Today we’ll speak of how to calculate the Cyclically Adjusted P/E Ratio, or CAPE, for the Nifty. Robert Shiller invented this for the US, so it’s also called the Shiller P/E Ratio.

Price to Earnings isn’t always usable. Companies run through cycles. Steel is in a downcycle. Cement is in an upcycle. And so P/E ratios – or the Price to Earnings Ratios – are consistently high in a downcycle, but the people who understand cycles will know that things normalize over the course of time, so they are willing to pay higher P/Es in downturns, and will pay lower P/Es in the upcycle.

To avoid this how about if we averaged earnings over a long time? That would run over any cycles and we will know the reality of how the earnings have grown if we compare it to the past?

That doesn’t work because of inflation. Inflation gives a company revenues and profits no matter what – because that’s how things are. If something cost me Rs. 100 to make and I sell it for Rs. 150, I have a profit of 50. If inflation is 10%, I can sell it at Rs. 165 next year, but my cost goes up to Rs. 110, meaning I make a profit of Rs. 55. That’s a 10% higher profit due to inflation alone.

So, we can “adjust” past profits for inflation. A Rs. 50 profit last year should be adjusted up by inflation, in the example above, to Rs. 55. Then today’s earning of Rs. 55 is exactly equal to last year’s earning of Rs. 50. We can THEN average these inflation adjusted earnings over time.

That means:

- We take past earnings of a stock or index, and adjust them up for inflation. We can do that with the CPI, for which we have back-date till 2001, through an RBI paper.

- We also then average out about 5 years worth of these inflation adjusted earnings to smooth over all the cycles. In India, we’re assuming a cycle lasts about 5 years.

We have earnings data from 1999 and inflation data from 2001, so the earliest we have valid data for is around 2006. (Needs a 5 year average)

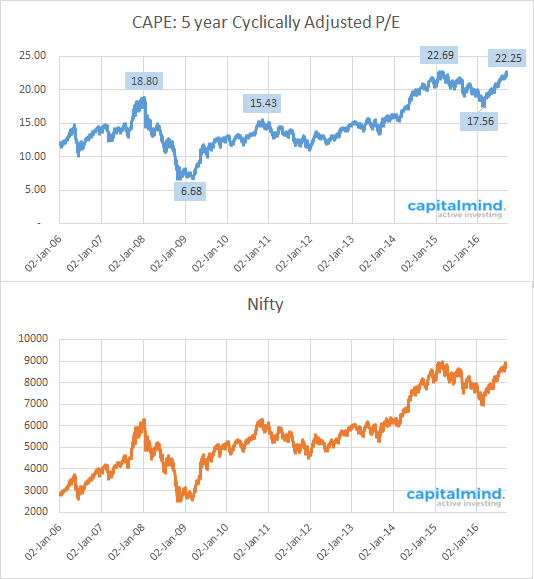

So we have this CAPE chart for the Nifty 50:

The higher this P/E ratio, the more richly valued an index is. At this point the Nifty is about as richly valued as it has been in 2015 January (and the market levels are the same).

A similar exercise with a 10 year adjusted P/E (rather than a 5 year) is a P/E of 24.07, again a very high relative level.

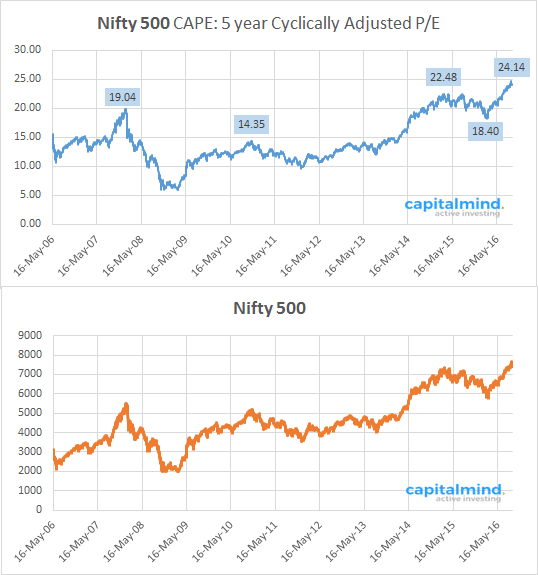

The Nifty 500 Though Is Off The Chart

It doesn’t really make sense to use CAPE for a narrow index like the Nifty which has only 50 stocks. Many of those are not even cyclicals (like banks or technology). We should take a larger industrial universe, and the prime fit here is the Nifty 500 (which is the top 500 stocks).

The CAPE for that is over 24 and the highest it has ever been.

(The 10 year Nifty 500 CAPE, for reference, is at 28.27)

This is also one of the slowest times in terms of earnings growth – which is negative, and earnings have contracted for the Nifty 500 in the last year (and indeed, inflation adjusted, in the last five years!).

What We Think

The CAPE or Shiller P/E tells us how this index is valued relative to its past, when you adjust for business cycles and inflation. And this P/E is at its highest today.

Note: For the US, you can visit multpl.com to get the S&P 500 Shiller CAPE.

At this point, the broad market looks frothy. Individual stocks, though, may be performing way better if you used the CAPE concept on their own earnings. But if the index itself has a very high CAPE, it is expected to give great earnings growth over time – but we have seen none of the past high expectations translate into reality at the index level.

![]()

DISCLAIMER: Please do not treat anything at in this email or Capitalmind Premium as investment advice. Capitalmind Premium does not provide any recommendations of securities. However, you may choose to consider our content as one input in your decision making process. While we may talk about strategies or positions in the market, our intent is solely to showcase effective risk-management in dealing with financial instruments. This is purely an information service and any trading done on the basis of this information is at your own, sole risk.