Following up on our post on banks’ NIMs, let’s take a closer look at their NPAs (non-performing assets), both Gross NPAs and Net NPAs, over the last quarter. There are 31 banks that had released their results for Q1 2015.

Gross NPA ratio is calculated as gross NPAs as a percentage of Gross Advances. The Net NPA ratio is simply that number adjusted for provisions for losses and unreceived interest. Since the base for banks would differ, it would be more meaningful to compare the ratios than the absolute numbers.

GROSS NPAS & RATIO:

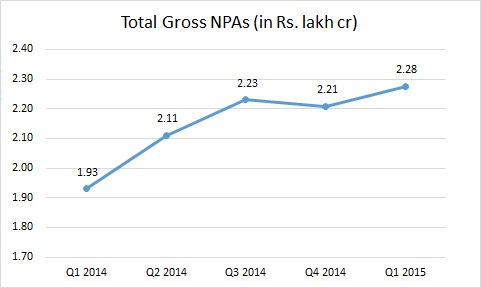

Total Gross NPAs has increased from Rs. 2.208 lakh cr last quarter, to Rs. 2.277 lakh cr this quarter; an increase of 3.13%. This is how total gross NPAs have been over the last 5 quarters:

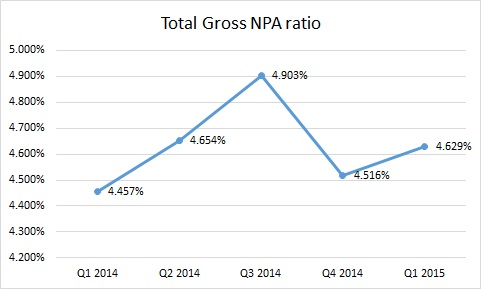

As a weighted-average (based on a specific bank’s Gross NPAs as a proportion of total Gross NPAs), Total Gross NPA Ratio (of all 31 banks together) has grown from 4.516% last quarter to 4.629%, an increase by .113%. Checking out the trend in total gross NPA ratio:

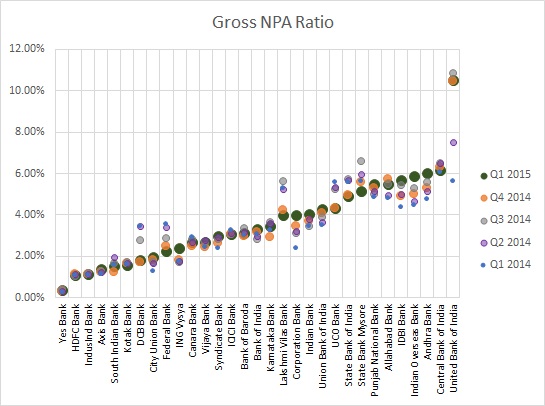

Looking at each bank individually, gross NPA ratios look this way:

The best bank by this metric, is Yes Bank, followed by HDFC, IndusInd, Axis and South Indian Bank.

- Yes Bank has not seen any drastic changes, either upwards or downwards in its Gross NPA ratio. Same with HDFC and IndusInd, there are very small changes in the ratio.

- Axis Bank saw a slight increase from 1.22% to 1.34% quarter-on-quarter.

- South Indian Bank too, saw an increase; from 1.19% to 1.50% this quarter.

On the other end of the spectrum the worst performing bank by some distance, is United Bank of India, followed by Central Bank of India, Andhra Bank, Indian Overseas and IDBI Bank.

- United Bank of India is quite a telling story: Its gross NPA ratio has been climbing since Q1 2014, where it was at 5.59%, to 7.52% in Q2 2014, to 10.82% in Q3 2014, and it has languished at those levels since. Its ratio right now is at 10.49%, up 2 bps from the previous quarter. Truly staggering, considering the next bank on the list is at 6.15%.

- Central Bank foresaw a slight dip from 6.27% to 6.15% q-on-q.

- As seen in the chart above, Andhra Bank, Indian Overseas and IDBI Bank have been seeing quarterly increases in their Gross NPA ratios; not a particularly impressive sign.

[blurb-capmind-prem]

NET NPAS & RATIO:

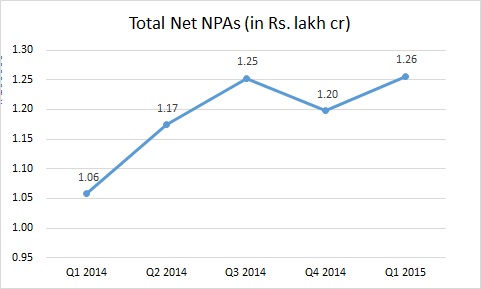

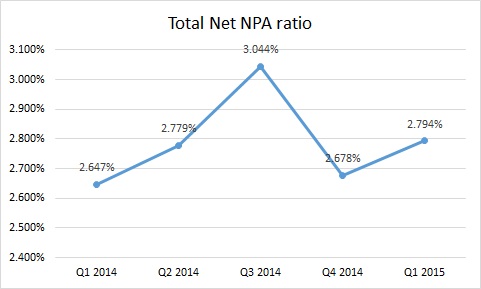

Now Total Net NPAs as a number increased to Rs. 1.256 cr from Rs. 1.198 cr last quarter, a 4.84% increase. For the last 5 quarters, this is what net NPAs have looked like

A steady growth q-on-q, except the anomaly from Q3 to Q4, which mirrors the trend for gross NPAs.

As a weighted-average (based on a specific bank’s net NPAs as a proportion of total net NPAs), Total Net NPA Ratio has grown from 2.678% last quarter to 2.794%, an increase of 11.6 bps. Checking out the trend in total net NPA ratio

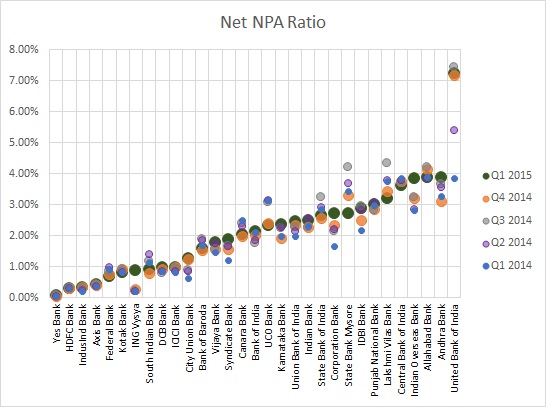

Individually, the banks tell a story of their own:

The best bank, again, is Yes Bank, followed by HDFC, IndusInd, Axis and Federal Bank.

- As with the Gross NPA ratios, Yes Bank has not seen much of a shift in its net NPA ratio; HDFC, IndusInd and Axis Bank tow the same line; very small changes in the ratio.

- Federal Bank on the other hand, shows a decreasing trend for this ratio, q-on-q.

At the other end, United Bank of India is the worst performer followed by Andhra Bank, Allahabad Bank, Indian Overeas and Central Bank.

- Just as its Gross NPA ratio indicates, United Bank of India saw a massive dip in asset quality, as its net NPA ratio climbed from 3.86% in Q1 2014, to 5.39% in the next, to 7.44% in the next quarter. It now stands at 7.23%, up 5 bps from the previous quarter.

- Interesting trends for the remaining 4; Andhra Bank oversaw an increasing Net NPA ratio (3.11% to 3.89%); so did Indian Overseas Bank (3.20% to 3.85%).

- Allahabad, Central Bank of India and Lakshmi Vilas Bank on the other hand, saw their Net NPA ratios declines q-on-q.

OUR VIEW:

These ratios are a very strong indicator of the asset quality of a bank; the higher the gross/net NPA ratio, the lower its asset quality.

United Bank of India retains the unenviable position of being the bank with the highest Gross & Net NPA ratios; and by a very large margin. Not just that, their ratios have climbed massively since Q1 2014, a sign that they possibly haven’t been lending too smartly.

In general public sector banks have been seeing deteriorating asset quality. Private banks remain within controlled limits, and importantly, seem to provision enough to keep Net NPAs within 1%. Public sector banks, sadly, have not.

With rising default potential, will NPAs of banks get even worse? Already we see an uptick from the March quarter and while the situation isn’t as bad (for the system) as the December quarter, the next quarter will tell if the trend is actually back upwards or if the June quarter was an anomaly.

Note: This kind of research and analysis is what we do at Capital Mind Premium. Do take a test ride!