This post was originally published in Dec 2021 and updated in June 2022 based on FY22 results and the latest developments.

As per the management of RBL Bank, things are slowly falling in place. But the investors are yet to believe in the story. Meanwhile, the stock is down by another -35% YTD.

On June 11th, the board of directors of RBL Bank confirmed the appointment of Mr R Subramaniakumar as the new MD & CEO of the bank. He is a veteran banker with 40 years of experience working with PNB, DHFL, and Indian Overseas Bank. However, the market didn’t like this development, pushing the stock down by -22% on the day of the news. But why?

As a general trend, RBI appoints veteran PSU ex-bankers to head the financial institutions in trouble. For example, Mr Prashant Kumar, former DMD of SBI, was appointed as the head of Yes bank. Mr Rajendran, an ex-Andhra Bank MD, was appointed as CEO of CSB Bank.

Please note that Mr R Subramaniakumar was associated with DHFL after it went belly up. In 2019, RBI appointed him as an administrator for DHFL to overview the insolvency process. This move further spooked the markets about the future of RBL Bank.

Concerns on asset quality are not new to RBL bank. The stock is down (-88%) from its all-time high and trading (-68%) below its IPO price of ₹ 225

So, what is happening at the bank? Is RBL Bank safe? Should depositors be worried? (Short answer: No). Why is RBL Bank’s share price going down? What should investors do? (Short answer: It depends)

Ratnakar Bank was founded in 1943, with its HQ in Mumbai. It was a rural-focused bank till 2010. In July 2010, Mr Vishwavir Ahuja, the former CEO of Bank of America, India, joined the board to make the bank future-ready. In Aug 2014, Ratnakar Bank renamed itself RBL Bank Limited.

The bank grew multifold under the management of Mr Ahuja. Deposits grew 46x. Advances grew more than 50x. Net worth 35x, from ₹350 crores to over ₹12,500 crores. Net Profit from ₹12 crores to ₹508 crores in FY21. Stellar growth numbers.

But aggressive growth at lending institutions tends to be accompanied by deterioration in asset quality.

All the buzz around asset quality

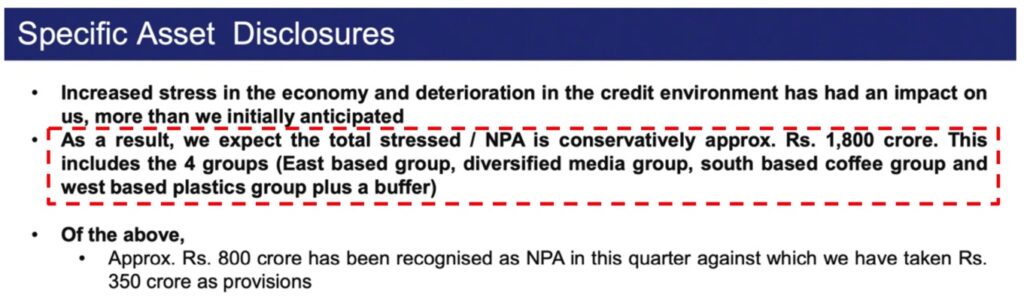

The first big blow in asset quality came in Oct 2019, when the bank released its exposure to groups like CCD, Sintex, and Essel group to the extent of 1800 Cr. This came as a big shocker to the markets.

*Snippet from Q2FY20 investor presentation

Just when the bank was coping with its stressed assets, the pandemic happened. RBL Bank, like all businesses, was impacted by the pandemic. But unlike others, it hasn’t recovered fully.

Gross Non-Performing Assets, NPA spiked from 1.38% pre-pandemic to 4.4% in FY22. Net NPA stood at 1.34%, up from 0.69% in FY19.

As of FY22, nearly 4.2% of the book is exposed to borrowers having BB+ & below credit ratings. That is around 2,467 Cr of outstanding risky loans on a total loan book of 60,002 Cr.

Provisions jumped from ₹2,228 crores in FY21 to ₹2,860 crores in FY22. Write-offs were also of similar magnitude. Since FY21, the company has cumulatively written off ₹3,968 crores.

Not good numbers, but not terrible, in the context of other banks.

To deal with losses from the pandemic, the bank raised ₹1,566 crores by Qualified Institutional Placement, QIP, in Nov 2020. In May 2022, the bank raised an additional ₹770 crores through Basel III – compliant unsecured and subordinated tier 2 bonds. This provided it with the much-needed capital. The Capital Adequacy Ratio, CAR, moved from 16.4% in FY20 to 16.8% in FY22. It also managed to bring down the cost of funds from 6.76% to 4.81% as of FY22.

The numbers say RBL Bank has not recovered, and the larger private sector banks are not necessarily worse off compared to other mid-sized banks.

How safe are RBL Bank depositors?

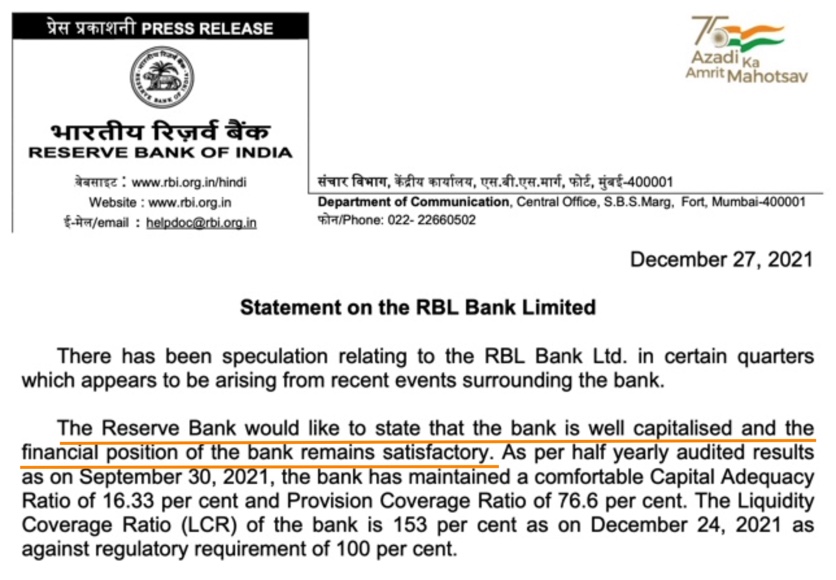

RBI says All is well

In Dec 2021, RBI released a press note stating everything was OK with RBL Bank. They clarified that RBL Bank is well-capitalized & in a strong position. They appointed Mr Yogesh Dayal as an Additional Director to support the bank in all regulatory & supervisory matters. RBI asked depositors and other stakeholders not to react to speculative reports that the bank’s financial health remains stable.

The numbers bear this out.

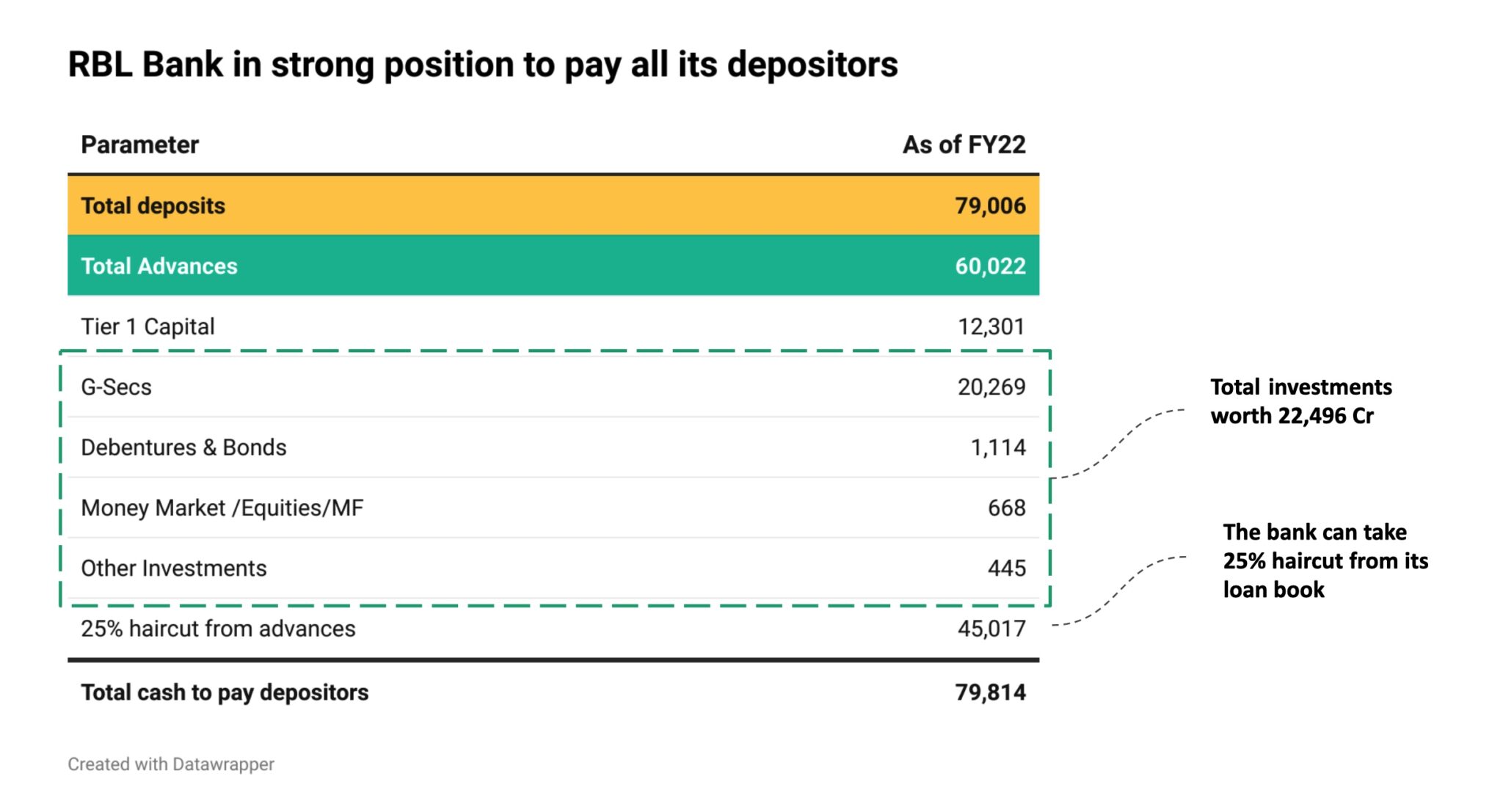

RBL’s balance sheet size is ₹1.06L crores. A deposit base of ₹79,007 crores and advances of ₹50,002 crores as of FY22. The bank has Tier 1 capital of ₹12,301 crores. They have a total investment of ₹22,274 crores across G-Secs, Bonds & other money market instruments.

The bank has strong liquidity of ₹34,575 crores, i.e. 44% of total deposits. The remaining 56% can be arranged from the sale of assets at a discount of 25%. In other words, even if 25% of the loans become toxic, the bank still will be in a position to honour all its depositors.

If required, the bank can raise approx 79,000 from its investments & sell assets to pay its depositors.

From the depositors’ perspective, things are stable. We don’t see significant risk with the bank.

But RBL Bank shareholders?

In financials, perception breeds price. Cleaning up a bank and improving book quality is an arduous task. It may take years before meaningful improvements, if and when they happen, get noticed. In short, it depends on whether “the worst is over”, which no one can say just yet.

Long-term investors will need to keep a close eye on both fundamentals & technicals of the bank. With the kind of handholding & monitoring from RBI, things should slowly start to move in the right direction. A few quarters of balance sheet cleaning may be left before they return to growth.

Two recent instances

In Dec 2018, Capital First NBFC was merged with IDFC Bank to form IDFC First Bank. Mr V. Vaidyanathan was the new MD & CEO of the merged entity. Considering his experience at ICICI Bank & how he turned around Capital First (erstwhile Future Capital), the market was bullish on the stock. Yet, three years later, he is still dealing with legacy loans. The market hasn’t given a premium to the bank yet.

Another infamous example was Yes bank. Mr Ravneet Gill joined Yes Bank with a commitment to revive it. Fifteen months later, he exits the bank as RBI had suspended the board. His task remains unfinished to date.

As of now, both these banks are stable. Asset quality has been improving, albeit slowly. Stock prices, however, haven’t shown strength.

For existing long-term investors, till the perception of the bank changes, reconsider total allocation to the stock and ensure it is within reasonable limits. Read Commonsense Position-sizing for investors. Avoid averaging down to reduce your buy price. If you choose to stay invested, knowing that the price might not recover for a while, consider a trailing stop loss to prevent further erosion to the portfolio.

How about fresh positions in the stock?

Not yet. For the reasons mentioned above, not until clear signs of improvement to the underlying business and, importantly, perception is evident.

The stock is currently trading at 0.4X book (other mid-size banks with better asset quality are at 1.5X to 2.5X book). The bank is leveraged at 11.5 times. In has to go for a fundraise soon to bring down leverage & prepare for further write-offs.

We’d refrain from trying to catch the bottom in RBL Bank stock.

Further Reading:

Our piece on Yes Bank from 2019: Are Yes Bank deposits safe, will the stock price recover?

https://www.youtube.com/watch?v=bWqJKVNzT-o&t=3s

This article is for information only and should not be considered a recommendation to buy or sell any stocks.