Update: This post is now free for all users. We sent this to Premium customers a few days back. We have also incorporated answers to our questions from DHFL Pramerica and will update further as we get more clarifications.

The Ballarpur Default had one big victim: Taurus Mutual Fund. But Taurus owned just 100 cr. or so of Ballarpur Debt. Was it the only Mutual Fund to have been caught unawares?

Answer: no. There were at least four other mutual funds holding Ballarpur Debt till November 2016. We look at each one.

Reliance Mutual Fund: 125 cr. But off the MF books

Reliance Regular Savings Fund (Debt) had about 125 cr. of Ballarpur+Bilt Commercial Paper on its books. On 22 December 2016, this CP was “sold” at a yield of 11.75% in an off market transaction.

Given Ballarpur was days away from a default, it’s quite likely that no one else would have wanted to touch the debt (there are very few rookie fund managers in debt). This had to be sold to someone close to the AMC, we reckon, to avoid investors taking any hit. That 125 cr. is gone to someone else now, and it’s quite likely the Reliance MF folks know where it is.

You don’t need to take any action since any further issue will be handled by the Reliance AMC, and it doesn’t affect you.

Invesco MF: 100 Cr. but again, off the MF books

Invesco had about 100 cr. of Ballarpur debt (NCDs and Commercial Paper) till November 2016. They seem to have sold off that Debt after that, around the 13th to 15th of December. Again, this might sit on the books of Invesco, to protect mutual fund holders.

Again, for mutual fund holders, they are safe and protected.

IDBI MF: Bonds Mature But Receivables Go Up

IDBI owned Ballarpur securities till December end 2016. In their Debt opportunities fund (17 cr.) and Monthly Income Plan (4.25 cr.) and some others. These are small amounts, adding up to probably around Rs. 30 cr.

IDBI has however shown a much higher “receivable” number is the Debt Opportunities fund, of about 22 cr. (from about 5 cr.). This might indicate that they consider the Ballarpur Debt a “receivable” that has not yet come in.

(This is a problem – they assume all of the money comes in. Any one who exits now will get the full NAV, but anyone who waits will probably see the hit when Ballarpur doesn’t pay back much or at all, because then the receivable will have to be written off)

Aside: How MFs Downgrade Investments

Technically, a Mutual Fund should downgrade an investment when the credit rating agency downgrades it (end December). CRISIL and ICRA give values for each security and they consider downgrades and give lower values to those that are downgraded. Since commercial paper for Ballarpur was downgraded in end-December 2016, the valuation wold have come down (but not by too much since it was due to mature soon anyhow).

The bigger problem comes when a company doesn’t pay interest or principal, and actually defaults. A mutual fund that owns the paper can mark it to zero immediately (which is what Taurus did). Or, it can pretend and extend: Mutual funds get upto 3 months to recover the money, and if they don’t get that, they need to call it an NPA.

Even at “calling it an NPA” an MF doesn’t need to mark it to zero. It gets another three months (that is, 6 months from the default date) to mark it down to 10%. Then another 3 months for another 20%. Then, in every three months after, 20%, 25% and 25%. The asset is written down to zero in 18 months.

The problem is, however, that if you don’t mark them down, investors that exit will benefit unfairly versus those that stay. If you have a fund with just two investments of Rs. 100 each, and one has defaulted, you can technically tell the world you have Rs. 200 for six more months. Then it will go to Rs. 190 (the defaulted one marks down 10%). Nine months later, it falls to 170, and so on. But that also means that if an investor in such a fund gets out when you say 200, you have to pay him according to Rs. 200. So you’ll sell the good investment. You only have Rs. 100 of the good investment – so if enough people withdraw (half of the AUM), you’re hosed. The remaining investors will see all the losses, since you can’t recover from the defaulted debt. Which is why Taurus marked it down to zero immediately.

And which is why, if you own any units of IDBI Corporate Debt Opportunities Fund, you should sell them off now. They have apparently not marked down the value of the Ballarpur debt at all, or left it as a receivable, and they will need to do so at a future date. It’s in your best interest to get out – otherwise you will be left holding the bag.

The Scariest: Pramerica Puts Money In Promoter Company’s Unrated Debt

DHFL Pramerica is the scariest of the lot.

November 2016: It owned 179 cr. of Ballarpur/BILT debt in the Pramerica Low Duration Fund, 50 cr. in the Short Maturity Fund and about 45 cr. in the Credit Opportunities fund. That’s about Rs. 275 cr. in total.

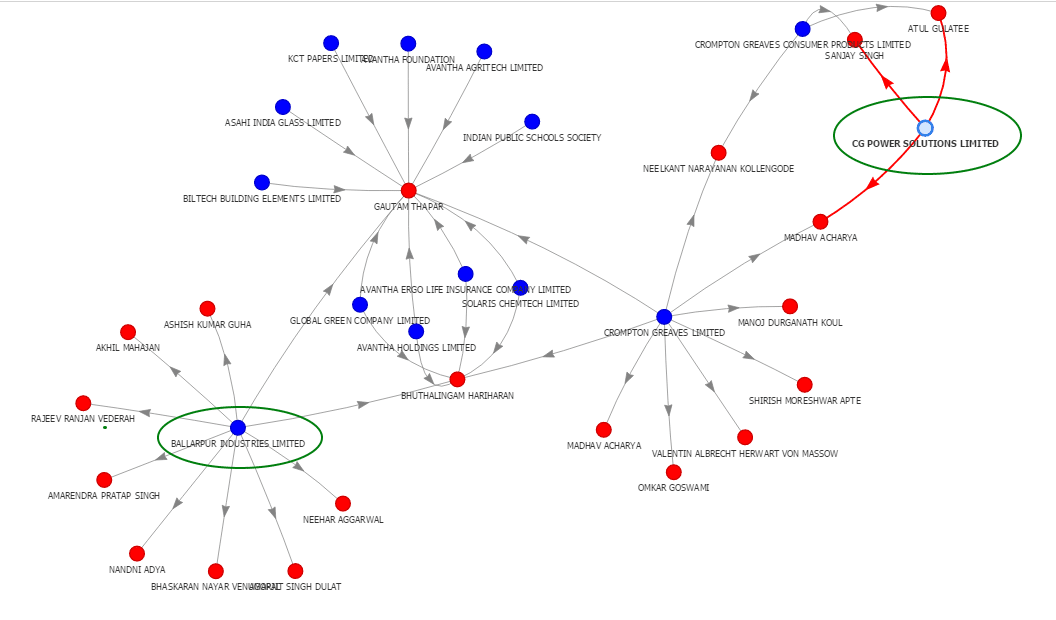

December 2016: Miraculously, the Ballarpur Debt vanishes. And it’s replaced by 200 cr. of debt to a company called CG Power Solutions. The debt is not rated. This company, we believe, is a promoter entity of Ballarpur – promoted by Gautam Thapar, who also owns Crompton Greaves (which saw a demerger of the retail entity recently). You can see the link on this excellent graph on Tofler.in:

So, while some 75 cr. of debt has somehow been returned (or is a receivable, which is still high in each of the funds) about 200 cr. of Ballarpur debt has been rolled into a promoter entity of Ballarpur. This is likely be to a mechanism to just push the default off the books – the new debt is exactly about a year old to avoid a rating requirement (any thing less than a year has to be rated) and the new entity (CG Power Solutions) is not something that seems to have operational revenues. (There is a similar company, CG Power and Industrial Solutions Ltd., which is listed and has revenues, but they are not the same entity)

Secondly, if you look at the bonds that have been issued by CG Power Solutions, there is a repayment every month (of principal) required. Two bonds are issued – one of 84 cr. and one of 116 cr. The 84 cr. bond requires repayment of about Rs. 3 cr. every month from January till November and then a big bullet in December. Given that the outstanding in Feb 2017 for this bond in Pramerica’s books is the same as in December, we can assume that there was no such repayment in Jan and Feb. Meaning, this bond has already defaulted.

The second bond of 116 cr. requires a 12 cr. repayment on March 24, 2017 and then further payments each month. If that doesn’t come by, then the second bond would ALSO have defaulted.

Effectively, the fund has kicked the can down the road. We now have to take action accordingly.

What does this mean?

If you own these funds:

- DHFL Pramerica Low Duration Fund

- DHFL Pramerica Credit Opportunities Fund

- DHFL Pramerica Short Maturity Fund

You want to exit immediately. This problem debt is not liquid. These funds have other assets – the Low Duration Fund and the Short Maturity Fund have more than Rs. 1500 cr. in AUM and the Credit Opportunities Fund has 750 cr.

However once this problem is known, other, larger investors will exit and if you stay in the fund, you will be left holding the bag – because for any exits, Pramerica will sell the liquid and better investments first, and what’s left will be the bad stuff, for whoever didn’t sell their units.

The investment in CG Power Solutions by Pramerica seems to be an approach to push the default to later. The debt is unrated, so a rating agency can’t even now say that a further default has occured, but it seems to us that it has already defaulted.

The bigger question is: How does this unwind? At some point, Ballarpur has to be forced out of the hands of Thapar, and sold to the highest bidder. It’s a company with Rs. 7000 cr. of debt and only a fraction of it is held by mutual funds. This resolution could either take years, or be done fast – in India, no one tries hard enough so it takes long.

There is a systemic risk in telling investors to exit now, because it could cause a run on Pramerica’s funds. However, in the light of their transferring debt to an unrated set of bonds and maintaining high receivables, it does not give us confidence that such an action is in the best interest of mutual fund investors and an exit from these funds is warranted.

(Note: this doesn’t impact any other fund, including DHFL Pramerica’s equity funds)

If anything, SEBI should block all further entries (and exits) from these funds, extricate the problem debt and keep it in a separate entity like JP Morgan MF did with the Amtek Auto debt. And they should allow all funds (including Taurus) to do this for any default. We know there will be more such issues, and it’s better to address the issue now.

Our reaction to the Taurus debt NAV fall was: Don’t sell your units, you will take 100% loss where there is a potential to get something back since the Ballarpur debt was marked down to zero. Our reaction to the mechanisms used at IDBI and DHFL Pramerica funds are: Sell now because they didn’t mark it to zero – in fact they didn’t mark it down at all.

The optimal markdown would probably be somewhere in between, but in our relatively undeveloped debt market and inability to resolve debt quickly, there can only be extremes.

Update: Response from Pramerica and Our Views

We had some proactive responses from DHFL Pramerica who we asked these questions, and some follow ups. A comprehensive set of replies from them:

1) Has the CG Power Solutions bonds that had repayments in Jan and Feb 2017 defaulted on those payments to you? As the debt is unrated we are unable to ascertain the above.

DHFL Pramerica: Our bonds of Crompton Greaves Power Solutions Ltd. (CG Power) had no repayment obligations in January/February 2017 and as such there has been no default whatsoever in these bonds. Furthermore, we have a Private rating outstanding from one of the top two rating agencies on these bonds, which represent a high investment grade’ rating.

Capitalmind: We replied back with:

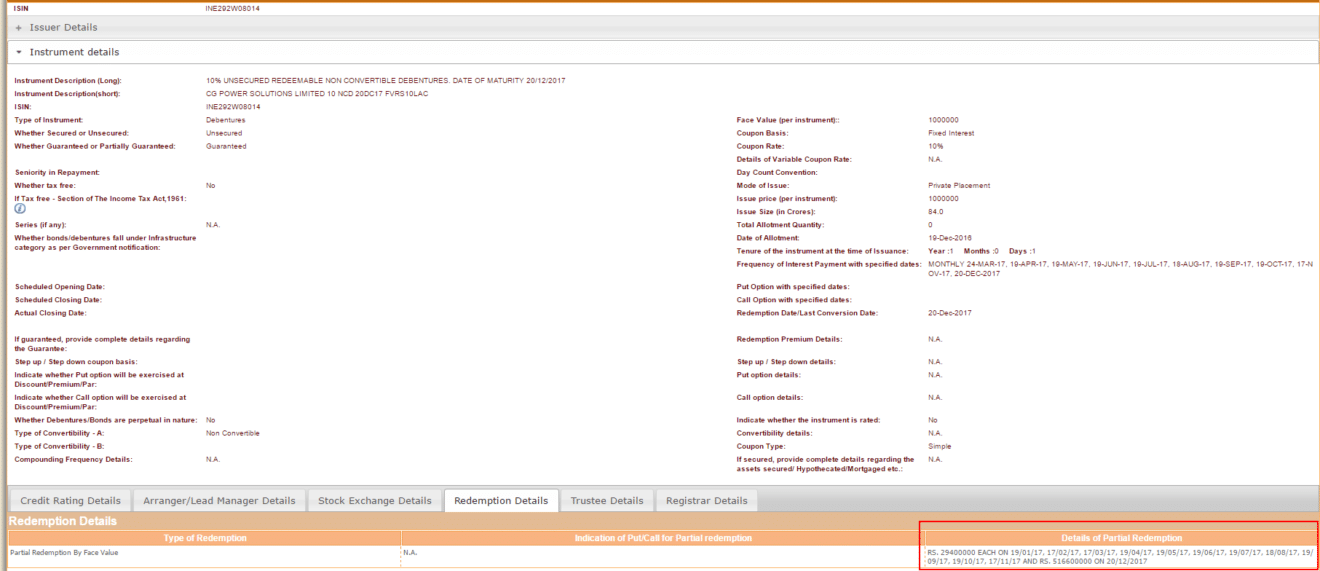

You mention the CG Power Solutions bond has no repayment obligations in Jan/Feb. However, when we use the NSDL Portal to find details of the bond (https://www.indiabondinfo.

(click for larger image)

As we can see it shows a repayment of 2.94 cr. required on 19th Jan, and same on 17th Feb. (2017)

If the bond was repaid in the above two installments, then the 84 cr. outstanding should have fallen to around 78 cr. as of end-Feb, but your portfolio as of end-Feb still shows 84 cr. outstanding for this bond.

This is why we believe the partial redemption has not happened, and therefore there are arrears. Could you clarify about this?

DHFL Primerica Replies:Upon the closure of the transaction in December it was noticed by the Company that NSDL had erroneously carried an incorrect repayment schedule in one of the bond tranches. The company then approached NSDL to rectify the repayment schedule. In fact on the NSDL website there are 2 locations wherein the repayment schedule is produced. While the error had long been rectified in the main screen, in one of the other tabs NSDL had not effected the change. I think this is the source of the confusion. The necessary information has since been updated at the other location as well, so that it is now consistent with a second series wherein we have also invested. Thanks for pointing it out.

Capitalmind: While this may be an error, it’s more likely to be a change in terms later, in our opinon. We have NSDL data from three sources, all of which include the Jan/Feb bullet payment. In any case, there is a repayment on 24th March 2017, and let’s hope that bond is repaid properly.

2) Do any of your “receivables” contain receivables from Ballarpur, the promoter company, or from BILT? If so, how much is due more than 30 days?

DHFL Pramerica: We would like to confirm that none of the funds of DHFL Pramerica Asset Managers has any outstanding whatsoever from Ballarpur Industries Limited (BILT), its subsidiaries or any of its promoter companies. As such there are no receivables outstanding against this account. All our ‘receivables’ in our funds are in the usual course and are ‘current’ and represent no delays or defaults.

Capitalmind: Fair enough, we thank them for the clarification.

3) Have you recovered any principal from Ballarpur, the Promoter companies or from BILT since Jan 1, 2017? If so, could you let us know the amount as a percentage of the overall outstanding?

DHFL Pramerica: We wish to clarify here that as at end December 2016, none of the funds of DHFL Pramerica Mutual Fund, had any outstanding whatsoever from Ballarpur, its promoter companies or from BILT. As such the question of recovering any outstanding in January 2017 or beyond does not arise.

Capitalmind: We have to take this answer, as the CG Power Solutions Ltd. company is not “technically” a promoter company. It’s an entity managed by the promoters but fully owned by another Avantha group company, CG Power and Industrial Solutions Limited. But it’s good to know that the Ballarpur debt (from Ballarpur and BILT) are fully repaid.

4) Is the CG Power Solutions debt backed with any collateral other than the corporate guarantee of Crompton Greaves Limited? Does Crompton Greaves Limited have enough revenues after the recent restructuring to back repayment of this debt as a going concern?

Note: We insert our clarifications in the middle here.

DHFL Pramerica: We would like to highlight that CG Power Solution Ltd is a 100% subsidiary of Crompton Greaves Ltd., (the listed flagship entity) which was recently renamed as CG Power and Industrial Solutions Ltd. (Parent). CG Power Solution Ltd is not a private company of the Promoters nor is it held by any Group holding company.

Our exposure under the aforesaid NCD is covered by an Unconditional, irrevocable and absolute Corporate guarantee of the Parent. The structure is also rated privately by a reputed rating agency and has been assigned a strong and high grade investment rating.

Capitalmind:

We went through the books of CG Power Solutions and it is indeed owned by the listed CG Power and Industrial Solutions Ltd. Here is its Annual Report and results. While it is a subsidiary of the public company, promoters will exercise substantial control over it, and in India such situations are not entirely uncommon. We understand that the bonds are unsecured but guaranteed by CGPower and Industrial Solutions Now as per your mail.

However the guarantee of a public company is usually given in a public rating document so that other lenders are aware of such debt, which is why we wonder why a rating was not immediately made public.

Could you clarify if:

a) you are aware of movement of funds from CG Power Solutions to Ballarpur/BILT in order to make the repayment

b) any guarantee from the parent has been revealed in any document to other lenders of CG Power and Industrial solutions (since CG Power solutions has heavy losses and won’t anyhow be able to pay back the debt)

DHFL Pramerica Replies:The prerogative to opt for an unrated issuance usually rests with the issuer. While we have the option to invest in ‘Unrated debt’ as per SEBI guidelines and our own investment guidelines, we opted to secure a private rating so as to obtain an additional input in our decision making. It is fairly common to see unrated instruments as well as privately rated instruments in mutual fund portfolios.

For example you may find such instances here:-

a) Franklin Templeton Corporate Bond Opportunities Fund: Privately rated investments

b) Birla Sunlife Medium-term Fund: Unrated securities

Corporate Guarantee structures are standard and are usually resorted to wherein potential investors draw comfort from stronger entities within a group over & above the primary borrower financial and credit profile.

To the best of our knowledge we are not aware of any movement of funds from CG power to Bilt. We are unaware of other instances wherein the parent may have offered a Corporate Guarantee to cover any of the other liabilties of CG Power.

There has been no change in the shareholding of CG Power Solutions from the time we have concluded our transaction. The reason for the omission in the entity from the list of subsidiaries at the end of December 2016, is because this list is not exhaustive and includes only those entities wherein a limited review was conducted. CG Power Solutons remains a wholly owned subsidiary of CG Industrial and Power Solutions Ltd. (the Parent).

For example you may find such instances here:-

a) Franklin Templeton Corporate Bond Opportunities Fund: Privately rated investments

b) Birla Sunlife Medium-term Fund: Unrated securities

Corporate Guarantee structures are standard and are usually resorted to wherein potential investors draw comfort from stronger entities within a group over & above the primary borrower financial and credit profile.

To the best of our knowledge we are not aware of any movement of funds from CG power to Bilt. We are unaware of other instances wherein the parent may have offered a Corporate Guarantee to cover any of the other liabilties of CG Power.

There has been no change in the shareholding of CG Power Solutions from the time we have concluded our transaction. The reason for the omission in the entity from the list of subsidiaries at the end of December 2016, is because this list is not exhaustive and includes only those entities wherein a limited review was conducted. CG Power Solutons remains a wholly owned subsidiary of CG Industrial and Power Solutions Ltd. (the Parent).

Capitalmind: On private ratings: this is what we would still call “Unrated”. In the Franklin fund these investments are about 1.88% of the fund (added up). Also, in the Birla medium term, it’s less than 1.5%. (Though there is a problem with the corporate bond fund where it’s 3.81%, and I’d do a double-check there)

In the Pramerica scheme, its about 6%, which is a slightly larger worry. SEBI allows each scheme to invest upto 10% in unrated debt, so there’s nothing illegal about this. It’s just the context that worries us.

DHFL Pramerica: ‘Private ratings’ are an accepted industry practice and are routinely sought by lenders/investors to further reinforce the quality of their investment decision. While ‘Public ratings’ are undertaken at the behest of the issuing entities (borrowers), ‘Private ratings’ are availed directly by investors’. As such the process followed for assigning the ratings is highly similar and should not be construed as inferior to Public ratings. The aforesaid entity viz. CG Power Solutions Ltd., is not a regular borrower in the market and has hence not opted for a ‘Public ratings’. The practice of availing Private ratings as such is routine and is employed by many other mutual funds locally.

Capitalmind:You mention a private rating and we have tried to connect with other funds to understand the rationale but this is not something that has happened in the funds we connected with.

Additionally the new SEBI regulations for rating agencies (http://www.sebi.gov.in/cms/

Additionally the new SEBI regulations for rating agencies (http://www.sebi.gov.in/cms/

In this regard, we request you to let us know:

a) which rating agency has provided the private rating and

b) what rating has been provided (i.e. A, A+, A(SO) etc. )

DHFL Pramerica Replies: Our transaction was concluded in December and the private rating of the transaction is perfectly in line with extant SEBI guidelines. So our transaction as well as the private rating is in full conformity. Given that the rating was a Private mandate, we are a signatory to certain conditionalities, reps & warranties which are standard for such private mandates. These mandates do not permit any disclosures pertaining to the transaction including the name of the Rating agency or the rating, since this is purely for internal use and not for any public dissemination. You will appreciate that any sharing of information in this regard will cause us to be in breach of these norms.

We however would reiterate our earlier response that the rating is from one of the top two rating agencies and is in “high investment” grade.

Capitalmind: Such a private rating, in our opinion, is akin to no rating. If it cannot be disclosed which rating agency it is that rated it, and what the rating was, then it’s not really rated.

Sub-note: We don’t agree with having private ratings of any sort. Even the regulator might agree with us here. The concept of rating is that everyone knows. Getting an “investment grade” rating from a rating agency makes sense only if the rating agency will let the world know if the debt servicing is going sour.

DHFL Pramerica: Lending under a Corporate guarantee structure is a ‘standard practice’ since the credit view in such cases is assumed on the Parent which is issuing the Corporate guarantee as against the borrowing entity. The borrowing entity’s financials are consolidated with those of the Parent under the consolidated financials since the holding share in this case is 100%. As such both the credit / investment view and the Rating agency view factor in the Parent’s strength over and above those of the issuing entity.

Few recent examples of bond issuances under a Corporate Guarantee structure are as under:

a) Tata Power – Welspun deal – backed by a CG of Tata Power and rated AA(SO)

b) Talwandi Sabo / Balco issuance backed by Vedanta CG – rated AA- (SO)

c) L&T Nabha – backed by a CG of L&T and rated AAA (SO)

DHFL Pramerica: Lending under a Corporate guarantee structure is a ‘standard practice’ since the credit view in such cases is assumed on the Parent which is issuing the Corporate guarantee as against the borrowing entity. The borrowing entity’s financials are consolidated with those of the Parent under the consolidated financials since the holding share in this case is 100%. As such both the credit / investment view and the Rating agency view factor in the Parent’s strength over and above those of the issuing entity.

Few recent examples of bond issuances under a Corporate Guarantee structure are as under:

a) Tata Power – Welspun deal – backed by a CG of Tata Power and rated AA(SO)

b) Talwandi Sabo / Balco issuance backed by Vedanta CG – rated AA- (SO)

c) L&T Nabha – backed by a CG of L&T and rated AAA (SO)

Capitalmind: Note that all the above bonds are rated. A rated bond with a guarantee is fine, typically. An unrated bond with a guarantee is a little strange.

Even more strange: CG Power Solutions’ results don’t seem to have been consolidated with the listed company in Dec 2016. It has been consolidated for earlier quarters. (See Sep 2016 auditor note, and Dec 2016 auditor note – the Dec list of cos has no CG Power Solutions (India) Ltd.) We’ll follow this up.

DHFL Pramerica: The Parent (CG Power & Industrial Solutions Ltd.) enjoys an outstanding A1+/ AA- rating. The Parent company has stable financial metrics reflected in a market capitalization of over INR 45 bio, PAT of INR 1.28 bio and Networth of INR 42.42 bio, as on 30-9-2016.

The gearing of the Parent entity which stood at 0.4 x at the end of September 2016, has improved further post the conclusion of the sale transaction of its overseas automation business for a deal value of Euro 120 mio in March 2017. The deal proceeds are proposed to be utilized to reduce debt levels in the Parent entity. The transaction formalities are scheduled to be completed by end March 2017. As such the overall financial position is expected further strengthened.

DHFL Pramerica: The Parent (CG Power & Industrial Solutions Ltd.) enjoys an outstanding A1+/ AA- rating. The Parent company has stable financial metrics reflected in a market capitalization of over INR 45 bio, PAT of INR 1.28 bio and Networth of INR 42.42 bio, as on 30-9-2016.

The gearing of the Parent entity which stood at 0.4 x at the end of September 2016, has improved further post the conclusion of the sale transaction of its overseas automation business for a deal value of Euro 120 mio in March 2017. The deal proceeds are proposed to be utilized to reduce debt levels in the Parent entity. The transaction formalities are scheduled to be completed by end March 2017. As such the overall financial position is expected further strengthened.

Capitalmind note: The 120 million euro received will go only to pay out international debt. = The listed entity doesn’t show the additional Rs. 200 cr. as debt in the December results because of a consolidation issue. We’re not sure this helps the company’s books quite as much. But anyhow, the point is that there’s no collateral, and there’s an issue with unrated debIt that’s guaranteed by the parent as mentioned above.

5) What is your policy on NPA recognition in this case after a default? Would you wait 90 days before declaring NPA or would you mark it down by how much, given that this debt is unrated?

DHFL Pramerica: All our funds follow the principle of ‘fair market valuation’ (FMV) as prescribed by SEBI, in respect of all our security holdings. The FMV principle obligates the Asset Management Company (AMC) to appropriately value the securities in all cases and at all points of time. We believe it is untenable for an AMC to carry a debt security at full value post default.

Capitalmind: Fair enough. We’ll have to look at default situations carefully.

Capitalmind View

Even after the clarifications, it seems to us that there is something not-exactly-right with the unrated nature of the CG Power Solutions debt, which seems oddly in coincidence with the debt redemptions of Ballarpur. Plus, the CG Power Solutions results were not consolidated with the parent (see the notes on Auditors earlier). This retains our view that the fungibility among promoter run entities is possibly why this is happening, and that the debt still is in distress. We would still exit such funds and wait for further clarity on the unwinding of this debt, or a payout from Ballarpur.

Disclosure: The Analyst has no investments in any of the companies or fund schemes mentioned above. Analyst has no commercial relationship to any of the companies or funds mentioned above. This information is for educational purposes only – please consult a financial advisor before taking action.