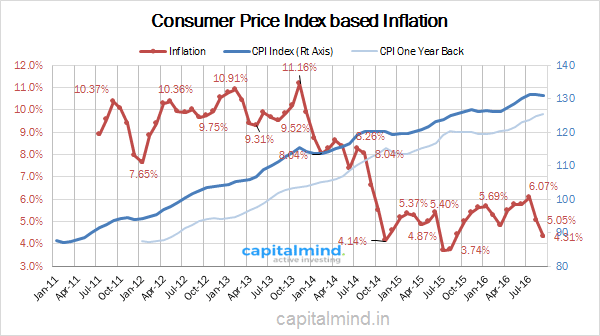

Consumer Price Inflation for September 2016 came in at a low 4.31%. This shows in the index with the major fall being in food inflation (which is just 4.1%) and Fuel (which is at +3.1%)

This is the lowest in a year! RBI’s rate cut move makes sense since inflation is this low. And they maintain a 1.5% “real” rate – meaning you can get 6.25% (the RBI repo rate) versus about 4.31% inflation, which is a good risk free rate above inflation.

Personal Care Costs Remain Stubborn But Other Components Fall

Component wise, here’s how it’s panned out:

Personal care has fallen only a little. Housing costs are at 5.2% and will rise when the pay commission changes are fully implemented into Housing Rent Allowance for Government employees.

Fuel costs are likely to go up in October only, if the oil companies hike fuel prices on Monday.

Food has fallen big time due to vegetables (prices are down 7%) and Pulses (inflation falls to only 14% from the 40%+ levels recently).

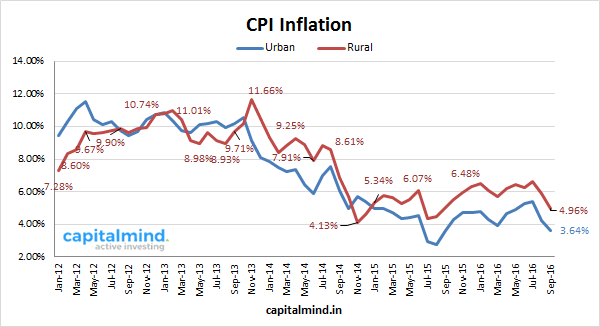

Rural and Urban Consumers Benefit

Low inflation translates into all demographic boundaries, it seems:

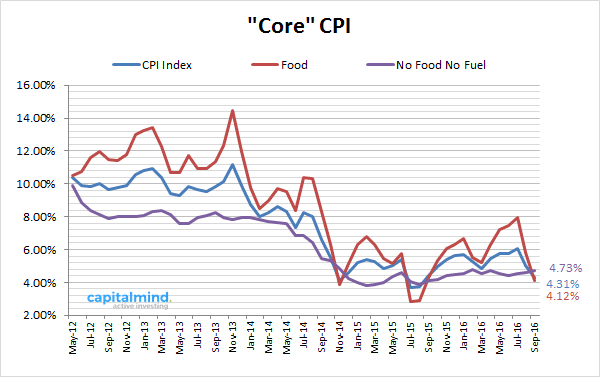

But Core Inflation Isn’t Going Down

If you remove the food and fuel impact – these are prices that are volatile in general – and look at “secondary” inflation, that is more “core” to the exercise. Your tomato prices can fall to Rs. 10 a kg, but your restaurant isn’t going to cut prices just yet. (It didn’t raise them either until the inflation was unbearable) The point is – secondary inflation is “sticky” and tends to take a lot of time – sometimes years – to come away.

Core inflation has remained largely benign through the time inflation went up and down, but now it’s again showing a small move up. For the first time in a year, core inflation is higher than both food and fuel inflation.

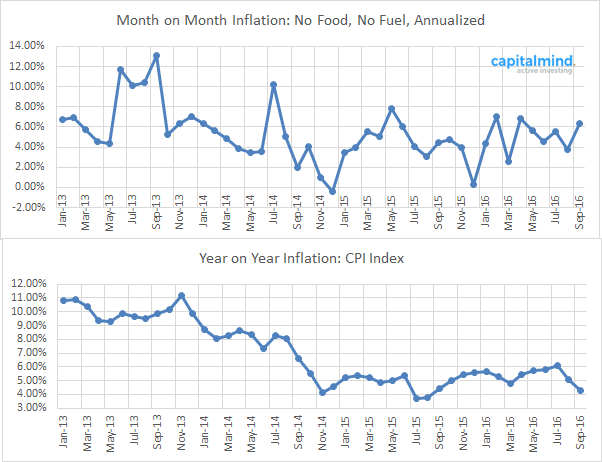

If you look at core inflation then you don’t need “seasonality” changes. We compare food inflation year on year only because month-on-month will not account for seasonality of certain items. But non-core items (restaurant prices) can actually be compared month-on-month. And that data isn’t looking so great.

We don’t yet have a problem – even at 4.7% year on year, or 6% month on month, this is not a big deal. However it does have the potential to hurt us if core inflation doesn’t fall.

The headline data still provides enough room for another rate cut when the RBI so desires. However, core inflation must moderate as well, and for that we might need more time.