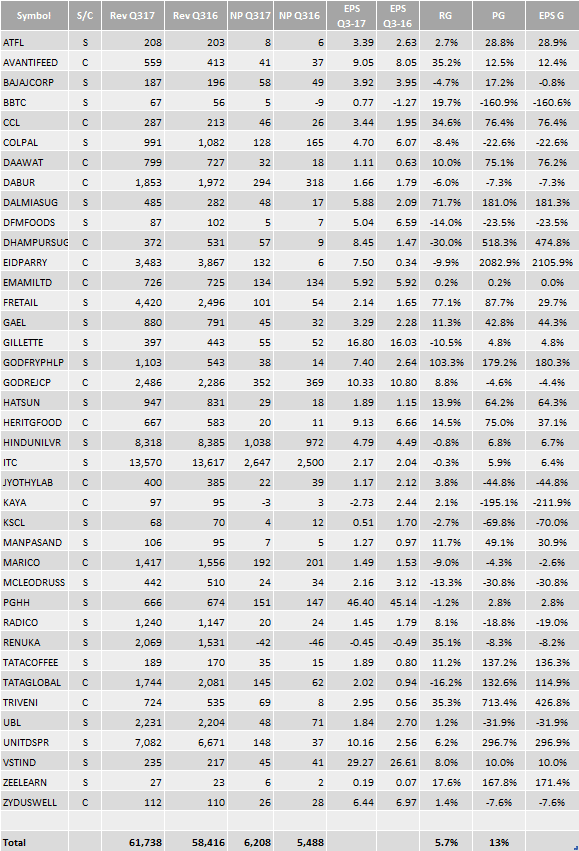

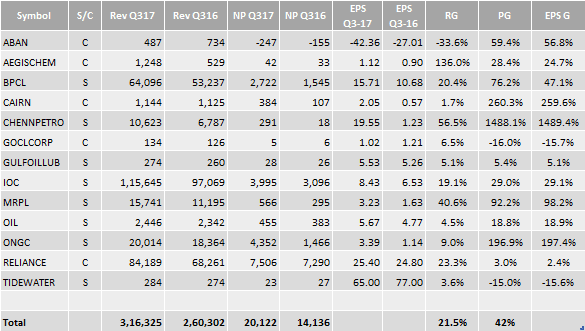

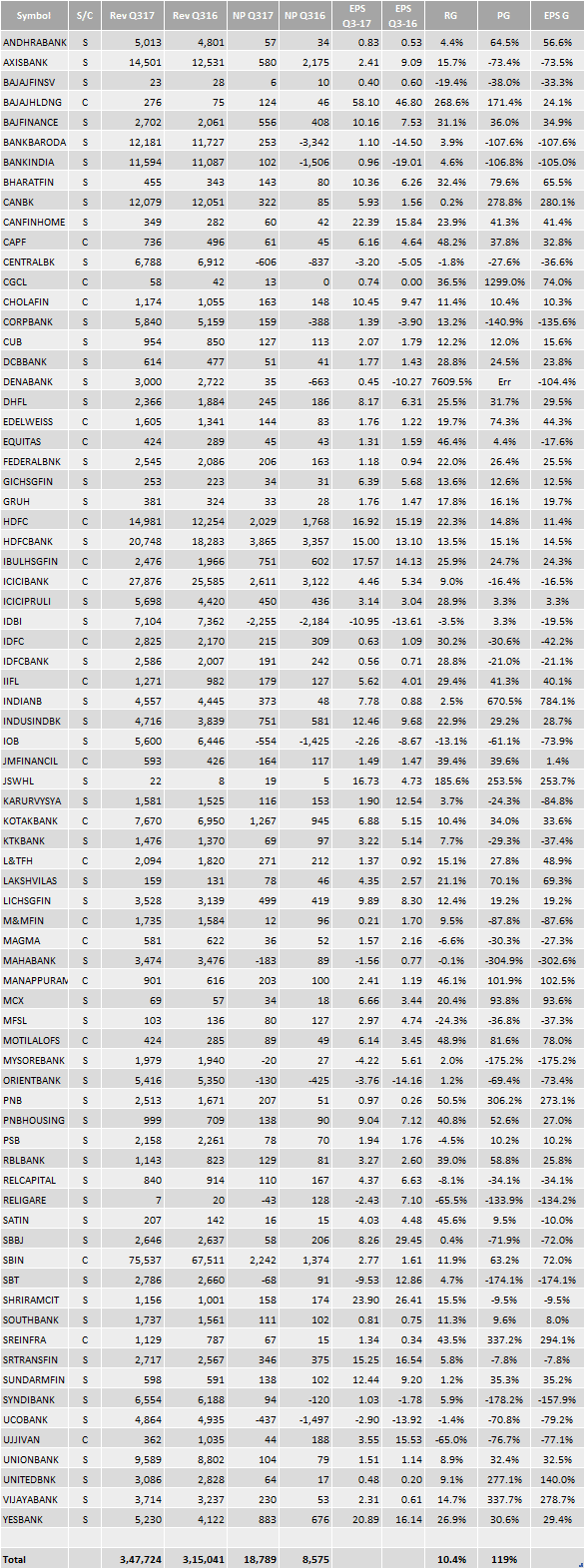

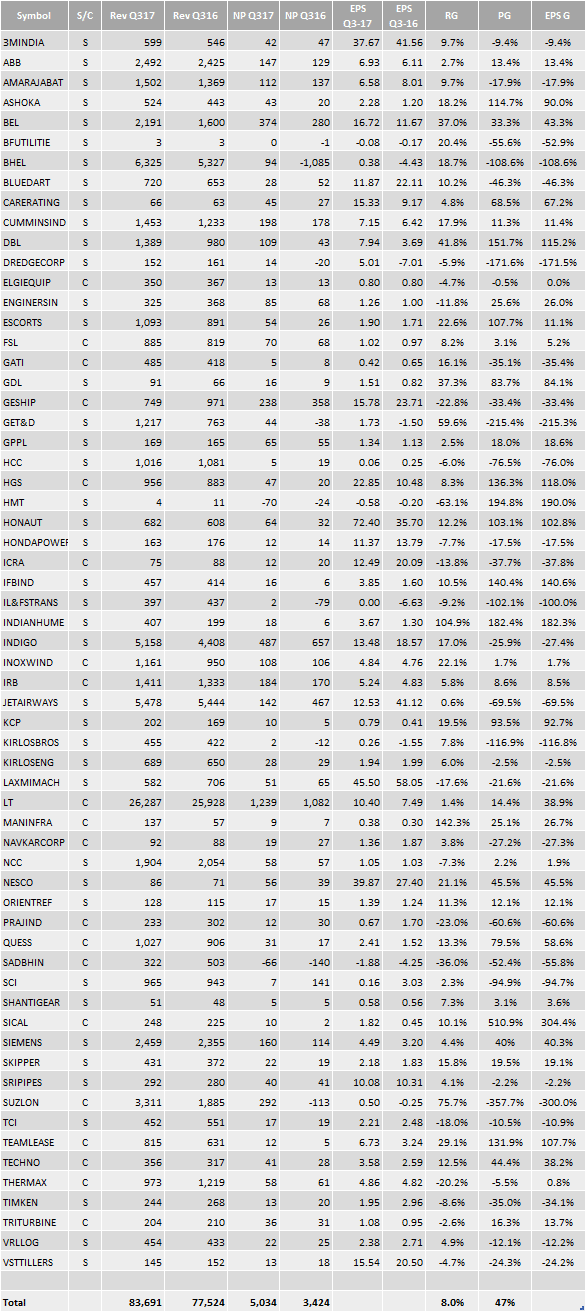

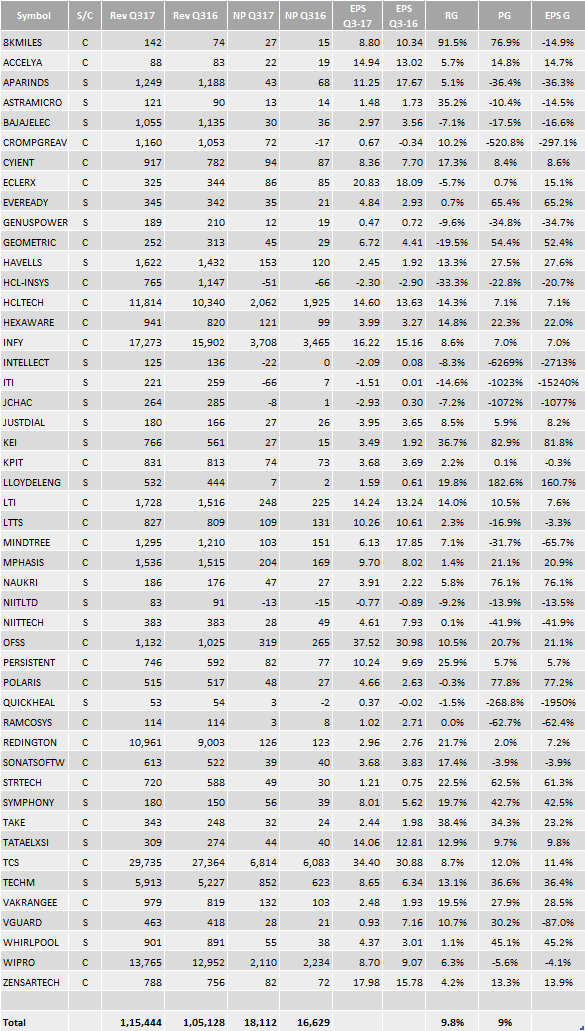

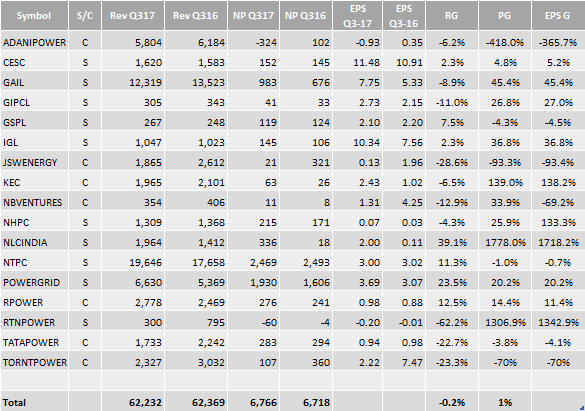

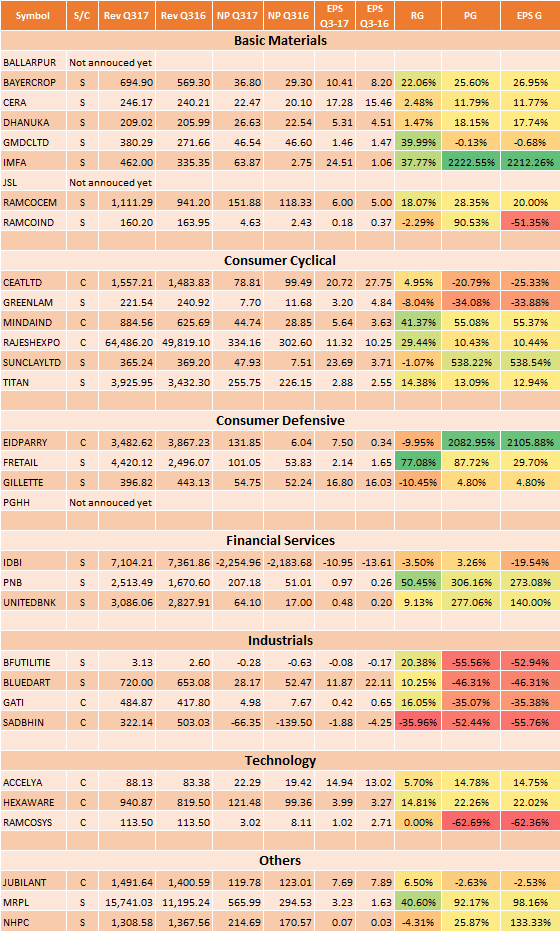

Here is a quick summary of the third quarter financial results for all the companies announced till date. For some companies, management comments have been reported here. Please refer notes at the bottom.

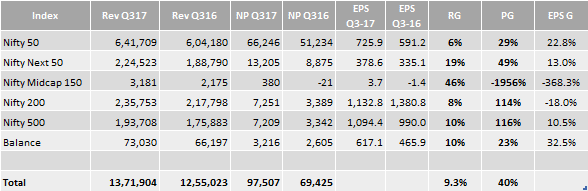

Indices

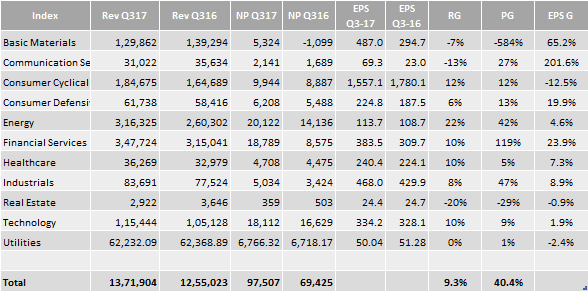

Sectoral

Basic Materials

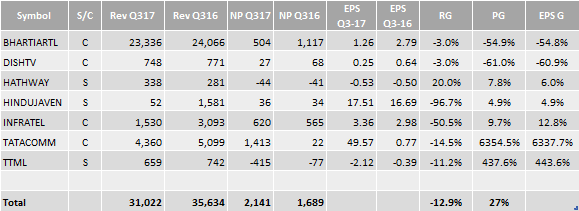

Communication Services

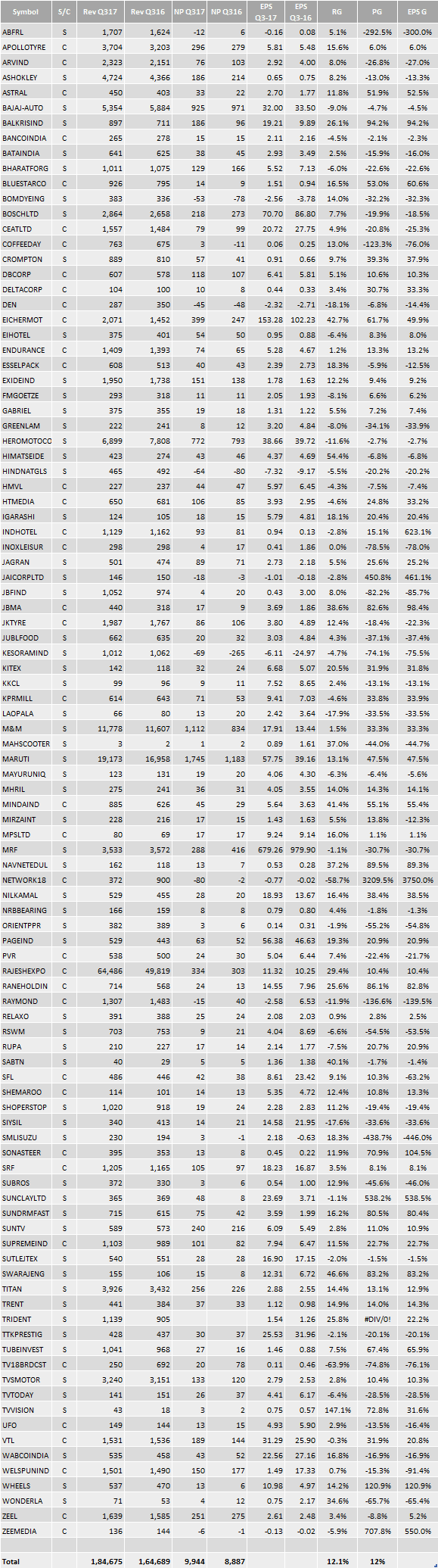

Consumer Cyclical

Aditya Birla Fashion & Retail

- Revenue stood at Rs. 1,707 Crore against Rs. 1,624 Crore, PAT went into negative at Rs. 12 Crore from a positive Rs. 6 Crore. (YTD PAT stood at Rs. 32 Crore).

- Q3 started with strong festive sentiments in October

- November sales fell by nearly 25% – 30% post announcement

- December witnessed a healthy recovery, though overall business continues to be lower than normal.

Ashok Leyland

- Expecting just like the rest of the industry pre-buy because of the Euro IV implementation – expecting 15% to 20% growth. Greater clarity in February as to where the pre-buy and how the pre-buy is going to happen

- LCV business – currently have only one vehicle – Dost. The PARTNER and MiTR faced some disruptions in the supplier’s engines but have resumed production.

- If cash for clunker happens, then anywhere from 400,000-500,000 to maybe 800,000-900,000 vehicles will need replacement over some period of time.

- Defence revenues are in the range of 3% to 5% of the overall revenues. Domestic Truck & Bus business contribute 71%, Exports close to 10%, LCV about 5% with the balance coming in from aftermarket.

- Export revenue for Q3 stood at Rs. 388 Crore.

- Inventory levels have gone up in Q3 and that is part of the planned strategy so as not to miss sales when the demand comes back before April, 2017.

- Plant inventory stood at 11,500 vehicles

Crompton Greaves Consumer Electricals

- Lighting business growth close to 5% (B2B business is roughly about 50%).

- Premium fans volume growth close to 40%.

- LED business grew by 83% and now comprises more than 55% of total lighting revenue.

- Agricultural pump growth remained flat 0.4% – slowdown in agricultural pumps linked to demonetization

- In appliances, water heaters showed a good growth of about 28% as Q3 is the key seasonal quarter for water heaters.

- Foresee headwind in terms of commodity cost.

Eicher Motors

- Total Income from operations stood at Rs. 2,071 Crore as against Rs. 1,452 Crore

- Profit after tax stood at Rs. 417 Crore as against Rs. 278 Crore

- Royal Enfield motorcycles – strong volume growth in the third quarter despite many issues in the quarter both – macro issues and extraneous issues.

- Even around demonetization the bookings and sales were not affected.

- Available at more than 640 dealers covering 400 cities across the country as on December, 2016 (500 a year back).

- Himalayan launched it in Australia and Columbia both in November, 2016.

- Oragadam capacity is absolutely on full stream and delivering as many motorcycles. Capacity expansion in the new facility which is facility 3 at Vallam Vadagal, Chennai is on track and expected to be commissioned in Q3 of FY2017-18.

- VE Commercial Vehicles – month of November and December were extremely hard on the commercial vehicle industry as a result of demonetization.

- Situation currently in CV seems to be improving because BS4 emission norms are coming all over India by 1st of April.

- RE – did not take any price hike though material cost have marginally gone up by 0.2%. Last hike was in August, 2016 at 0.9%. VECV price hike in October at 1% due to blended goods.

- We can only sell BS4 vehicles from 1st April. Any BS3 stock which is lying at the end of March cannot be sold from 1st April.

- Approximately three-month wait in for the highest selling model of Classic – based on customer deposits.

- Smaller town’s potential vs Big City dealer potential is stands at 20-30 and 100-150 respectively.

- Entry point for production into next year in any case is 60,000 units a month

Jubilant Food Works

- Same Store Growth (SSG) declined 3.3%

- Net Sales stood at Rs. 658.75 Crore against Rs. 633.76 Crore

- Standalone Net Profit stood at Rs 19.9 Crore

- Company has now opened 95 Domino’s Pizza and 11 Dunkin’ Donuts thus far

JFL Chairman Shyam S Bhartia and Co Chairman Hari S Bhartia said:

Q3 has been a challenging quarter for the consumer sector on account of currency demonetisation. However, we were able to minimize the impact by offering multiple non cash payment options to customers and launch of new products which got excellent customer response.

Shoppers Stop

- Post-demonetization 20% de-growth in Department Store format

- 55-56% of business comes from credit, debit cards while the balance comes from cash

- South zone in spite of demonetization actually recorded a double digit growth while larger impact witnessed in east and north.

- Apps downloaded generate 20% of online sale. E-commerce contribution to overall sales stands at 1% with a target of increasing it to 10% in 3 years.

- Net addition of stores stood at 4 for the quarter with new stores taking anywhere between 24-30 months to start paying back and contributing to overall revenues. 2 stores closed down contributed revenues of below Rs. 45-50 Crore.

- Stop n Live and Life are two of the biggest brands as they contribute almost 70% of the entire private brand sale. Next year growth will be driven by Women’s Ethnic Wear brand – Kashish and Hot Curry

- Least productive category for the company in ascending order is Home, followed by Kids, followed by Women’s Ethnic Wear and then Women’s Western Wear, Men’s Casual Wear and then Non-Apparel.

Consumer Defensive

Emami

- Reduction in discretionary spends that consumers spending mostly on the essentials.

- Consolidated revenues at Rs.726 Crore s, Profit after tax at Rs.134 Crore s

- Domestic revenue grew by 3% during the quarter with volume growth of 0.2%.

- Boroplus antiseptic cream grew by 13%

- Petroleum Jelly grew by 21%

- Boroplus lotion grew by 10%

- Kesh King grew by 2% – mostly sells in the rural areas

- Fair & Handsome Face Wash grew by 38% and

- 7 Oils in One grew by 35%

- Navratna Cool Oil declined by 4%

- Balms declined by 5%

- Fair & Handsome cream declined by 18% – due to demonetization as this is a pure discretionary spend item

- Overall distribution moves – presently company will cross 7 lakh outlets by March, 2017; with a visibility of adding another lakh outlets by next year.

- Price hike in Q3 was in the range of 2%

- Coconut being the largest selling variant in India and South is predominantly a coconut market so to put footprints in south the base is coconut with the same values of Kesh King.

- Targeting double digit growth i.e. 12% to 14% for next year

- Next big move for FMCG would be the introduction of GST

- Presently wholesaling contribution to the total business is almost 50% to 55%

- Next 2-3 months things would be more or less normal or very stable

Energy

Financial Services

Cholamandalam Investment and Finance

- Disbursements for the quarter were at Rs. 4,373 crores. Rs. 3,491 crores in vehicle finance against Rs. 3,245 crores – Tractor, CE, and CV, and PV. No difference in performance of these segments other than Tractor which went up in the month of November and has improved into December and started improving. Rs. 619 crores towards Home Equity disbursements against Rs. 882 crores.

- LAP financing business –Average ticket size on the loan is about Rs. 50 lakhs disbursed out of 88 branches. Maximum ticket size is about Rs. 7 crores. Most of the tickets that have been funded in the larger ticket sizes lie between Rs. 3 crores and Rs. 4 crore. Currently the company has 20,000 LAP accounts.

- MSME business is primarily bill discounting done out of 5 branches with an average ticket size of Rs. 2.5 crores to Rs. 3 crores

- Demonetization – flat disbursement, slight increase in vehicle financing and decrease in Home Equity. Near-term impact on the used segment is going to be higher.

- Heavy Commercial Vehicle – BS-IV implementation from April will prepone the sale either in the end of February or in the end of March.

- Of the 166 new branches opened in the last two quarters, 158 branches are in rural areas. CAPEX and OPEX in new branches are maintained very low, currently in the range of Rs. 10-15 lakhs. 80% to 90% of these branches get profitable within the first year of operation. Looking to add another 100 branches or so most likely next year.

- IT foray driven post demonetization – digital payment, a co-branded credit card, working with UPI etc.

ICICI Prudential Life Insurance

- Average ticket size in the protection business stood at Rs. 10,000/-. These comes from 3 separate channels agency, bank relationship, as well as proprietary sales force. Protection product linked to loans comes from the bank channel and employer-employee kind of protection which comes in the direct channel.

- Fourth quarter, is probably the strongest quarter for most insurance companies. Demonetization move to be positive for financial services.

- IRDAI regulations on the corporate agency – Payment of commission or remuneration regulations were changed and they are effective from the 1st

- Bulk of the new business comes from the retail products which are sold across the channels. Existing client repeat sale including protection is still at a fairly low level.

- Different patterns across lines of business – younger generation (below 30) go for protection and slightly older for savings.

Sriram City Union Finance

- Full impact of the demonetization is yet to unfurl.

- Experienced near term delays in payments as the businesses have come down, cash has been out of circulation, the turnovers have come down.

- Business growth yet to pick-up. Collections were down for the quarter ended December 2016 by 9.9% compared to September quarter. Disbursements were down by 7.6% for the quarter at Rs. 5,146 Crore.

- Two-wheeler disbursements stood at Rs. 1,208 Crore. Dealer point sales were down by 40% to 60% for 2 wheelers.

- Home enterprise finance at Rs.1,934 Crore s

- Loan against gold at Rs.1,430 Crore s (30% dip)

- Personal loans at Rs.380 Crore s

- Auto loans at Rs.256 Crore

- Product wise mix of AUM was 55% for SME, 18% for two-wheeler. 15% for gold and 6% each for auto and personal loans.

- Currently stage – cash collection is greater than demand for gold loan. This would mean disbursement growth will be about 25% to 30%.

- No clear-cut answer on how GST is going to change the business.

- Colour on what prompted the resignation of the CFO Ms. Subhasri – she is available for the group and is moving into a software company – not going out of the group.

- Not seen any uptick in January. Two-wheeler and Auto absolutely not much of a change from December to January. Banking on SME for an uptick.

Ujjivan Financial Services

- Total Income at Rs. 371.32 Crore , an increase of 4.01% over Q2-FY17 or 38.88% over Q3-FY16

- Net Profit at Rs. 43.94 Crore ; a decline of 38.43% over Q2-FY17 or 9.54% over Q3-FY16

- Gross Loan Book stood at Rs. 6,587.90 Crore while Net Loan Book stood at Rs. 6,046.35 Crore

- Disbursement stood at Rs. 1,662.84 Crore. During demonetization period disbursement to existing customers- stood at Rs. 965 Crore.

Mr. Samit Ghosh, Chief Executive Officer and Managing Director, Ujjivan Financial Services said:

Despite the challenging environment we have been able to maintain overall satisfactory performance. Our monthly collection efficiency for November & December was around 90%. However customers impacted by demonetization are continuing to repay with a time lag. Consequently as of date the collection for November & December dues stand at 95.4% and 91.1% respectively. We are confident that this trend will continue. We have maintained strong customer connect and critical support during this period with timely dissemination of information and continued loan disbursements to our valued customers.

Healthcare

Biocon

- BLA for our proposed biosimilar Trastuzumab filed in November 2016 was accepted by the US FDA for review with a target action date of September 3, 2017. (Actual approval time can vary and only after that the launch can be done taking into account various factors).

- Biocon SDN – Malaysian step down subsidiary, was awarded MYR 300 million contract to be serviced over a period of three years for supplying rh-Insulin cartridges and re-usable insulin pens. Revenues expected from Malaysian facility will be more than $50-$60 million expected.

- ANDA of Rosuvastatin Calcium also received FDA approval this quarter and we are gearing up for the commercial launch of this product in the US market.

- Booked licensing income of Rs. 79 Crore, R&D spend was Rs. 100 Crore (Rs. 350 Crore is full year guidance) – YTD spend is Rs. 201 Crore.

Divi’s Laboratories

- Standalone PAT stood at Rs. 268 Crore on a Revenue of Rs. 976 Crore against Rs. 246 Crore and Rs. 860 Crore respectively for the same period last year.

- US FDA Inspection update – Engaged with external consultants and experts for regulatory compliances. Read here more about the inspection. Company is awaiting an update from US FDA.

Dr.Reddy’s Laboratories

- Companies 3 plants which came under the US FDA scanner expect a re-inspection in February and March, 2017. Company has provided updates on its remediation plans in January 2016, March 2016, May 2016 and August 2016 for all its plants i.e. Srikakulan in Andhra Pradesh, Miryalaguda in Telangana and Duvvada, Visakapatnam.

- Lower contribution from Northern America and Venezuela led to a 9% decline in Global Generics revenue

- Revenues from Emerging Market declined 7% while from Northern America a 15% decline.

- Indian and Europe witnessed growth at 2.4% and 11% respectively.

Pfizer

- Impact of demonetization – the acute therapies got hit whereas the chronic therapy drugs initially got a small phase bump. IPM growth which was always trending at a double-digit level in this quarter actually came down to 5.7%.

- Impacted to the extent of about Rs. 15 Crore in the month of November because of the demonetization.

- Corex sales stood at Rs. 58 Crore (against Rs. 77 Crore YoY) while the overall sales reported by the company stood at Rs. 503 Crore.

Strides Shasun

- Regulated Markets Business

- Revenues grew 42% to INR 4,475 Mn against INR 3,150 Mn in Q3 FY16

- North America front end delivers best ever quarterly performance driven by continued market share improvement and a healthy sales traction for base portfolio.

- The company has recently received an FTF approval for Fingolimod Capsules. The product can be launched on generic market formation expected in February 2019, with a potential 180 day exclusivity.

- Australia business delivered a steady quarterly performance despite PBS impacts.

- Emerging Markets Business

- Revenues grew by 42 % to INR 1,697 Mn against INR 1,194 Mn in Q3 FY16

- Generics business in Africa continues to witness macro heads winds

- Demonetization impacted India brands business that led to destocking in the channel

Shashank Sinha, Group CEO, stated

Q3 was a solid quarter of revenue growth and margin expansion backed by gains in market share of key products. Growth was led by the formulations business as API operations normalised. Growth particularly in the regulated markets was strong despite delay in new product approvals. We continue to increase our investment in developing a robust new product pipeline.

Syngene International

- Revenue grew by 23% to Rs.347 Crore

- Profit after tax grew by 12% to Rs.74 Crore

- S2 facility caught fire – the ground floor housed biologics pilot plant, the mezzanine had some office space and the top three floors of the building were largely chemistry and analytical labs. Require around 12-months to remediate and reconstruct the facility. S2 lab is about 10% of the entire lab footprint and contributes 20% of total revenues.

- Lost one client contract with an annual value of around about Rs.40 Crore

- Abbott Nutrition – one of the clients in the dedicated services space has extended their contract for another year.

- The new CGMP formulations facility is on track to be commissioned in Q4 and is strategically positioned in providing integrated Discovery and Development Services.

- Received environment clearance for the commercial API facility in Mangalore. Expect construction to begin in the next fiscal and the facility to be operational in FY2020.

Unichem Laboratories

- Revenue at Rs. 360 Crore against Rs. 309 Crore

- International formulation business clocked in Rs. 123 Crore against Rs. 93 Crore

- Domestic business impacted due to demonetization stood at Rs. 203.64 Crore against Rs. 191.52 Crore.

- Export business – 15 of the 21 products approved have been launched

- Price erosion in US business – we have to face it as nothing can be done. This was in high single digit

- Goa API facility expansion – completed which can be seen in the depreciation numbers. Warehouse expansion is pending which may be taken up in a year or so.

Industrials

Real Estate

Technology

Utilities

Notes:

- All figures in Rupees Crore except EPS

- NP = Net Profit After Tax

- Rev = Revenue

- EPS = Earnings Per Share (Adjusted for Bonuses and Splits)

- C = Consolidated, S = Standalone

- If we have published an incorrect data set here, do let us know.

- Where earnings go from profit to loss or vice versa, things go a little crazy with the profit and EPS growth percentages. Please ignore them.

Love it or hate it, do leave us with your reviews in the comment section below!

{kind=link}