when G-Secs yields are falling? Is it something to do with duration?

The maturity period of the bonds are changing too. As the maturity nears the yields should be falling. In the above case L&T Finance Bond has a maturity at 10th Jan 2022. Another three years. This has however seen a RISE in yields since Oct 2018.

Why? The IL&FS default tampered the trust factor in the bond market. This led to selling of the bonds in open market, triggering increase in the yields. And post DHFL and India Bulls crisis even housing finance firms faced the heat. On the other hand yield on G-Secs has been going down due to RBI rate cuts. Therefore the gap between yield of G-Secs and corporate bonds has been rising.

Is this going to stay this way? Unlikely. At some point the yields start looking attractive. The NBFCs are a parallel banking system catering to the customers not having seamless access to banking system. The government/RBI is also taking active steps to ease out the steps by infusing excess liquidity in the market. Simultaneously the banks are also buying securitised loans from NBFCs giving them some cash buffer. At some point bond yields have to normalise.

The important question is “When”? That we don’t know. But in a medium-term range of 1-2 years, things will cool off and return to normalcy. Once it returns to normalcy the yields will fall and you can see capital appreciating.

Here we try to analyse bond yields for five different corporates viz. PFC, IDFC First Bank, Manappuram and L&T Finance to demonstrate the capital gains once the yields start normalising

Note: The data used is as of 6th Sep 2019

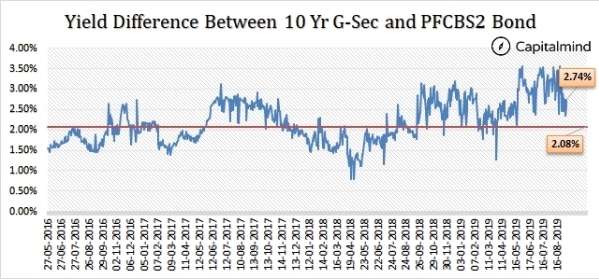

Power Finance Corporation.

We took PFC BS2 series bond. The bond is cumulative in nature and is AAA rated by CRISIL. Has a coupon rate of 8.30% and matures on 31st Mar 2021. The bond is currently trading at 9.31%. The current differential between yields of G-Sec and PFC BS2 bond are 2.74%. Historically the median yield difference has been at 2.08%.

So assume post one year the G-Sec yields remain same and things tend to normalise, then PFC BS2 yield tend to revert back to the normal range (G-Sec + 2.08% spread). The fall in yield will be roughly by 65 bps.

If the yield falls by 65 bps then bond prices tend to be at 10,598 in next one year. A capital gain of 9.71% from the current price. As these are cumulative bonds the capital gain is intrinsic of interest rates as well.

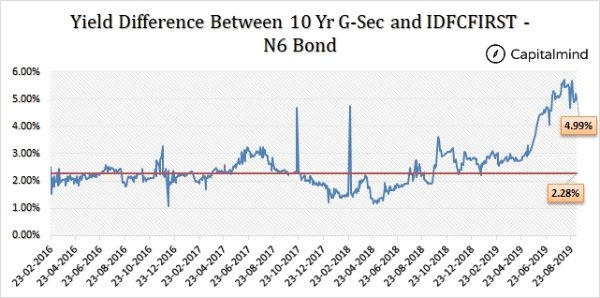

IDFC FIRST BANK

Similarly the IDFC First – N6 series bond is AA+ rated and has a maturity at 21st Feb 2021. The current yields are at 11.56%. The differential between G-Sec yields and IDFC FIRST N6 Bond is at 4.99%. Historically the median has been at 2.28%.

Assuming post one year the G-Sec yields remain same and things tend to normalise, then IDFC First N6 yield tend to revert back to the normal range (G-Sec + 2.28% spread). The fall in yield will be roughly by 271 bps.

If the yield falls by 271 bps then bond prices tend to be at 10,393 in next one year. A capital gain of 12.97% from the current price of Rs 9,200.

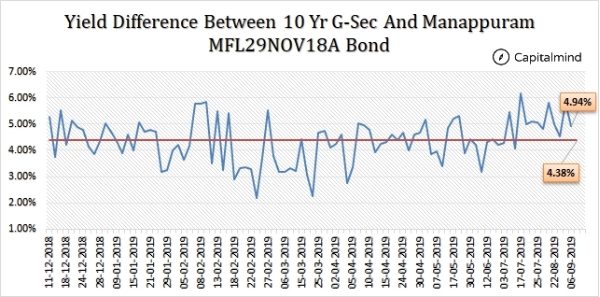

Manappuram Finance

Manappuram – MFL29NOV18A series bond is AA+ rated and has a maturity at 29 Nov 2020. The current yields are at 11.54%. The differential between G-Sec yields and Manappuram Bond is at 4.94%. Historically the median has been at 4.38%.

Assuming post one year the G-Sec yields remain same and things tend to normalise, then the Manappuram bond yield tend to revert to the normal range (G-Sec + 4.38% spread). The fall in yield will be roughly by 56 bps.

If the yield falls by 56 bps then bond prices tend to be at 1179.5 in next on year. A capital gain of 11.80% from the current price of Rs 1,055.

L&T Finance

L&T Finance Limited – LTINF912II series bond is AA+ rated and has a maturity at 10 Jan 2022. The current yields are at 10.60%. The differential between G-Sec yields and L&T Finance Bond is at 4.01%. Historically the median has been at 2.33%.

Assuming post one year the G-Sec yields remain same and things tend to normalise, then the L&T Finance bond yield tend to revert to the normal range (G-Sec + 2.33% spread). The fall in yield will be roughly by 168 bps.

If the yield falls by 168 bps then bond prices tend to be at Rs 2110 in next on year. A capital gain of 12.94% from the current price of Rs 1,868.

After seeing the above examples, two basic questions pop up.

What happens if G-Sec Yield increases?

Assume G-Sec yield increases by 50 bps in next one year. One reason for that could be a return to an inflationary regime; If that happens, the economy will be more normalized (less panic). Panic is what has widened the spread between the G-Sec and the corporate bond yield. If there’s less panic, the spread will narrow, and the rise in the G-Sec will get offset partially by a narrowing differential.

What Happens if Yields Don’t Revert to Median?

If yields don’t revert to Median value, then consider only this: are you happy with a 9% return? The current yields are better than most of the alternative options in fixed income portfolio. Think of the extra added returns from normalisation of bond yields were extra offering (may be or may not be).

Before you buy bonds one needs to ask following questions to oneself?

Is the firm going to default?

You don’t want a defaulting firm, but no one does. It’s useful to look at downgrades, and why a bond is being downgraded, and to exit if that reason is sinister. If a bond rating says it’s stable, or positive, that’s not the end of it – you’ll have to still do more research to see promoter integrity, company’s balance sheet and such.

How long should I hold the bond?

If you plan to hold till maturity, then see that are the current yields of the bond will meet your expectation. For instance the above L&T finance bond having yield of 10.6% might be good enough for you to hold till 2022.

If you plan to sell, there’s a couple of issues:

- Interest rate risk : a rise in rates in the interim will drop your bond price, making it less profitable (or loss making!) to sell

- Liquidity risk: You can’t sell if there’s no buyer. And bonds are illiquid.

Is there Enough liquidity in the market?

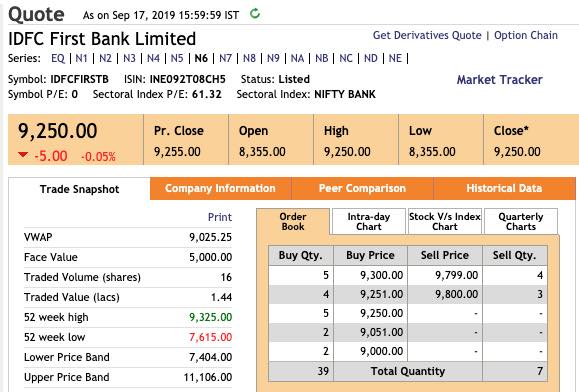

No. This is a problem. Look for any of these bonds (and others like these) on NSE or BSE, and you’ll see the problem, with low volumes of these bonds changing hands. The bids and asks on some of these look like they are not even for the same security, that’s how far apart they sometimes are.

Here’s a look at the IDFC First Bank N6 bond as of Sep 17th. Notice the quantities available for sale and the difference between the highest Ask and lowest Bid price.

What if you needed 50 of these bonds at ₹ 9,400 (that’s ₹4.7 Lakhs at a yield of 10.17%)?

Time for a plug. We thought of this and started the CM Bond Desk.

To make it easier for retail investors to buy bonds without the pain. It’s simple. We accumulate bonds over a period of time. At the same time, we’d like to sell them at reasonable yields and quantities. We do this on the exchange, meaning, they are available for anyone to buy. If you are signed up for our Bonds Mailing List, you receive updates (2-3 a week) on bonds available and their yields. If you see something you’d like to buy, log in to your trading account and place a Buy order.

You can read more in the introductory post about the Bond Desk.

You can sign up for the mailing list here (unsubscribe anytime):