Opening a broking account is one of the first things you would need to do to get started as an Investor or Trader. In this post, we do a detailed comparison of two of the larger broking houses in India. Which brokerage should you pick?

You’ve read up a bit about how to start investing and you’ve saved some money, and you’re finally ready to rake it in on the stock market! But now what? The next step is to get a broker or what is also called a trading & DEMAT account which allows you to buy and sell shares.

You have several choices when it comes to opening a Trading account, from bank brokerages like ICICI Direct and HDFC Securities to independent brokerages like Zerodha and Upstox, the sheer number of choices can be overwhelming.

Before we delve into the comparison between Zerodha and ICICI Direct account, a bit about how depositories work. If that does not matter to you, skip this part.

DEMAT & depositories

In India you have two depositories, NSDL and CSDL, now these are the folks who are responsible for maintaining the records for various financial securities: Shares, Bonds, Mutual funds etc. These depositories keep records in dematerialized (DEMAT) format, in other words in an electronic format.

But you cannot directly access these depositories, you need an intermediary and they are called Depository Participants (DP), these are the entities which transact on your behalf with the Depositories and make sure every time you buy or sell your shares, it’s recorded with the depository.

Usually, the brokerage firm also happens to be a DP, if they are not, they may use the services of an existing DP.

For instance, in the past Zerodha used to use the services of IL&FS which in turn was registered with both NSDL and CDSL the two depositories, now Zerodha is itself registered as Depository participants (DP) with CDSL and hence does not need an intermediary like IL&FS.

Now that we’ve got a sense of what is what? Let’s delve into the question – With which brokerage should you open your account?

ICICI Direct vs. Zerodha

1. Account Opening Process

Both Zerodha and ICICI Direct provide both Online and Offline account opening processes. For online account opening (with any broker) one would need an Aadhar Card linked to a mobile number, the reason being e-KYC is possible only through Aadhar.

For an offline account opening process you need to download forms sign them and submit them to the broker, both the brokers provide a home collection of documents in case of offline account opening.

NRI Account Opening – While ICICI Direct provides an online process for NRI account opening, Zerodha allows only an offline account opening process for NRIs.

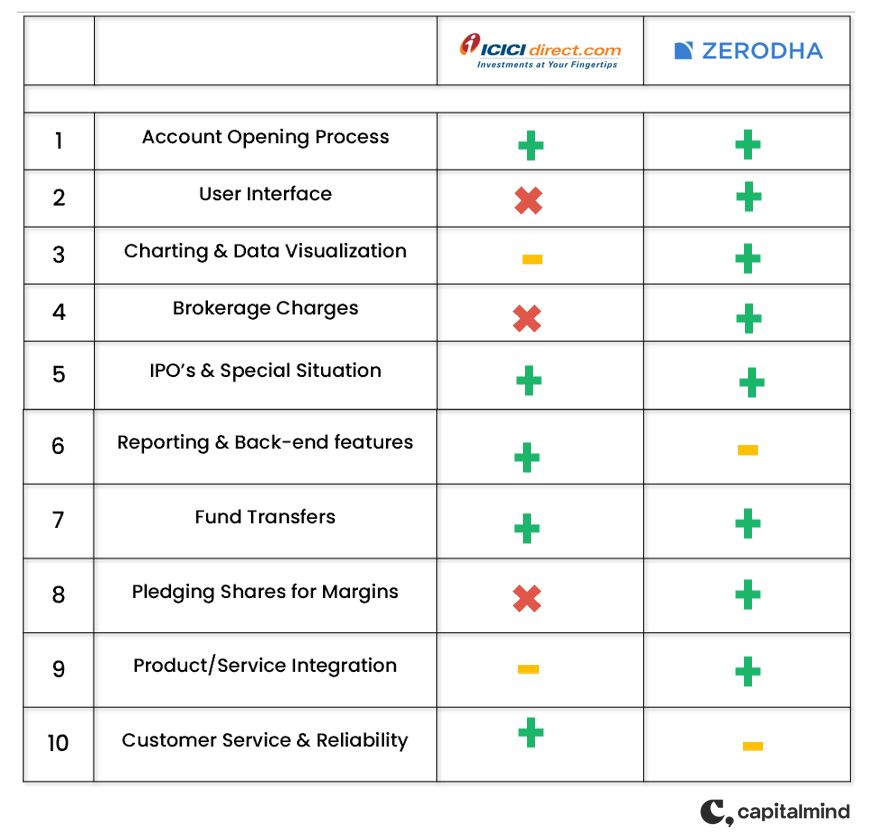

Our pick on ease of Account opening: Draw

2. User Interface

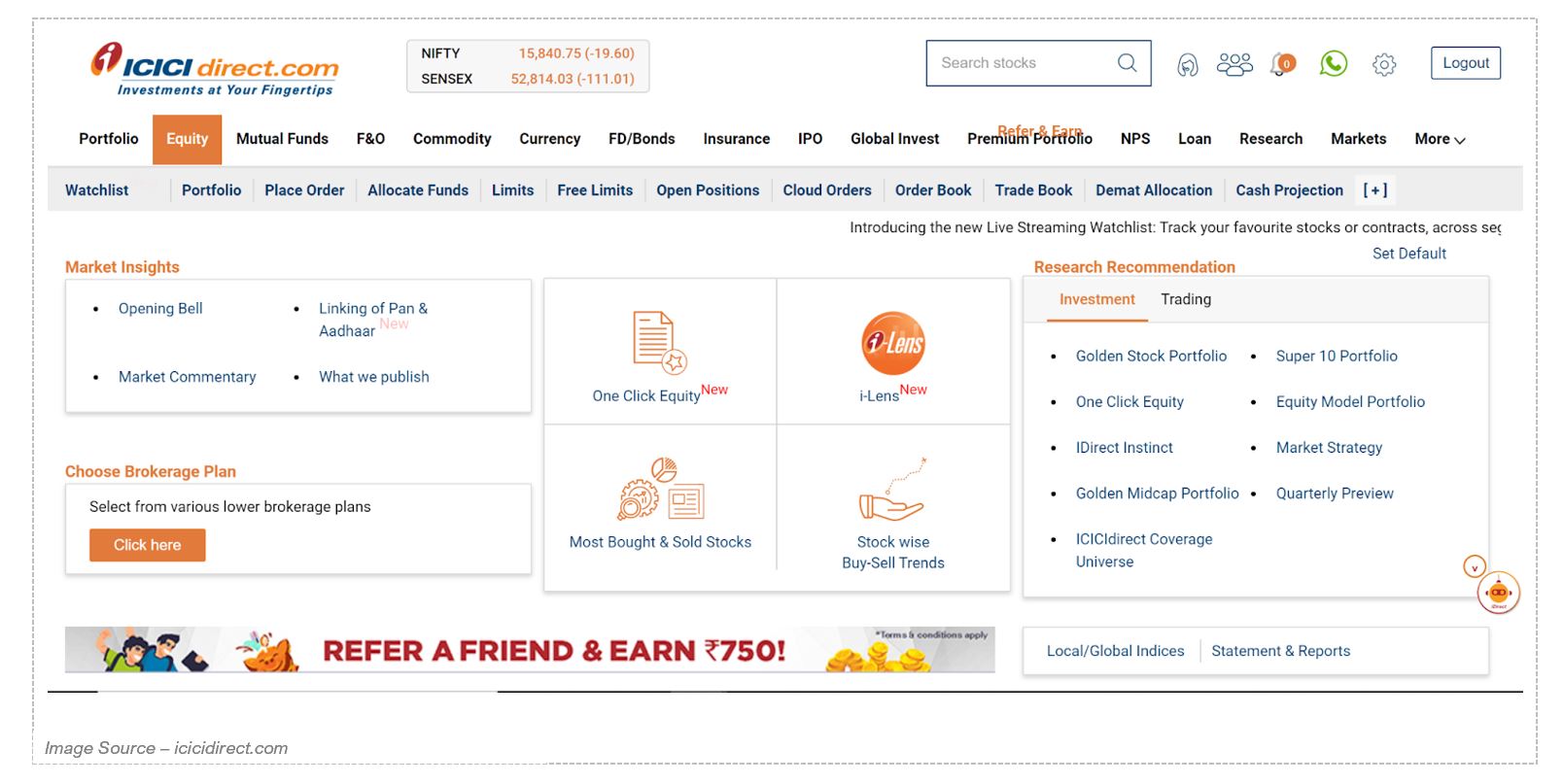

User Interface (UI) is not something one should even need to explain. So here’s the landing page right after you log in on ICICI Direct, to start with.

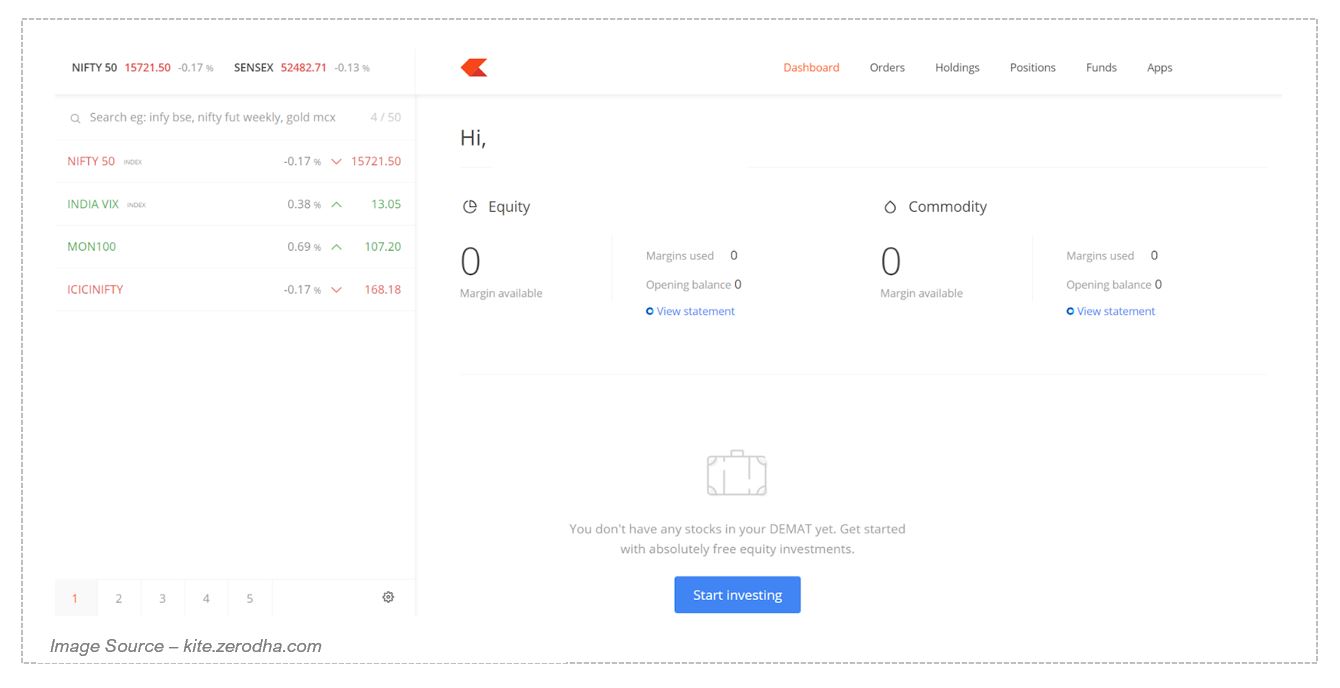

Next is the landing page of Zerodha, the moment you log in.

If the landing pages don’t make it evident, lets look at UI from a functional standpoint, let’s look at a simple Buy/Sell process flow.

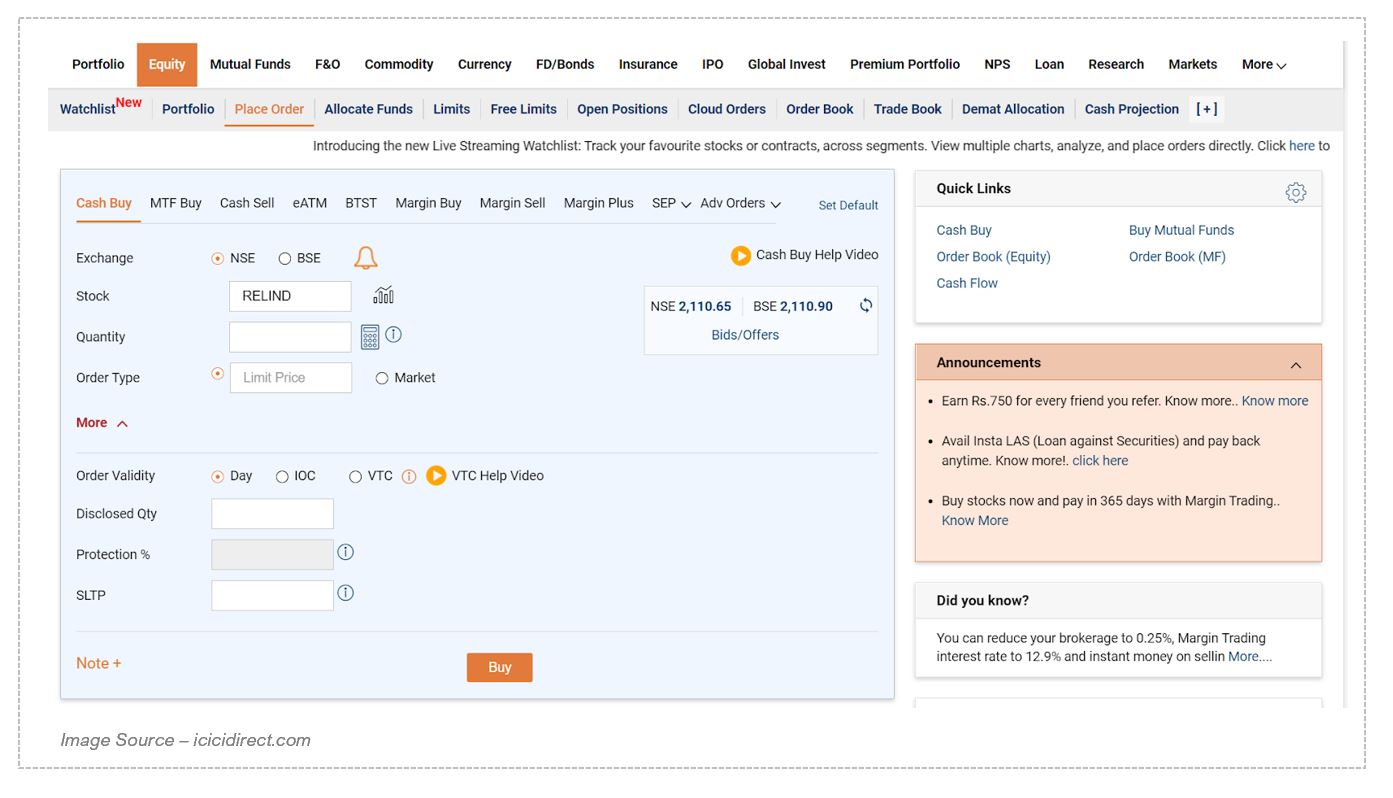

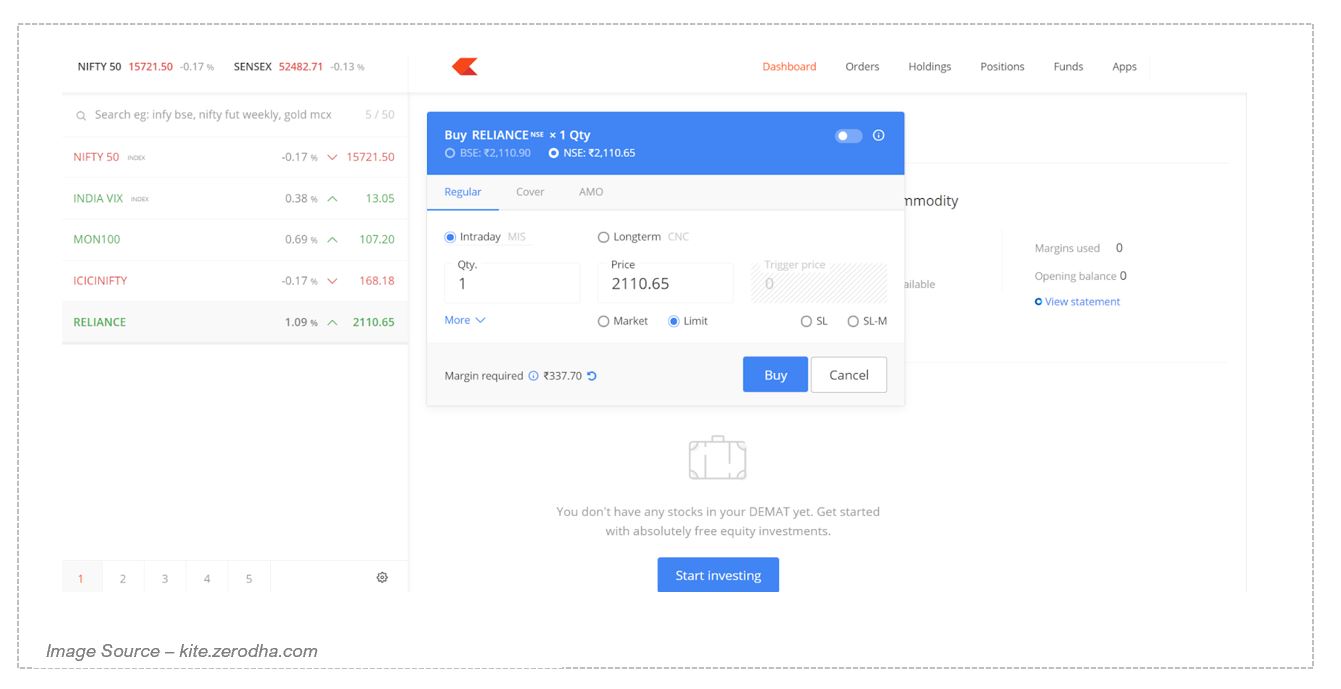

It took us about 7 clicks to execute a buy order in ICICI Direct. Lets do the same in Zerodha.

With Zerodha it took us close to 4 clicks to place a Buy order.

This difference in the UI extends to the mobile apps as well. Zerodha certainly takes the cake on this one.

Our pick on User Interface and Experience: Zerodha

3. Charting & Data Visualization

Beyond executing trades the next most frequently used feature is Charting. ICICI Direct offers basic charting, you need to add a stock to the watchlist and you see the option to visualize it. It uses the same charting engine i.e. Cosaic/ChartIQ, that Zerodha kite uses, however there are some differences.

ICICI Direct also offers a desktop-based, downloadable trading platform called TradeRacer which is resource-heavy but has its own charting.

Currently, Zerodha does not support any Desktop-based trading platforms for its retail clients. (Corporate clients have something called Nest which we won’t talk about here)

Zerodha however, offers two different charting engines, ChartIQ is one, and the other is TradingView. You can select any one of them depending on the specific features that interest you. You cannot run both ChartIQ charts & TradingView charts parallelly though.

One of the things unique to ICICI Direct is the visualization of Derivatives data through their integration with Heckyl.

Our pick on Charting and Data visualization: Zerodha

Our pick on Charting and Data visualization: Zerodha

4. Brokerage Charges

If you are a trader or even an investor who invests in strategies that are relatively more active, the brokerage is something that should bother you.

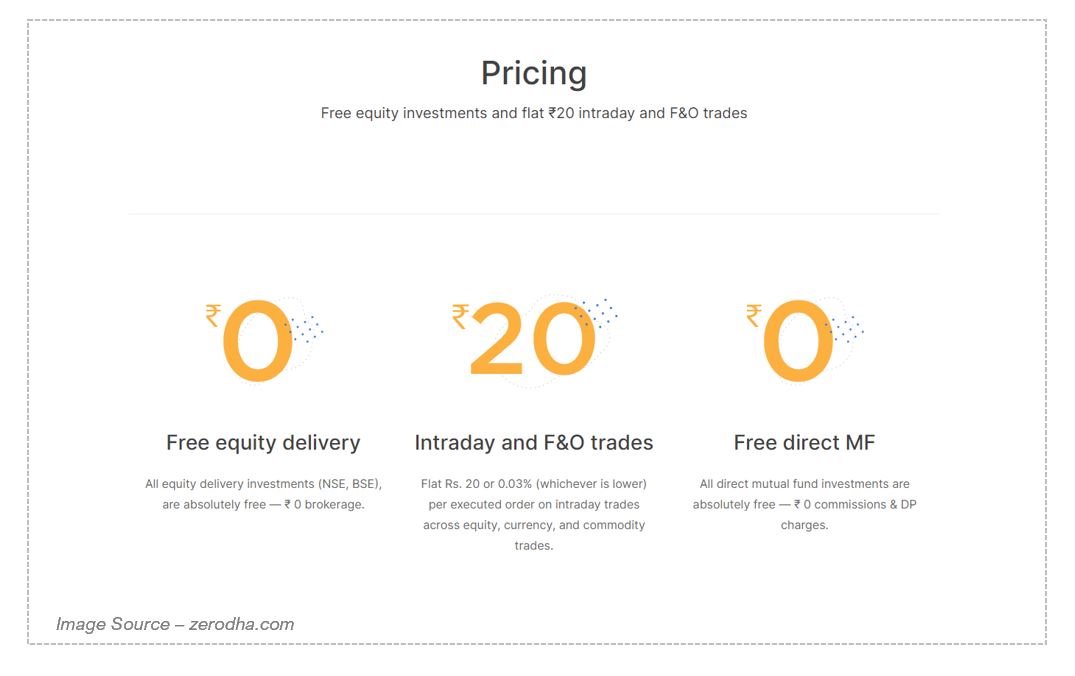

Zerodha – One must remember that Zerodha started as the country’s first discount broker, that Makes them pioneers in low cost brokerage.

They’ve always kept their brokerage plan (Yes, they just have one) quite simple.

For Equity Delivery it’s Free. I mean the brokerage is free, you would still need to pay the exchange transaction charges and stamp duty though.

For Equity Intraday and Derivatives (Futures & Options) its Rs. 20 per order or 0.03% of the turnover whichever is lower.

For Mutual Funds it’s free again, no commissions & DP charges either.

ICICI Direct – ICICI Direct started as a full service broker and for a very long time held the position as the top broker in terms of active clients, till 2019 when Zerodha toppled it to occupy the top spot.

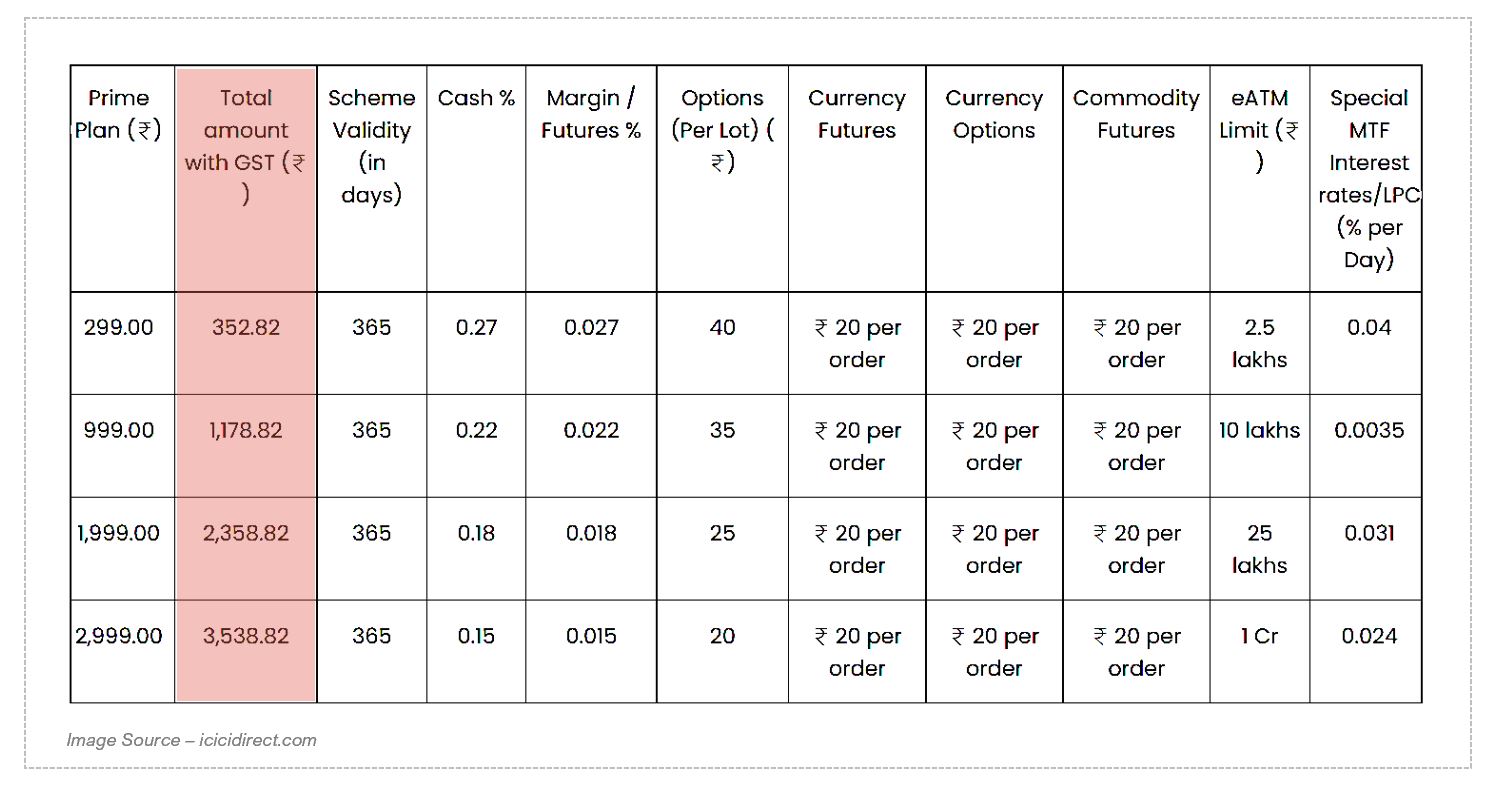

Their Brokerage charges are based on ‘Plans’ a bit like Broadband or Mobile plans. Depending on the plan you choose your per order brokerage differs.

Here’s their Prime Plan (This is as of July’21 )

The second column, here highlights the price of the plan, this is a fixed amount that you would have to pay, for instance if you pay Rs. 3,538 you would need to pay 0.15 % of the turnover as brokerage, for Cash/Equity segment, 0.015% for Futures segment, Rs.20 per Order for Options and so on.

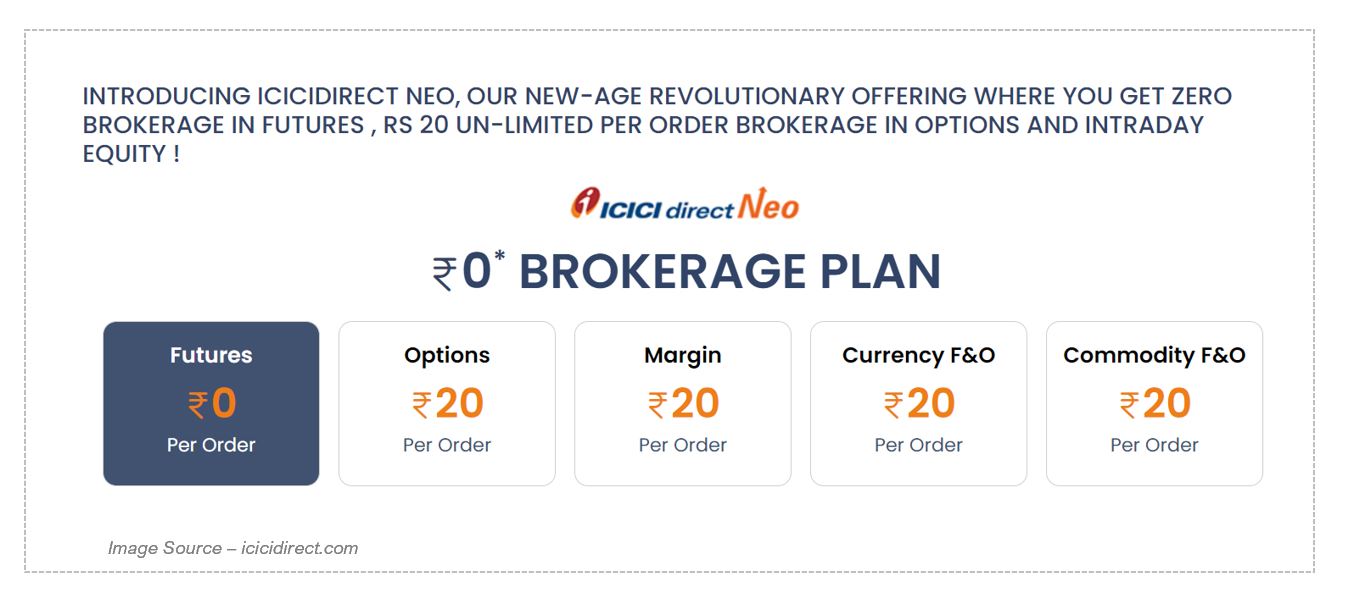

They also have a plan called NEO where they have fixed brokerage per order but that’s only for the derivatives segment.

More about their plans over here, however, they do not have any plan that either has free or fixed brokerage for the cash/equity segment.

Lastly, you cannot buy Direct Mutual Funds from ICICI Direct, you can only buy Regular Mutual funds, there are two types of costs that would affect you as an investor.

One is, the increased TER (Total Expense Ratio) in regular funds, TER which is the cost of running and distributing a fund is actually added to the NAV of the fund, which reduced its returns, on top of it ICICI Direct also charges a transaction fee for buying mutual funds in excess of Rs. 8 Lakhs.

For instance, if you opt for a SIP approach, you would pay, Rs. 30 or 1.5% of the investment value whichever is lower.

More about it here.

Our pick on Brokerage Costs: Zerodha (by a distance)

5. Applying for IPOs and Special Situations

While both ICICI Direct and Zerodha offer fairly simple process flows to apply for IPOs However if we were to compare it step by step ICICI Direct is way simpler and requires you to follow lesser steps to apply for IPOs.

Situations like Buybacks and OFS (Offer for Sale) – Again, the process to apply for such special situations is both simple and easy, with both the brokers.

Our pick on IPOs and Special Situations: icicidirect

6. Reports & Back-end features

This is one area where ICICI Direct arguably beats Zerodha. ICICI has a very robust Reporting with archiving for ever since you started. While Zerodha has gotten a lot better over the years, if you are a very old user it’s still possible that you may get into trouble looking for older reports.

From a usability standpoint, ICICI Direct reporting is well integrated with the trading platform, whereas in Zerodha it’s a different application, though it uses the same login credentials as the trading platform Kite.

Our pick on Reporting and Back-end Features: icicidirect

7. Fund Transfers

Deposits into the trading account are a breeze with ICICI Direct if you have an account with the bank, one nifty feature is that it shows you the bank balance as well and that helps sometimes, the same logic obviously does not apply if you use non-ICICI banks.

Fund withdrawals also are seamless with ICICI as in technically it’s just single click Away. In other words, it makes absolute sense to be a part of the ICICI ecosystem if you are looking at using ICICI Direct.

Zerodha also has made it as seamless as possible for you to add and withdraw funds, but it’s not a part of any banking ecosystem like that of ICICI, here you need to add a Primary or a Secondary bank account through which you can transfer funds into Zerodha, the time it takes to reflect in your trading account depends on the method of transfer.

Fund withdrawal, however, cannot be as quick as it can be with ICICI Direct account linked with an ICICI Bank account though.

Both offer UPI-based transfers as well. Zerodha being more user-friendly when it comes to UPI transfers.

Our pick on Fund Transfers: Draw

8. Pledging Shares for margins

Note: the concept of pledging has changed recently. Earlier shares used to leave your account and go to the broker’s margin account. Now after the Karvy fiasco, where pledged shares were misused, the system has changed: shares are marked as pledged in your demat account (they don’t leave the account).

Zerodha beats ICICI Direct hands down on this one, the pledging process actually has two legs, first part is on the brokers side, where the broker has to allow you to pledge Shares, Mutual Funds and ETFs select them all of that, and then is the second part which is the same for all, as this is the OTP authorization process.

Zerodha is incredibly transparent and easy when it comes to pledging Shares, Mutual funds and ETFs.

On a related but different note, earlier ICICI direct used to offer Loan against securities and Zerodha didn’t, but now Zerodha also has an NBFC license and it also seamlessly offers loans against securities.

Our pick on Share Pledging for margins: Zerodha

9. Product/Service Integration

Typically one broker cannot provide all value-added services and features its users need, this is where product integration helps.

Zerodha again has been a pioneer in this space in many ways, at the moment it offers Integration with three products, Sensibull which is an Options analysis platform, SmallCase which offers baskets of stocks & ETF similar to curated portfolios, which allows for a single click execution, Quicko a tax planning and filing product, and TradingView if you want to include that too.

ICICI Direct also has just about one such integration i.e. with Sensibull.

Our pick on Product / Service Integrations: Zerodha

10. Customer Service & Reliability

ICICI Direct has been a full-service broker has always had better service levels compared to Zerodha. Even today it’s relatively easy for one to get through to their Customer service on the phone than Zerodha.

However, Zerodha has a fairly efficient ticket resolution process.

Talking about reliability if you look at social media reports you would definitely find more instances of Zerodha’s trading platform being down, compared to ICICI Direct, but that could also be due to the relatively active, tech-savvy clientele that Zerodha caters to.

If you are an investor, these glitches should not bother you at all, as they last for anywhere between a few minutes to a few hours and if you are an active trader, you should definitely plan for such events and have necessary backups.

Our pick on Customer Service: icicidirect

Visual Summary of comparison between icicidirect and zerodha

Overall Verdict

For ICICI banking customers, setting up an icicidirect 3-in-1 account is seamless. Their reporting, reliability and customer service are an advantage in this head-to-head comparison with zerodha.

But zerodha scores on ease-of-use, charting, and the all-important consideration of costs. In the long run, as a retail investor or trader your net savings on everything from brokerage to mutual funds transaction costs, will be substantially higher with Zerodha.

Given these two options, retail investors are better off picking Zerodha over icicidirect.

You might also like to read: Which is the best Mutual Fund App in India?

Capitalmind received no payment or compensation for this review, neither do we have any affiliation or relationship with the owners of the product or service being reviewed.

Sandeep is on twitter @mysandz. To connect with us about Capitalmind Premium or the PMS, write to us at premium [at] capitalmind [dot] in or on twitter @capitalmind_in