CPI Inflation for Sep 2018 came in at a meagre 3.77% basically because food prices didn’t go up much. This is a refreshing release because of one thing: RBI. We’ll come to that, but look at how inflation has been:

In fact, last year inflation rose from a low of 1.5% in July 2017, to 5.2% in December.

With a rising base, unless inflation keeps going up, we aren’t going to see big headline numbers.

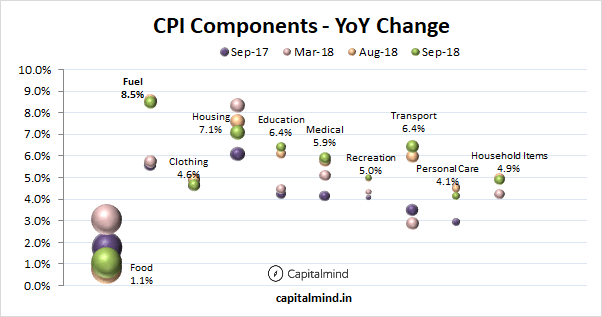

Components: Food Makes Up For Fuel

Food inflation was a meagre 1.1%, and food is nearly half of the index. Fuel inflation though was 8.5% on the back of rising crude and a falling rupee, and while it’s high, fuel is just 6.8% of the index, so it’s more than offset.

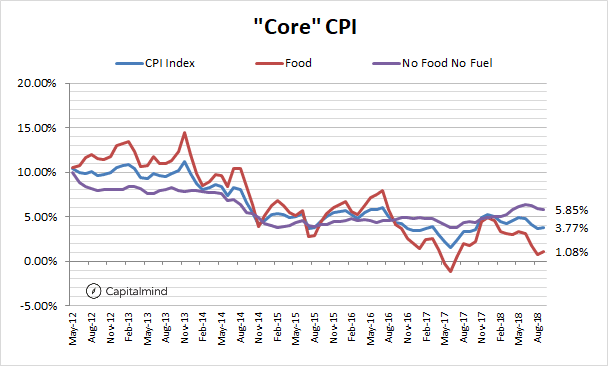

Take out Food and Fuel: We’re Not Trending Up

I’ve made the argument before that core inflation is a problem if it’s rising. Core means stuff that’s not volatile like food or fuel. Core is more intrinsic; like if fuel prices go up they can come down, but when bus fares are made to rise because of rising fuel prices, they may not reverse easily.

Core inflation too isn’t rising – it is flat, just short of 6%. Again, this is not a major concern.

What’s The Takeaway?

It’s not really a big deal that your inflation isn’t the same as the inflation seen in the headline numbers. Food for you probably is a much smaller part of the monthly budget than for most of India. In fact, I was recently praising the food delivery startups for allowing me to be lazy and order food in at 50% off, so even I haven’t seen that much food inflation even when I didn’t actually cook.

The point is that the index applies for a significant part of India, and those people don’t see that much inflation in the basics – food, shelter and clothing. When they do, the RBI is likely to start to act.

If RBI sees no inflation, the monetary policy committee is unlikely to want to raise rates. That’s by design. Because parliament has told them to focus on only one thing – keeping inflation at 4% with a buffer on each side (can go from 2% to 6%). At this point, inflation’s lower than the target. So raising rates is unncessary and perhaps even against the legislated purpose of the MPC.

(To state clearly: If the MPC was told that their job was to protect the rupee, they would perhaps have had to raise rates. But that’s not their purpose, and any change in purpose needs to come from parliament)

At this point, high fuel prices haven’t translated to high inflation on the ground. The bond markets have been fearing a rise in rates, and perhaps that will now ease up.