In this post we look at the Q4FY19 results and share notes from the conference call of a tyre company that we have talked about earlier.

Balkrishna Industries (BKT)

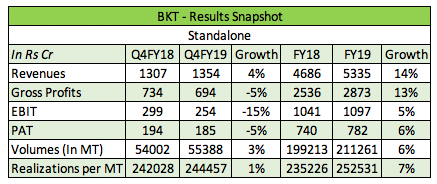

BKT announced its results on 17th May, you can find the result note here. The conference call was held on 20th May and we attended the same. In this post, we shall share our notes from the call. But, first let us look at the Q4 and full year results.

Sales have grown by 4% in the latest quarter, on the back of volume growth of 3% and increase in realizations by 1%. Revenues shown in the above table include realized gain on FX on the back of sales. For Q4FY18 the FX gain was Rs 75 Cr and for Q4FY19 Rs 3 Cr. Inclusion of these gains at the top line has also impacted the gross and operating profits.

Sales for the full year increased by 14%, on the back of volume growth of 6% and increase in realizations by 7%. For the full year FX gains on the back of sales was Rs 91 Cr for FY19 and Rs 221 Cr for FY18.

Gross profits have declined by 5%, adjusting for the FX gains gross profits have actually grown by 5% from Rs 659 Cr to Rs 691 Cr. Gross profit margins (GPM) stood at 51% versus 53% in Q4FY18 (excluding FX gain). Management has stated that the margins have been impacted during FY19 due to higher raw material prices. Gross profits for the full year was Rs 2,873 Cr, registering a growth of 13% over the previous year. GPM for the full year was 54% similar to the previous year.

Operating profits or EBIT for the quarter declined by 15%, the impact of including FX gains in the top line is clearly visible here. Expenses below the gross profit line haven’t seen a substantial increase, the largest expenses are the other expenses, these have increased by 4% at Rs 299 Cr from Rs 288 Cr. Operating profit margins (OPM) stood at 19% in the latest quarter versus 23% in Q4FY18. Operating profits for the full year was Rs 1097 Cr, registering a growth of 5%. Growth has been hampered due to increase in other expenses by 26% from Rs 935 Cr to Rs 1,179 Cr. The company has incurred higher expenses on branding and advertisement to strengthen brand BKT. OPM for the full year were 22% versus 21% in FY18. The company expects to maintain these margins over the next couple of years.

Net profits or PAT for the quarter stood at Rs 185 Cr, drop of 5%. PAT margins at 14% versus 15%. PAT for the full year was Rs 782 Cr versus Rs 740 Cr in FY18, growth of 6%. PAT margins for the full year were 15% versus 16% in FY18.

Consolidated sales for the full year was Rs 5,482 Cr versus Rs 4,800 Cr in FY18. Net profits were Rs 774 Cr versus 736 Cr in FY18.

The company’s working capital (Inventories + Receivables – Payables) has seen a jump of 29% during the year. Working capital at the end of FY19 was Rs 890 Cr versus Rs 690 Cr in FY18. The increase is primarily on the back of increase in inventories by 23% from Rs 619 Cr to Rs 759 Cr and receivables have increased by 8% from Rs 480 Cr to Rs 517 Cr. Payables on the other hand have decreased by 6%, from Rs 490 Cr to Rs 386 Cr.

Borrowings at the end of FY19 were Rs 871 Cr versus Rs 651 Cr at the end of FY18, increase of 34%. The debt/equity ratio for both the years was 0.2. The company had cash and investments of Rs 1,135 Cr at the end of FY19. The company has a net cash position, adjusting for debt of Rs 264 Cr.

Notes from Conference Call

Volume sales for the full year can be split region wise, segment wise and replacement and OEM sales.

In terms of region, Europe contributed 51% to full year volumes, USA – 17%, India – 18% and rest of the world (ROW) – 14%.

Agriculture segment contributed 61%, OTR – 36% and ATV and lawn garden 3%.

Volumes from the replacement market were 71% and OEM contributed 29% to volumes.

The demand for the next year is bleak, the company expects degrowth in the industry. However the company has guided for 3-5% volume growth guidance for FY20. Demand is impacted due to trade wars and weather impact in Europe. As per the management the sentiment across the world is that of caution, even though the company derives majority of its revenues from Europe and trade wars are between the USA and China. The company is upbeat on India, this market is growing at 17-18% and the company expects to maintain this momentum.

CAPEX for the year was Rs 757 Cr. The company expects to incur CAPEX of Rs 1,400 Cr over the next two years. The CAPEX details are as follows

- 425 Cr on carbon black plant for total capacity of 1,40,000 MT. Company has commissioned 60,000 MT for Rs 175 Cr and this facility should start production in H1FY20. 80,000 MT will be commissioned in FY21

- 500 Cr in Waluj, to replace old plant

- 500 Cr in Bhuj, to set up capacity of 5,000 MT of large sized all steel radial OTR

- $100 Mn to set up 20,000 MTPA capacity in the USA

The company is looking for land in the USA all other CAPEX should be done in the next two years. Apart for the above CAPEX the company will incur maintenance CAPEX of 250 Cr per annum. CAPEX will be meet through internal accruals, if there is a need for taking debt, the company will borrow in foreign currency.

Raw materials are softening and demand is looking bleak, this has already triggered players in the industry to reduce prices. Competition in the market has already taken price cuts, BKT will also have to do the same as the company does not enjoy pricing power in the market for its products.

The company has global market share of 8% in the agricultural tyres market and 2-2.5% in the OTR segment. Overall the company has global market share of 5%.

Way Forward

There is a slowdown in demand and management has guided for volume growth of 3-5% for FY20. The reasons for the slowdown are trade wars, weather conditions in Europe and auto slowdown across the board. We believe these issues are short term in nature and will be overcome over the course of time, these are not structural issues which hamper the growth of the company permanently.

Full year EPS is 40/share, at the current price of Rs 768 the company trades at 19 times earnings. These are not mouth watering valuations. However the company over the years has proven its mettle –

- Sales growth of 14% and profit growth of 29% CAGR since FY09

- Capital allocation – average ROE and ROIC of +20% over the last 10 years and successfully executing the Bhuj CAPEX

- Maintained manageable debt levels, current D/E ratio of 0.2

- Positive cash flow from operations (CFO) every single year since FY09. Cumulative CFOs in the FY09-18 period is Rs 5,404 Cr, in the same time net profits were Rs 4,080 Cr. CFOs are greater than the net profits and indicates efficient working capital management. Cash conversion cycle in FY18 was 66, this has been coming down over the years

The global OHT market is estimated to be $12-15 Billion, 2/3rd of this market is the OTR tyre market (used in construction, mining) and agricultural tyres form 1/3rd of the market. BKT has global market share of 2-2.5% on the OTR segment and 8% in the agri tyre market. BKT has a market share of 5% and there is huge scope of growth on this front. BKT has also taken steps to increase its share – like sponsoring events in key markets to gain visibility and is in the process of setting a plant in USA.

While there are headwinds in the near term, we believe that the stock should deliver over longer period. However the stock will not do much on the earnings front over the next year and it will not be surprising if there is fall from these levels.

NOTE: As a disclosure some Capitalmind authors may own the above company in their stock portfolios. There is no other relationship between Capitalmind and the above company. Please do not consider this article as a recommendation, It is purely for informative purpose only.

Foot Notes

Our Premium Long Term Portfolio is at https://capitalmind.in/

Our Premium Momentum Portfolio 2.1 is at https://capitalmind.in/

Our Premium DivYield Portfolio is at https://capitalmind.in/

Our Premium EV Portfolio is at https://capitalmind.in/